LNG Natural Gas Market Update – 28th August – 1st September 2017

8mins read

Market Analysis

Crude Oil

Brent and WTI pries remained bearish in the first half of the week, and then recovered in the second half.

Market is still weighing the impact of Hurricane Harvey as 25% of US refining capacity are down.

However long term outlook is still bearish as US production was expected to rise to 10 million barrels per day by end of the year.

Hurricane Harvey has impacted the gasoline prices in North America as US is forced to use it strategic reserves.

Latest report from OPEC suggest that oil output has fallen by 170,000 BPD in August due to production cut in Libya along with Iraq and KSA stepping up production cut compliance.

Brent price closed at $52.75, increased by 0.64% from Monday, whereas WTI closed at $47.29, rose by 1.55% from Monday price of $46.57/BBL.

EIA Weekly report reported a draw of 5.4 million barrels with stock at 457.8 million barrel on 25th August 2017; against a market expectation of 1.9 million barrels.

Gasoline inventories at 229.9 million barrel reported on 25th August 2017, inventory decreased by 35,000 barrels on week on week basis.

Baker Hughes rig count reported no change in oilrigs with total standing at 759, whereas gas rig increased by 3 and now at 183, with total number of rigs at 943.

Natural Gas

Henry Hub prices closed at $3.07/MMBTU, up by 6.23% from last Friday, as traders resumed their focus on weather.

Weather is expected to be warmer than normal, as South West, South East, Mid West and Pacific region is in peak hot summer and enhanced cooling demand is a bullish factor contributing to gas demand.

Tropical storm Harvey affected both offshore (down by 0.6 Bcf/d Wednesday) and onshore (down by 3 Bcf/d last Saturday) natural gas production.

US LNG export suspended from Sabine Pass due to hurricane Harvey.

EIA showed domestic supplies of natural gas fell by 2% in comparison with last week, averaging 77.2 BCFD, whereas demand decreased by 10% compared to last week with residential and commercial sector decreased by 7% and export to Mexico decrease by 11%.

Working gas in storage was 3,155 BCF as of Friday, August 25th 2017, an increase of 30 BCF from previous week and expectations were of 32 BCF increase. Stocks were 239 BCF less than last year at this time and 8 BCF above the five-year average. At 3,155 BCF, total working gas is within the five-year historical range.

October Natural Gas futures settled at $3.065/MMBTU, whereas $3.128/MMBTU for November delivery on Friday, defining the direction for winter prices.

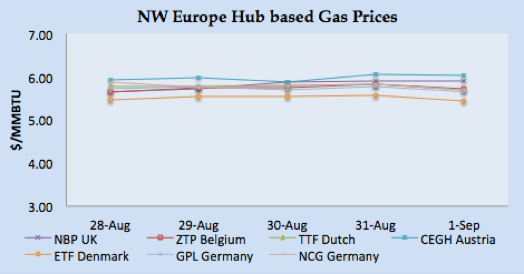

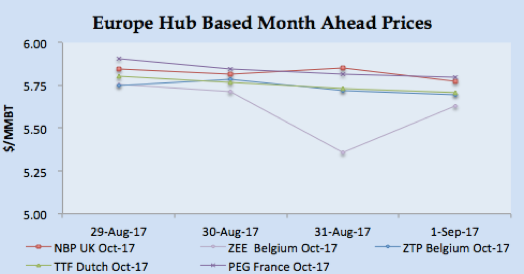

NBP UK remained bullish through out the week due to reduction of supply from Norway and South Hook terminal along with low wind generation forecast.

The outlook for imported LNG is weak for the remaining year along with Norwegian maintenance in September.

NBP UK day ahead prices closed 45.4850 Pence/Therm (equivalent $$5.89/MMBTU) on Friday, increased by 1.5% from last Friday of 44.8120 Pence/Therm.

NBP UK curve market for October and November closed at 44.5900 Pence/Therm & 47.6500 Pence/Therm (equivalent of $5.77/MMBTU & $6.17/MMBTU), putting bullish trend on prices and making it attractive for spot LNG offers from US.

Dutch & French market also remained short during the week due to Norwegian unplanned outage along with weak LNG supply outlook.

