Market Analysis

Crude Oil

- Crude oil resumed the volatile, however price tone were more govern on long term supply situation as OPEC production cut compliance is also becoming an issue.

- The prevailing re-balancing of oil market doesn’t is not bringing confidence in the market as market participants are skeptical about the balance to stay along with production numbers from OPEC.

- Brent price closed at $52.10, slight reduction from last Friday closing price of $52.42/BBL, whereas WTI closed at $ 48.82, in comparison with last Friday price of $49.58/BBL, a decrease by 1.53%.

- According to OPEC, US, Libya and Nigeria are collectively pumping 1.55 million B/D more than last October, the base line number set by OPEC.

- Saudi Arabia production numbers reported by secondary sources are increased by 9,000 barrel a day.

- The non-compliance issue was discussed in an extra-ordinary meeting in Abu-Dhabi, but there is no strategy announcement.

- So OPEC production cut has not been effective as there have been quota busters and till the time there is robust compliance and reporting system in place, OPEC production cut impact will not be effective.

- EIA Weekly report reported a draw of 6.45 million barrels with stock at 475.4 million barrel on 4th August 2017; with market expectations were of 2.8 million barrels draw.

- Gasoline inventories at 231.1 million barrel reported on 4th August 2017, recorded a build of 3.4 million barrel as compared to last week draw of 2.5 million barrels.

- Baker Hughes rig count reported an increase of 3 oil rigs, with total standing at 768, whereas gas rig decreased by 8 and now at 181, with total number of rigs at 949

- IEA has revised historic demand data for 2015-2016, meaning a lower demand base in 2017-2018 combined with unchanged high supply numbers could lead to lower stock draws than initially anticipated.

- In my opinion, OPEC Production cut compliance along with US rig numbers needs to be monitored closely in coming days, as these two parameters will decided the long term crude price.

Natural Gas

- Henry Hub prices closed at $2.98/MMBTU, jumped by 7.58% from last Friday.

- Bullish tone is attributed to warm weather and lower than expected production number.

- Weather is going to be warm all across USA for the next week, which will increase cooling demand.

- EIA showed domestic supplies of natural gas rose by 28 BCF for the week ending August 4 against market expectation of 37 BCF.

- Working gas in storage was 3,038 BCF as of Friday, August 4th 2017, an increase of 28 BCF from previous week. Stocks were 275 BCF less than last year at this time and 61 BCF above the five-year average. At 3,038 BCF, total working gas is within the five-year historical range.

- September Natural Gas futures settled at $2.985, up $0.102 or +3.54%. So market is relying on increased demand due to warm weather.

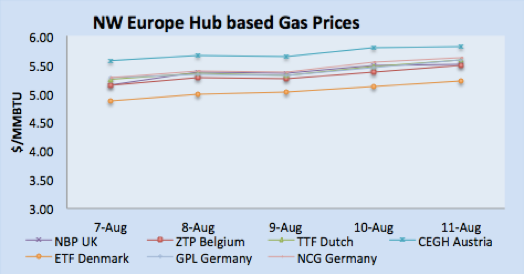

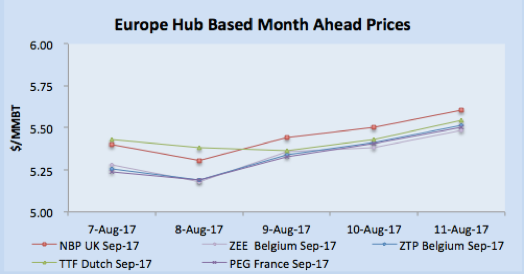

- NBP UK remained volatile through out the week due to due to Crude and coal prices along weather plus bearish power generation from renewables and nuclear units.

- Clouds have hampered renewables power generation plus two nuclear units, Dungeness and Hinkley.

- Weather is expected to be warmer next week in UK, plus unpredictable power generation from renewables is bullish factors for the prices.

- NBP UK day ahead prices closed 42.4490 Pence/Therm (equivalent $$5.51/MMBTU) on Friday, increased by 10.43% from last Friday of 38.4380 Pence/Therm.

