Market Analysis

Crude Oil

- Brent and WTI pries remained bullish through primarily based upon three major monthly reports, which depicted production cuts and demand growth along with comments from Saudi Arabia pertaining to extending production cut.

- OPEC monthly report stated a decline in production by 81,000BPD, which gave market the feeling about OPEC production, cut compliance.

- IEA projected a rise in demand in 2017 by 1.6 million BPD in comparison with 2016.

- OPEC reported also stated oil demand growth by 1.42 million BPD, attributing the growth expectation from OECD, Europe and China.

- EIA revised down, but still a demand growth by 1.35 million BPD, which is most conservative among all three projections.

- Brent price closed at $55.62/BBL on Friday, an increase by 3.42% from last Friday price of $54.49/BBL, whereas WTI closed at $49.89 on Friday, an increase of 5.08% from last week price of $47.48/BBL.

- Brent/WTI spread this Friday decreased to $5.73/BBL from last Friday spread of $6.30/BBL.

- OPEC largest product cut in the month of August though did bring bullish impact in the market, however, the major reduction was attributed to production issue in Libya due to militant activities.

- Saudi Arabia is focusing more on production cut compliance, as production cuts are not being translated into corresponding oil export numbers. This is the agenda item for next ministerial meeting scheduled for 22nd September 2017.

- Nigeria and Libya have pumped 608,000 BPD more than their combined level last October, and thus negating the production cut target by OPEC/Non OPEC countries.

- The production cut compliance is also questionable when it comes to Russian output, as the target was to reduce the production 300,000 BPD and against the target of 10.391 million BPD, Russian oil supply was recorded at 11.25 and 11.26 million BPD.

- EIA Weekly report reported a buildup of 5.8 million barrels with stock at 468.2 million barrel on 8th September 2017; against a market expectation of 4.0 million barrels build up.

- Gasoline inventories at 218.3 million barrel reported on 8th September 2017, recording 8.4 million draws on week on week basis.

- Refinery use fell a further 2.0% from last week of 16.9% decrease due to the continuing impact of outages as flooding caused substantial damage, although markets had been expecting a recovery in capacity use for the week.

- Baker Hughes rig count reported a decrease by 7 in oilrigs with total standing at 749, whereas gas rigs decreased by 1 now at 186, with a total number of rigs at 943, still 430 more rigs than last year.

- Short term oil prices seem bullish as demand from refineries expected to pick up as refineries are coming online after hurricanes Harvey and Irma and lower gasoline inventory level.

Natural Gas

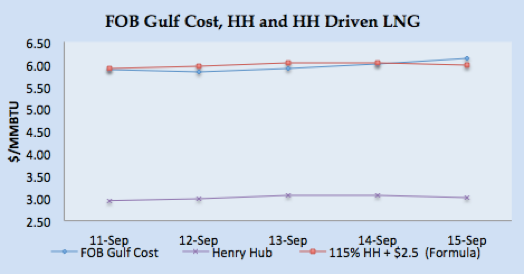

- Henry Hub prices closed at $3.02/MMBTU, up by 4.50% from last Friday, due to warmer than normal weather, which may trigger moderate to high natural gas consumption.

- Average total supply remained same as last week, averaging around 79.2 BCFD whereas consumption declined by 7% week on week basis due to demand destruction from Hurricane Irma. Demand from power generation decreased by 7% whereas, industrial sector consumption decreased by 1% week on week basis.

- Baker Hughes reported an increase in natural gas rigs by 1.

- US LNG export resumed post Hurricane Harvey from Sabine Pass with five vessels already departed.

- Working gas in storage was 3,311 BCF as of Friday, September 8th 2017, an increase of 91 BCF from the previous week, against an expectation of 85 BCF. This is the largest net injection since June 2017. Stocks were 179 BCF less than last year at this time and 43 BCF above the five-year average. At 3,311 BCF, total working gas is within the five-year historical range.

- October Natural Gas futures settled at $3.035/MMBTU, whereas $3.091/MMBTU for November & $3.242/MMBTU for December delivery on Friday, exhibiting stable to bullish tone.