Gas Prices in Iberian Peninsula were bullish through out the week due to hot weather and low outlook of hydro power generation due to low water level in Spain.

TTF closed at €16.36/MWH (equivalent of $5.69/MMBTU), PEG Nord France closed at €16.51/MWH ($5.74/MMBTU), and Spanish at €17.45/MWH ($6.07/MMBTU) on Friday.

In the curve market TTF November closed at €16.99/MWH ($5.91/MMBTU) and December at €17.17/MWH ($5.71/MMBTU), PEG Nord at €17.37/MWH ($6.04/MMBTU) & €17.57/MWH ($6.11/MMBTU) and Spanish for Month Ahead €18.25/MWH ($6.36/MMBTU), defining the price direction for winter season.

Currency

USD steadied on Friday on better than expected manufacturing data despite weaker data from the job market.

In the month of August 156,000 jobs were created against an estimate of 180,000 jobs, resulting in jobless rate increased by 4.4%, and this data may put Fed thinking before considering any interest hike.

The Institute for Supply Management reported August’s manufacturing index jumping to 58.8% from 56.3% in July., highest since April 2011.

The S. dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies, rose by 0.14% to 92.72.

Euro started strong against USD at the stat of the week, as last week Yellen and Draghi didn’t speak much about monetary policy and market forces took over and EURO/USD pair moved around 1.20 level.

However stronger US manufacturing data brought USD back in action and on Friday, EURO/USD closed at 1.1859 from 1.2025 on Monday.

GBP performed strongly against USD and Euro due to likelihood of both US and Euro-Zone may not opt tighter monetary policy plus stronger UK manufacturing data. GBP/USD closed at 1.2954 on Friday.

Friday’s purchasing managers’ index for UK manufacturing sector was considerably stronger than expectation. PMI rose to 56.9 in August from 55.1 in July and against an expectation of fall to 55.

USD/JPY rose to 110.236 on Friday. The pair remained volatile as due to Korean missile launching over Japan, however recovery in US Treasury yields gave the boost to investor sentiments.

AUD/USD closed stronger due to US Treasury Bond yield increase along with weaker job report from US. AUD/USD settled at 0.7966 on Friday.

Chinese Yuan closed at 6.55 on Friday.

Weather

UK & Belgium weather was warm with temperature around 20-31oC and expected to be cooler around 18-22o.

Netherland weather remained between 19-27oC, and expected to be cooler around 20o.

France remained warm this week with temperature around 27-31oC, and expected to be cooler next week around 19-23o.

Hot weather prevailing in Spain & Portugal with temperature around 30oC plus and expected to remain same next week.

Temperature in Argentina remained around 16-22oC, and expected to be the same for the next week.

Brazil remained hot with temperature around 30oC, and expected to remain around the same range next week.

Mexico is getting warm with temperature around 20-24oC and expected to remain same next week.

Middle East region summer season still prevailing however easing a bit, with Egypt around 35oC and be same next week before easing to 33oC, Kuwait 47oC and Dubai around 45oC, next week weather easing a bit with Kuwait around 43oC and Dubai around 40oC .

Indian Subcontinent in in monsoon season with temperature in Pakistan and India around 30-35oC, and expected to remain same next week.

Temperature eased a bit but still hot in North East Asia, with the temperature around 34-36oC in Taiwan, 25-28oC in Korea, China 25oC Plus, and Japan is around 28-32o Weather expected to ease a bit little next week.

South East Asia already in hot weather, Thailand around 32oC, Indonesia and Malaysia around 33oC, and will remain same next week.

USA Weather: Overall weather is remained warm, with South West, South East, Mid West and Pacific region in hot peak summer.

LNG

LNG prices in Asia remained weak in comparison with last week prices, however, climbed for a couple of days as there was news of one transaction in Japan concluded around $6.25 level mark.

Stocks are high in Japan as due to hot weather Japanese utilities secure more than required cargoes.

Asian market participants have opted for wait-and-see mode as supply is expected to be long in September.

On supply side, Australia Wheatstone is expected to load cargoes in September along with three vessels waiting at Sabine Pass for loading.

Cargoes for September delivery from Algeria, Russian and Gorgon Australia in the market.