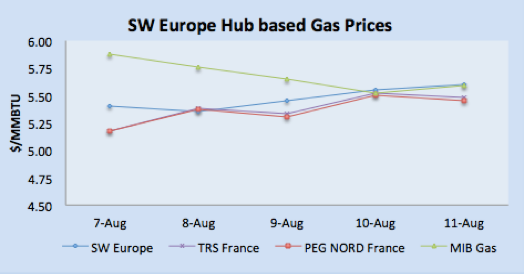

- Dutch and French gas prices remained range bound and moved up and down with Crude oil price trends.

- Overall supply in continental pipeline system remained adequate as flows from Russia and Norway normalized.

- Gas prices remained bearish in the Iberian Peninsula despite hot weather due to adequate supply.

- Two LNG cargoes expected to unload in UK by end August.

- TTF closed at €16.10/MWH (equivalent of $5.57/MMBTU), PEG Nord France closed at €15.75/MWH ($5.45/MMBTU), and Spanish at €16.15/MWH ($5.59/MMBTU) on Friday.

Currency

- USD fell against a basket of global currencies on Friday, primarily due to data on inflation and geopolitical tension between US and North Korea.

- Labor Department communicate that CPI (Consumer Price Index) edged up to 0.7% after remaining at 0.6% in June 2017.

- The depressed consumer inflation report is pointing to a continued slowdown in inflation, and reducing expectations the Federal Reserve may keep to its plan to hike rates at least once more this year.

- The S. DXY dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies, fell to 93.01 on Friday in comparison with last Friday level of 93.50.

- The rise in Euro and Sterling is primarily due to slump of USD. GBP/USD rose to $1.3004, whereas us EURO/USD rose to $1.1813.

- Inflation reports from Euro zone, German Inflation was in line with expectations and confirmed at 1.5% year over year in July, French inflation also subdued at 0.8% and Italian inflation reported to be 1.2% year on year, inline with expectations.

- British Pound is still a risky currency for investors as soft inflation and Brexit still bring the bearish pressure on the currency.

- USD/JPY fell to 109.07 as prevailing geopolitical tensions between US and North Korean is enhancing investors’ confidence on Yen.

- AUD/USD remained steady at 0.7878 on Friday, however US geopolitical tension escalation can support AUD against USD.

- Chinese Yuan also gained 1% in the region and stands at 6.67 on Friday.

Weather

- UK, Belgium and Netherland remained around 20oC and expected to be in the range of 20-25oC next week with some showers.

- France remained cooler around 20-25 oC, and expected to remain same next week.

- Hot weather in Spain & Portugal, temperature touched 40oC in Spain before cooling down to 30oC and Portugal remained between 30-35oC, Spain will be around 35oC whereas Portugal will be between 26-32oC in the coming week.

- Temperature in Argentina remained around between 16-18oC, and expected to be in the same range next week.

- Brazil remained hot with temperature around 25-30oC, and expected to remain hot next week.

- Mexico is getting warm with temperature around 25-30oC and expected to remain warm next week.

- Middle East region summer season in full swing with Egypt around 35oC, Kuwait 45oC plus, and UAE temperature reached 45oC and will remain the same next week.

- Indian Subcontinent in in monsoon season with temperature in Pakistan and India around 35oC, same weather profile for next week.

- Temperature remained hot in North East Asia, with temperature around 38oC in Taiwan, around 35oC in Korea, China 35oC, and Japan is around 30-32oC, weather is expected to cool down by couple of degrees but still hot weather prevailing in North East Asia.

- South East Asia already in hot weather, Thailand around 35oC, Indonesia and Malaysia ranging between 32oC, and will remain same next week.

- USA Weather: Overall weather is remained warm, overall its summer season and weather has entered into summer temperature profile.

LNG

- LNG prices in Asian market gained through out the week due to hot weather along with production issues and winter buying interest emergence.

- Production issues at Queensland Curtis, along with Peru export disruption and Trinidad Atlantic third production line out of commission is putting pressure along with two upcoming scheduled maintenances at NWS Australia.

- North Asia is in summer season and cooling demand increased has put pressure on utility buyers in Japan and Taiwan along with China.

- JKM Future curve market closed at $6.40/MMBTU for October, $6.70/MMBTU for November and $7.00/MMBTU for December, putting pressure on winter prices and buying.