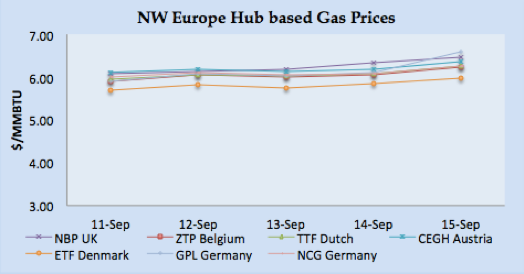

- Gas prices in the UK remain bullish during the week primarily due to system shortage due to supply issues at the pipeline, crude prices, environmental cost and reduced renewables power generation outlook.

- UK Gas system was short majority of week due to supply issues at Langeled & SEGAL pipeline.

- Rising Brent prices along with higher carbon and emission process are also weighing on NBP bullish run.

- Wind based power generation still looking strong, however solar is expected to be weak due to cloud cover and light rain forecast for next week, along with the resumption of gas through pipeline and LNG vessel arrival.

- NBP UK DA prices closed 47.7160 Pence/Therm (equivalent $$6.48/MMBTU) on Friday, increased by 3.84% from last Friday of 45.9536 Pence/Therm.

- NBP UK curve market for October and November closed at 45.0200 Pence/Therm & 48.0900 Pence/Therm ( the equivalent of $6.11/MMBTU & $6.53/MMBTU), a downward trend based upon Sterling performing well against Euro.

- Overall cooler temperature in France and Netherlands along with increased power generation cost due to higher crude and coal prices have kept European gas prices bullish. There has been maintenance at NORD Stream, which, is curtailing Russian gas flow, but the impact is not significant. There is one LNG vessel arriving on 6th October from the US.

- Gas Prices in Iberian Peninsula remained range bound as weather eased a bit and there is not significant increase in the demand.

- TTF closed at €17.83/MWH ( the equivalent of $6.25/MMBTU), PEG Nord France closed at €17.93/MWH ($6.28/MMBTU), and Spanish at €17.85/MWH ($6.26/MMBTU) on Friday.

- In the curve market, the prices impact were from Euro depreciation against Sterling, TTF November closed at €17.67/MWH ($6.19/MMBTU) and December at €17.93/MWH ($6.28/MMBTU).

- November & December PEG Nord forward prices closed at €18.12/MWH ($6.35/MMBTU) & €18.49/MWH ($6.48/MMBTU, defining the price direction for the winter season.

Currency

- Dollar remained weak through out the weak reasons attributed to Geo political tension, lower retail sales data, lower inflation and stronger Sterling performance.

- Investors assessed latest UN sanctions on North Korea as weak and believe that political risk still prevailing thus focusing more on other currencies that USD.

- GBP/USD went passed 1.3600 level since June 2016, as there are news on interest rate hike in near future along with removal of additional stimulus measures.

- Friday US retail sales data unexpectedly undershoot expectation for the month of August as retail sales dip 0.2% versus 0.1% rise expectation. Investors are lowering their expectation on third quarter economic growth.

- Weaker than expected wholesale inflation. Total PPI rose 0.2% in August against the expectation of 0.3% hike also dented the rate hike expectations and that kept USD demand uplifted for a day.

- The S. dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies, fell by 0.25% to 91.80.

- Euro has been volatile throughout the week, however not been able to cross 1.2000 level, and the pair has been continuing the pattern of alternating between gain and losses since last six weeks. Euro/USD closed at 1.1935 level on Friday.

- GBP remained bullish through out the week, as there is indication of interest rate hike along with withdrawal of some stimulus in coming months. GBP/USD closed at 1.3571 on Friday.

- Japanese Yen remained stable before sliding down as demand for safer currency eased after North Korea missile launch on Friday. USD/JPY closed at Y110.85 (JPB/USD 0.00902) on Friday.

- AUD/USD closed at 0.800078 on Friday, remained flat to weaker due to Asia stocks slipping due to disappointing Chinese out data.

- Chinese Yuan declined to 6.54395 on Friday, due to disappointing Chinese data, as China posted it slowest growth on fixed asset investment along with weaker industrial output and retail sales.