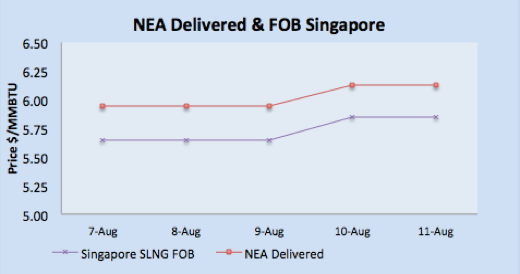

- Asian prices were heard to close on Friday with JKM $6.200/MMBTU, SLNG NEA Delivered at $6.130/MMBTU and FOB Singapore at $5.85/MMBTU,

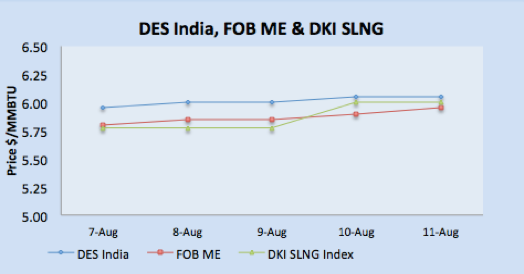

- Price sentiments in North Asian market has put pressure for the prices in Middle East and India as prices are up by $0.20/MMBTU and closed at $6.00/MMBTU for DKI SLNG Index on Friday.

- Demand for imported LNG in European markets is low, due to ample pipelined gas supply plus arrival and expected arrival of LNG vessels.

- Imported LNG offers in North West Europe were heard at $0.20 discount with NBP UK prices and around 25 cents discount to TTF. NBP UK closed at equivalent prices level of $5.51/MMBTU and TTF at $5.57/MMBTU.

- South Western gas prices were mixed as prices in France remained strong whereas in Spain and Portugal prices moved downward due to adequate pipeline supply. Imported LNG prices were heard at 20 cents discount with TTF September delivery prices.

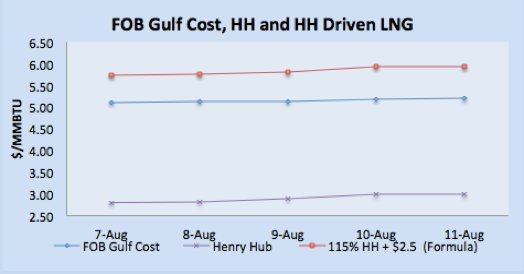

- Current Asian prices have become attractive for US producers as netback basis, North East Asian destination is at par with South American and European destination. Gulf Cost producers netback prices is in the range of $5.10-$5.30 per MMBTU basis.

- Bangladesh is expanding its gas portfolio options as it’s working on pipeline options beside LNG import terminals. Bangladesh Petroleum Corporation and Indian State run ONGC are in negotiation for building 6,900 KM pipeline that will connect Chittagong, Myanmar and North Eastern states of India for Mayanmar gas.

- Polish gas firm PGNiG expects to sign short and mid term contracts for liquefied natural gas by mid 2018 to take advantage of an expected supply glut.

Author’s Comments

- Short term impact of currencies are not weighting on LNG prices, however if USD keep on performing weak then buyers from North East Asia, Europe, Middle Eastern and Indian will like to take advantage of the situation specially when it’s a peak demand season due to hot weather in Asian market.

- Brent impact still insignificant on LNG and Natural gas prices, looking at spot prices, Brant based contractual prices are still higher for Asian customers, but gap is narrowing. Europe still enjoying better natural gas and LNG prices in comparison with Brent.

- Short-term prices outlook look bullish, however keeping in view supply resumption from Trinidad, NWS, Peru and Cheniere forth line commissioning, prices will remain under pressure once winter buying is over.

|

|

|

|

|

|

LNG Merchant Activity

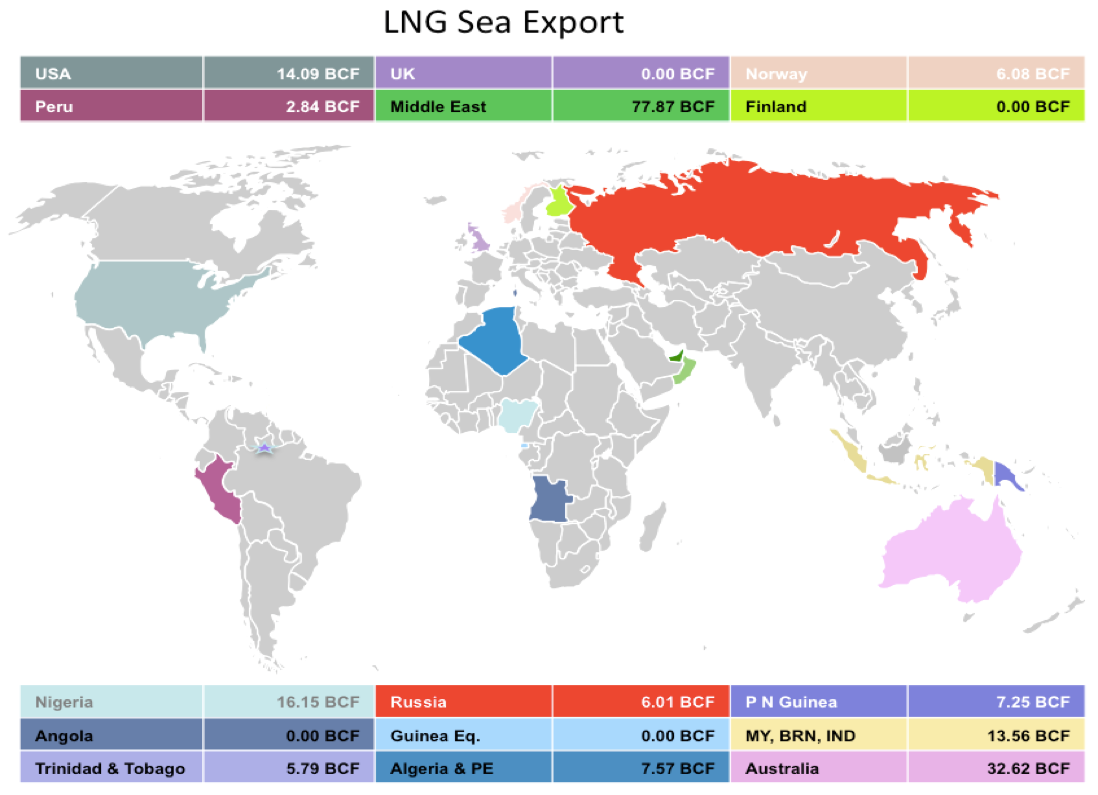

- 58 vessels carrying 3.73 million tons (204.60 BCF) loaded from various supply centres, a decrease by 0.29 million tons from last week.

- Primarily decrease in the quantities is from Nigeria, Trinidad, Oman and Angola in comparison from last week.

- 30 vessels carrying 2.41 million tons, have been dispatched from Ras Laffan, Qatar so far in the month of August, this represent 28% of total global trade for the first 11 days of August.

- 3 vessels left for Indian ports with 8.85 BCF and one for Pakistan carrying 2.95 BCF from Qatar.

- Five vessels carrying 16.15 BCF departed from Nigerian port for European, South American and Asian destinations.

- Algeria loaded two vessels carrying 3.06 BCF for Italy and Spain.

- Pont Fortin, Trinidad & Tobago loaded two vessels with 5.79 BCF

- Two vessel loaded from Brunei with load of 4.59 BCF.

- 10 vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China and Korea carrying 32.61 BCF.

- Two cargoes left for Spain and unknown location with 6.08 BCF from Norway

- Middle Eastern terminal at Das Island (UAE) loaded two vessels carrying 5.67 BCF for North East Asia.