Weather

- UK, Germany, Belgium & Netherland weather remained below normal range around 15-20oC and expected to remain a bit warmer next week with cloud cover and light rain.

- France was cold this week around 16-18oC with cloud & light rain, and expected to be a warmer around 15-20oC with rain forecast.

- Weather easing a bit in Spain & Portugal with widening temperature range of 21- 31oC and expected to lower than the normal range around 22-28o.

- Temperature in Argentina remained around 16-23oC with some thunderstorm, and expected to be in the same range of 17-22o.

- Brazil remained hot with temperature around 28-30oC, and expected to remain around the same range next week.

- Mexico is getting warm with the temperature around 20-25oC and expected to be warmer next week around 25oC.

- Middle East region summer season still prevailing, with Egypt around 33-37oC and expected to be same next week, Kuwait 43-47oC and Dubai around 37-42oC, next week weather easing a bit with Kuwait around 38oC and Dubai around 39oC .

- Indian Subcontinent in summer season with temperature in Pakistan and India around 30-35oC, and expected to remain same next week.

- Temperature still hot in North East Asia, with temperature around 29-35oC in Taiwan, 24-28oC in Korea, China 25-30oC, and Japan is around 26-31o Weather expected to remain same next week, with Taiwan 32-34oC, Korea around 25-28oC, China 27-32oC & Japan 23-30oC.

- South East Asia already in hot weather, Thailand around 33-35oC, Indonesia and Malaysia around 30-33oC, and will remain same next week.

- USA Weather: Weather is warm in the East Coast while cooler than normal in the West Coast, weather is expected to be warmer than normal in the coming week.

LNG

- LNG prices remain bullish through out the week due to buying appetite in Asian market along with higher European gas hub prices and upward Brent and coal prices despite the fact that there is ample supply outlook.

- Asian LNG prices kept moving Northward as there was buying appetite from China and Korea for second half October delivery.

- On Supply side there is resumption of supply from Sabine pass as 5 vessels left Sabine Pass during the week, along with expectation of Australia’s Wheatstone coming into production from end September 2017.

- There are cargoes available heard from Australian and Indonesian projects for October loading.

- China’s appetite for LNG is increasing as Hebei, China vowed to meet 2017 air quality targets by switching to gas based power generation which will displaced 6 million tons of coal (equivalent of 3 MTPA of LNG)

- European Hub gas prices also contributing to LNG bullish run as US and African suppliers along with traders are focusing on European market for winter season, especially UK after the closure of Rough storage facility in UK.

- Asian prices maintained its bullish trend since 10th July 2017 and price closure on Friday were; JKM at $7.0500/MMBTU, SLNG NEA Delivered at $6.6810/MMBTU and FOB Singapore at $6.4670/MMBTU.

- Indian buyers are in the market for November delivery and based upon FOB Singapore and Middle East, DES India is calculated around $6.65- $6.85/MMBTU level. DKI SLNG Index on Friday reported at $6.4880/MMBTU.

- JKM Future curve market closed at $7.500/MMBTU, $8.0500/MMBTU & $8.2500/MMBTU for November, December 2017 & January 2018 delivery respectively, suggesting the market in contango due to winter season approaching.

- European hub curve prices remained bullish through out the week due to crude price bullish run, weather outlook and emission prices. European gas curve prices for November onward depicting a bullish sentiment.

- North West Europe prices were estimated to be around $5.8656/MMBTU (96% of NBP UK October price). For Netherland market the imported LNG prices are estimated at 15 cents discount of TTF October price of $6.03/MMBTU level.

- South Western gas prices were stable, as hot weather plus Norwegian maintenance and poor LNG outlook has put pressure on the prices. PEG Nord closed at €61/MWH ($5.86/MMBTU) whereas Iberian Peninsula prices closed at €17.25/MWH ($6.09/MMBTU) on Friday.

- South West Europe imported LNG prices were estimated at 5 cents discount to PEG NORD October future, calculated to come around $6.05/MMBTU level.

- Iberian Peninsula prices closed at $6.62/MMBTU level and based upon estimated regasification charges of $0.50/MMBTU, desired level seems to be $6.10/MMBTU.