| Departure Date | Vessel Name | Capacity(CBM) | Loading Port | Discharge Country | ETA Discharge Port | LNG (BCF) |

| 5-Aug-17 | GASLOG SARATOGA | 155,000 | Bonny, Nigeria | Indian Basin | 17-Aug-17 | 3.20 |

| 5-Aug-17 | GOLAR BEAR | 160,000 | Bonny, Nigeria | Not Known | 3.30 | |

| 8-Aug-17 | GDF SUEZ POINT FORTIN | 154,982 | Bonny, Nigeria | West Africa | 3.20 | |

| 10-Aug-17 | LNG RIVER ORASHI | 142,988 | Bonny, Nigeria | Not Known | 2.95 | |

| 5-Aug-17 | LNG ABALAMABIE | 170,000 | Bonny, Nigeria | Kuwait | 28-Aug-17 | 3.51 |

| 8-Aug-17 | GASLOG GIBRALTAR | 217,900 | Punta Europa | Not Known | 06-Sep-17 | 4.50 |

| 8-Aug-17 | CHEIKH BOUAMAMA | 74,425 | Skikda, Algeria | Italy | 10-Aug-17 | 1.54 |

| 6-Aug-17 | CHEIKH EL MOKRANI | 73,990 | Skikda, Algeria | Spain | 07-Aug-18 | 1.53 |

| 6-Aug-17 | HISPANIA SPIRIT | 137,814 | Pampa Melchorita, Peru | Not Known | 05-Sep-17 | 2.84 |

| 5-Aug-17 | SESTAO KNUTSEN | 135,357 | Point Fortin, Trinidad | Not Known | 24-Aug-17 | 2.79 |

| 6-Aug-17 | CELESTINE RIVER | 145,394 | Point Fortin, Trinidad | China | 04-Sep-17 | 3.00 |

| 5-Aug-17 | CLEAN OCEAN | 162,000 | Sabine Pass, USA | Not Known | 20-Aug-17 | 3.34 |

| 7-Aug-17 | SK SUMMIT | 135,933 | Sabine Pass, USA | Korea | 15-Sep-17 | 2.80 |

| 11-Aug-17 | RIOJA KNUTSEN | 176,300 | Sabine Pass, USA | Not Known | 3.64 | |

| 10-Aug-17 | GASLOG GENEVA | 209,000 | Sabine Pass, USA | Atlantic Basin | 20-Aug-17 | 4.31 |

| 6-Aug-17 | EKAPUTRA 1 | 136,400 | Bontang, Indonesia | Japan | 14-Aug-17 | 2.81 |

| 10-Aug-17 | STENA CLEAR SKY | 173,593 | Bontang, Indonesia | Japan | 3.58 | |

| 10-Aug-17 | SPIRIT OF HELA | 173,800 | Lese, Papua New Guinea | Japan | 18-Aug-17 | 3.59 |

| 7-Aug-17 | GRACE DAHLIA | 177,425 | Lese, Papua New Guinea | Pacific Basin | 22-Aug-17 | 3.66 |

| 5-Aug-17 | HYUNDAI UTOPIA | 125,182 | MIGAS LNG BATU, Indonesia | Japan | 11-Aug-17 | 2.58 |

| 6-Aug-17 | GRAND MEREYA | 145,964 | Prigorodnoye, Russia | Japan | 10-Aug-17 | 3.01 |

| 8-Aug-17 | CYGNUS PASSAGE | 145,400 | Prigorodnoye, Russia | Japan | 13-Aug-17 | 3.00 |

| 6-Aug-17 | BEBATIK | 75,056 | Sieria Oil Terminal, Brunei | Malaysia | 1.55 | |

| 9-Aug-17 | ARKAT | 147228 | Sieria Oil Terminal, Brunei | Not Known | 3.04 | |

| 8-Aug-17 | DAPENG MOON | 147,200 | Dampier, Australia | China | 15-Aug-17 | 3.04 |

| 6-Aug-17 | NORTHWEST SNIPE | 127,747 | Dampier, Australia | Japan | 16-Aug-17 | 2.64 |

| 11-Aug-17 | CLEAN PLANET | 162,000 | Dampier, Australia | Japan | 26-Aug-17 | 3.34 |

| 10-Aug-17 | ENERGY FRONTIER | 144,596 | Dampier, Australia | Japan | 19-Aug-17 | 2.98 |

| 11-Aug-17 | WOODSIDE ROGERS | 159,800 | Dampier, Australia | Pacific Basin | 25-Aug-17 | 3.30 |

| 8-Aug-17 | PACIFIC EURUS | 135,000 | Darwin, Australia | Japan | 22-Aug-17 | 2.79 |