- US Gulf Coast producer price on FOB basis for October delivery on Friday based upon NBP October price comes around $5.610/MMBTU whereas for November delivery it is $6.030/MMBTU. This is based NBP curve price for October and November.

- Based upon November future price for North East Asia region, the estimated price for US Gulf Coast producer is coming around $6.35/MMBTU for November, opening an arbitrage for US producers for Asian market.

- Reloading cargo from European LNG terminal is calculated based upon Algerian FOB price for Spanish, UK and French destinations and its coming around in the range of $5.95/MMBTU – $6.05/MMBTU for October delivery.

Author’s Comments

- LNG prices are entering the winter season and all factors contributing to LNG prices for November onward are bullish.

- Supply seems adequate, however, demand is also picking up especially European destinations. Chinese demand will also play an important role for the winter season. However, price upward direction is limited, as there is ample supply availability and Brent price upward movement is also uncertain.

|

|

|

|

|

|

LNG Merchant Activity

LNG merchant data is developed in collaboration with Clipper Data LLC.

- 74 vessels carrying 4.52 million tons (217.51 BCF) loaded from various supply centres, during the week from 9th September 2017 till 15th September 2017.

- Primarily increase is from Qatar and USA.

- Month to date 37 vessels carrying 2.50 million tons have been dispatched from Ras Laffan, Qatar, this represents 31.70% of total global trade

- 20 Vessels left from Qatar carrying 64.46 BCF for India, Korea, Japan and Europe.

- Five vessels carrying 14.15 BCF departed from Nigerian port, for Middle East, Europe and South America.

- Algeria loaded five vessels carrying 10.03 BCF for Italy, Spain, Turkey and Egypt.

- Pont Fortin, Trinidad & Tobago loaded three vessels with 8.22 BCF for Puerto Rico and Spain.

- Two vessels loaded from Brunei with load of 5.49 BCF for Korea and Taiwan

- Twelve vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for India, Taiwan, China and Korea carrying 36.86 BCF.

- One cargo left for France with 2.87 BCF from Norway.

- Middle Eastern terminal at Das (UAE) and Qalhat (Oman) loaded 4 vessels carrying 10.64 BCF for India, Japan and Korea.

| Departure Date | Vessel Name | Loading Port | Loading Country | Discharge Country | ETA Discharge Port | LNG (BCF) |

| 15-Sep-17 | ESSHU MARU | Arzew | Algeria | Egypt | 19-Sep-17 | 3.02 |

| 12-Sep-17 | Berge Arzew | Arzew | Algeria | Turkey | 30-Sep-17 | 2.69 |

| 9-Sep-17 | Cheikh El Mokrani | Skikda | Algeria | Italy | 15-Sep-17 | 1.44 |

| 9-Sep-17 | Gdf Suez Global Energy | Skikda | Algeria | Italy | 18-Sep-17 | 1.44 |

| 12-Sep-17 | Cheikh Bouamama | Skikda | Algeria | Spain | 15-Sep-17 | 1.45 |

| 13-Sep-17 | Malanje | Soyo | Angola | Not Known | 01-Oct-17 | 3.01 |

| 9-Sep-17 | Prachi | BARROW ISLAND | Australia | India | 27-Sep-17 | 3.36 |

| 14-Sep-17 | Dapeng Moon | Dampier | Australia | China | 22-Sep-17 | 2.86 |

| 13-Sep-17 | Fuji LNG | Dampier | Australia | India | 01-Oct-17 | 2.81 |

| 14-Sep-17 | Energy Horizon | Dampier | Australia | Japan | 22-Sep-17 | 3.45 |

| 11-Sep-17 | Northwest Sanderling | Dampier | Australia | Taiwan | 26-Sep-17 | 2.44 |

| 13-Sep-17 | Amadi | Darwin | Australia | Not Known | 22-Oct-17 | 3.01 |

| 10-Sep-17 | Barcelona Knutsen | Gladstone | Australia | China | 24-Sep-17 | 3.37 |

| 11-Sep-17 | Cesi Gladstone | Gladstone | Australia | China | 22-Sep-17 | 3.38 |

| 13-Sep-17 | Cool Explorer | Gladstone | Australia | China | 25-Sep-17 | 3.11 |

| 10-Sep-17 | Hyundai Ecopia | Gladstone | Australia | Korea | 22-Sep-17 | 2.85 |

| 14-Sep-17 | Maran Gas Roxana | Gladstone | Australia | Korea | 27-Sep-17 | 3.37 |

| 15-Sep-17 | METHANE RITA ANDREA | Gladstone | Australia | Pacific Basin | 27-Sep-17 | 2.82 |

| 13-Sep-17 | Arkat | Seria Oil Terminal | Brunei | Korea | 16-Sep-17 | 2.86 |

| 11-Sep-17 | Abadi | Seria Oil Terminal | Brunei | Taiwan | 19-Sep-17 | 2.63 |

| 11-Sep-17 | Gdf Suez Cape Ann | Alexandria | Egypt | Singapore | 16-Sep-17 | 2.82 |

| 13-Sep-17 | Yenisei River | Punta Europa | Equatorial Guniea | China | 29-Sep-17 | 3.01 |

| 11-Sep-17 | Tangguh Jaya | Bitung | Indonesia | Singapore | 22-Sep-17 | 3.01 |

| 11-Sep-17 | Senshu Maru | Bontang | Indonesia | Japan | 19-Sep-17 | 2.45 |

| 14-Sep-17 | Golar Mazo | Bontang | Indonesia | Taiwan | 18-Sep-17 | 2.63 |

| 10-Sep-17 | Puteri Nilam | Bintulu | Malaysia | Japan | 18-Sep-17 | 2.48 |

| 9-Sep-17 | Puteri Nilam Satu | Bintulu | Malaysia | Japan | 19-Sep-17 | 2.62 |

| 14-Sep-17 | Seri Ayu | Bintulu | Malaysia | Japan | 21-Sep-17 | 2.79 |

| 11-Sep-17 | Hyundai Greenpia | Bintulu | Malaysia | Korea | 19-Sep-17 | 2.43 |

| 10-Sep-17 | LNG Benue | Bonny | Nigeria | Argentina | 23-Sep-17 | 2.78 |

| 9-Sep-17 | Lng Ogun | Bonny | Nigeria | France | 19-Sep-17 | 2.91 |

| 14-Sep-17 | LNG Borno | Bonny | Nigeria | Kuwait | 09-Oct-17 | 2.91 |

| 12-Sep-17 | LNG Adamawa | Bonny | Nigeria | Mexico | 28-Sep-17 | 2.77 |

| 13-Sep-17 | LNG Cross River | Bonny | Nigeria | Spain | 23-Sep-17 | 2.77 |

| 12-Sep-17 | Arctic Lady | Melkoya | Norway | France | 19-Sep-17 | 2.87 |

| 10-Sep-17 | LNG Jamal | Qalhat | Oman | Japan | 24-Sep-17 | 2.66 |

| 13-Sep-17 | Hanjin Muscat | Qalhat | Oman | Korea | 25-Sep-17 | 2.69 |

| 13-Sep-17 | Pacific Arcadia | Lese | Papua New Guinea | Japan | 23-Sep-17 | 2.83 |

| 10-Sep-17 | Kumul | Lese | Papua New Guinea | Taiwan | 21-Sep-17 | 3.34 |

| 12-Sep-17 | Al Ghuwairiya | Ras Laffan | Qatar | China | 01-Oct-17 | 5.02 |

| 9-Sep-17 | Gaslog Saratoga | Ras Laffan | Qatar | France | 25-Sep-17 | 3.01 |

| 13-Sep-17 | Aseem | Ras Laffan | Qatar | India | 17-Sep-17 | 3.01 |

| 10-Sep-17 | Raahi | Ras Laffan | Qatar | India | 13-Sep-17 | 2.69 |

| 15-Sep-17 | MARAN GAS ASCLEPIUS | Ras Laffan | Qatar | India | 18-Sep-17 | 2.78 |