| 5-Aug-17 | MARAN GAS POSIDONIA | 164,000 | Gladstone, Australia | Not Known | 15-Aug-17 | 3.38 |

| 10-Aug-17 | CESI QINGDAO | 205,000 | Gladstone, Australia | China | 21-Aug-17 | 4.23 |

| 6-Aug-17 | LNG KOLT | 210,000 | Gladstone, Australia | Korea | 17-Aug-17 | 4.33 |

| 7-Aug-17 | NORTHWEST STORMPETREL | 125,525 | Gladstone, Australia | Pacific Basin | 18-Aug-17 | 2.59 |

| 8-Aug-17 | ARCTIC AURORA | 154,800 | Melokya, Norway | Egypt | 3.19 | |

| 11-Aug-17 | ARCTIC VOYAGER | 140,071 | Melokya, Norway | Spain | 18-Aug-17 | 2.89 |

| 11-Aug-17 | ISH | 137,512 | Das, UAE | Not Known | 25-Aug-17 | 2.84 |

| 6-Aug-17 | AL KHAZNAH | 137,450 | Das, UAE | Japan | 22-Aug-17 | 2.84 |

| 6-Aug-17 | SIMAISMA | 142,971 | Ras Laffan, Qatar | Not Known | 2.95 | |

| 6-Aug-17 | AL JASSASIYA | 142988 | Ras Laffan, Qatar | Pakistan | 11-Aug-17 | 2.95 |

| 5-Aug-17 | GOLAR KELVIN | 162,000 | Ras Laffan, Qatar | Mediterian/Jordon | 12-Aug-17 | 3.34 |

| 8-Aug-17 | AL KHARSAAH | 211,885 | Ras Laffan, Qatar | Not Known | 4.37 | |

| 11-Aug-17 | AL GHASHAMIYA | 211,855 | Ras Laffan, Qatar | Not Known | 4.37 | |

| 11-Aug-17 | AL KHATTIYA | 205,993 | Ras Laffan, Qatar | Not Known | 16-Aug-17 | 4.25 |

| 5-Aug-17 | BW GDF SUEZ PARIS | 162,524 | Ras Laffan, Qatar | Argentina | 29-Aug-17 | 3.35 |

| 10-Aug-17 | AL THUMAMA | 216,325 | Ras Laffan, Qatar | Belgium | 31-Aug-17 | 4.46 |

| 7-Aug-17 | AL KARAANA | 205,988 | Ras Laffan, Qatar | Far East | 19-Aug-17 | 4.25 |

| 9-Aug-17 | AL NUAMAN | 205,981 | Ras Laffan, Qatar | Far East | 4.25 | |

| 7-Aug-17 | RAAHI | 138,077 | Ras Laffan, Qatar | India | 10-Aug-17 | 2.85 |

| 11-Aug-17 | DISHA | 136,026 | Ras Laffan, Qatar | India | 16-Aug-17 | 2.81 |

| 10-Aug-17 | ASEEM | 154,948 | Ras Laffan, Qatar | India | 13-Aug-17 | 3.20 |

| 8-Aug-17 | CORCOVADO LNG | 159,800 | Ras Laffan, Qatar | Indian Ocean | 16=-8-2017 | 3.30 |

| 5-Aug-17 | HYUNDAI ECOPIA | 146,790 | Ras Laffan, Qatar | Korea | 21-Aug-17 | 3.03 |

| 8-Aug-17 | AL HUWAILA | 214,716 | Ras Laffan, Qatar | Mediterian | 15-Aug-17 | 4.43 |

| 5-Aug-17 | ZARGA | 266,000 | Ras Laffan, Qatar | Mediterian | 22-Aug-17 | 5.49 |

| 5-Aug-17 | AL KHOR | 135,295 | Ras Laffan, Qatar | Singapore | 16-Aug-17 | 2.79 |

| 10-Aug-17 | AL RAYYAN | 134,671 | Ras Laffan, Qatar | Singapore | 20-Aug-17 | 2.78 |

| 5-Aug-17 | TAITAR NO. 4 | 144,596 | Ras Laffan, Qatar | Taiwan | 20-Aug-17 | 2.98 |