| 11-Sep-17 | Al Khor | Ras Laffan | Qatar | Japan | 29-Sep-17 | 2.63 |

| 14-Sep-17 | Al Rayyan | Ras Laffan | Qatar | Japan | 30-Sep-17 | 2.62 |

| 9-Sep-17 | Al Sahla | Ras Laffan | Qatar | Japan | 30-Sep-17 | 4.12 |

| 15-Sep-17 | AL HAMLA | Ras Laffan | Qatar | Japan | 03-Oct-17 | 4.12 |

| 15-Sep-17 | AL WAJBAH | Ras Laffan | Qatar | Japan | 02-Oct-17 | 2.62 |

| 14-Sep-17 | K.Freesia | Ras Laffan | Qatar | Korea | 28-Sep-17 | 2.68 |

| 13-Sep-17 | Gaslog Seattle | Ras Laffan | Qatar | Kuwait | 18-Sep-17 | 3.01 |

| 11-Sep-17 | Mozah | Ras Laffan | Qatar | Mediterian | 16-Sep-17 | 5.09 |

| 12-Sep-17 | Lusail | Ras Laffan | Qatar | Not Known | 12-Sep-17 | 2.78 |

| 10-Sep-17 | Al Jassasiya | Ras Laffan | Qatar | Pakistan | 15-Sep-17 | 2.78 |

| 13-Sep-17 | Al Thakhira | Ras Laffan | Qatar | Singapore | 25-Sep-17 | 2.79 |

| 12-Sep-17 | Ejnan | Ras Laffan | Qatar | Taiwan | 25-Sep-17 | 2.80 |

| 9-Sep-17 | Taitar No.1 | Ras Laffan | Qatar | Taiwan | 23-Sep-17 | 3.01 |

| 14-Sep-17 | Taitar No.2 | Ras Laffan | Qatar | Taiwan | 26-Sep-17 | 2.81 |

| 11-Sep-17 | Al Safliya | Ras Laffan | Qatar | Thailand | 23-Sep-17 | 4.09 |

| 11-Sep-17 | Cygnus Passage | Prigorodnoye | Russia | Japan | 20-Sep-17 | 2.83 |

| 11-Sep-17 | Grand Aniva | Prigorodnoye | Russia | Taiwan | 20-Sep-17 | 2.82 |

| 9-Sep-17 | Grand Mereya | Prigorodnoye | Russia | Taiwan | 12-Sep-17 | 2.84 |

| 15-Sep-17 | STENA BLUE SKY | Prigorodnoye | Russia | Taiwan | 22-Sep-17 | 2.78 |

| 9-Sep-17 | Sevilla Knutsen | Singapore | Singapore | Not Known | 10-Oct-17 | 3.37 |

| 13-Sep-17 | Madrid Spirit | Point Fortin | Trinidad & Tobago | Not Known | 01-Oct-17 | 2.63 |

| 12-Sep-17 | Iberica Knutsen | Point Fortin | Trinidad & Tobago | Puerto Rico | 25-Sep-17 | 2.63 |

| 14-Sep-17 | British Diamond | Point Fortin | Trinidad & Tobago | Spain | 24-Sep-17 | 2.95 |

| 14-Sep-17 | Mubaraz | DAS | UAE | India | 21-Sep-17 | 2.63 |

| 9-Sep-17 | Al Hamra | DAS | UAE | Japan | 26-Sep-17 | 2.66 |

| 11-Sep-17 | Hyundai Peacepia | Sabine Pass | USA | Korea | 22-Oct-17 | 4.03 |

| 14-Sep-17 | Ribera Del Duero Knutsen | Sabine Pass | USA | Netherland | 06-Oct-17 | 3.37 |

| 12-Sep-17 | Golar Penguin | Sabine Pass | USA | Not Known | 3.11 | |

| 13-Sep-17 | Maran Gas Achilles | Sabine Pass | USA | Not Known | 28-Sep-17 | 3.38 |

| 10-Sep-17 | Methane Jane Elizabeth | Sabine Pass | USA | Not Known | 07-Oct-17 | 2.82 |

| Total | 217.51 | |||||