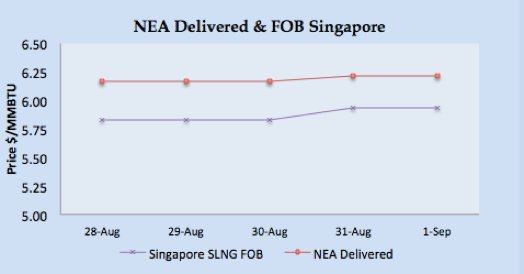

Asian prices were heard to close at JKM $6.150/MMBTU, SLNG NEA Delivered at $6.2190/MMBTU and FOB Singapore at $5.9320/MMBTU, lower than last week prices.

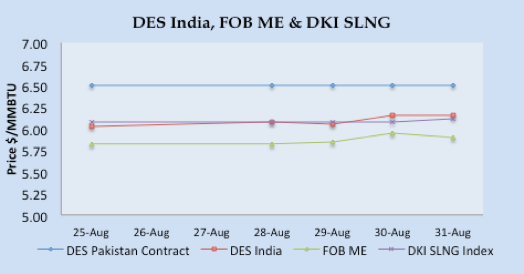

Indian buyers are also on the side-line and based upon FOB Singapore, DES India is calculated around $6.15/MMBTU level. DKI SLNG Index on Friday reported at $6.1230/MMBTU.

JKM Future curve market closed at $6.70/MMBTU, $7.145/MMBTU & $7.375/MMBTU for November 2017, December 2017 & January 2018 respectively. Future prices direction is based upon winter procurement.

Demand for gas is high in the European market as reduced pipeline gas from Norway, reduced LNG import outlook along with lower renewable power generation are the bullish factor.

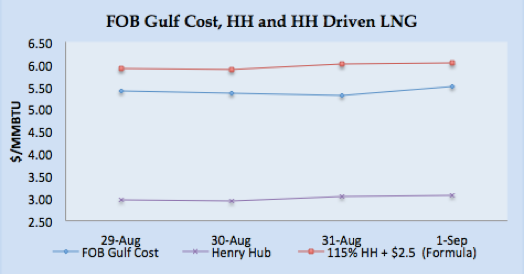

For North West Europe imported LNG prices assumed based upon 96% of NBP UK October prices, which comes around $5.5392/MMBTU. For Netherland market, the imported LNG prices are estimated at 15 cents discount of TTF October prices.

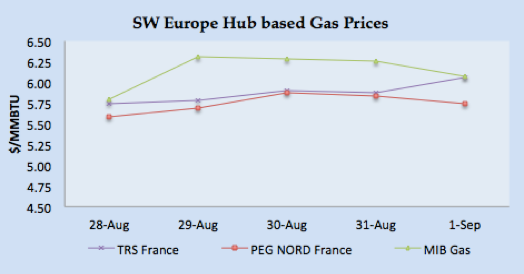

South Western gas prices were mixed as in France prices remained volatile as hot weather plus Norwegian gas pipeline outage has put pressure on the prices and PEG Nord closed at €51/MWH ($5.74/MMBTU) whereas Iberian Peninsula prices closed at €17.45/MWH ($6.06/MMBTU) on Friday. Spanish prices are high due to lower hydro-based power generation.

Based upon November future price for North East Asia and European destinations, US Gulf Coast manufacturers prices are coming around $5.50/MMTU level.

FOB EAM prices based upon DES Spanish from Algeria and Nigeria is calculated to be around $5.75 level mark on Friday.

Small scale LNG is evolving and more focus have been observed with Nigeria launching a scheme on transporting LNG to regions not linked with pipelines and focus on reduction of power generation via diesel.

USA is also proposing a speed up the approval process for small-scale LNG export to South American, the Caribbean and Central American regions.

Author’s Comments

Crude oil price is right now irrelevant to LNG spot prices and long term outlook is though bullish but still, Brent based prices are higher than spot prices. Brent prices of $45 or lower will be attractive for LNG buyer, however, for winter procurement LNG prices are being determined based upon European curve market. Looking at number of transaction for European gas market TTF seems to be the benchmark for winter procurement and End October price outlook seems bullish for European and Asian destination

LNG Merchant Activity

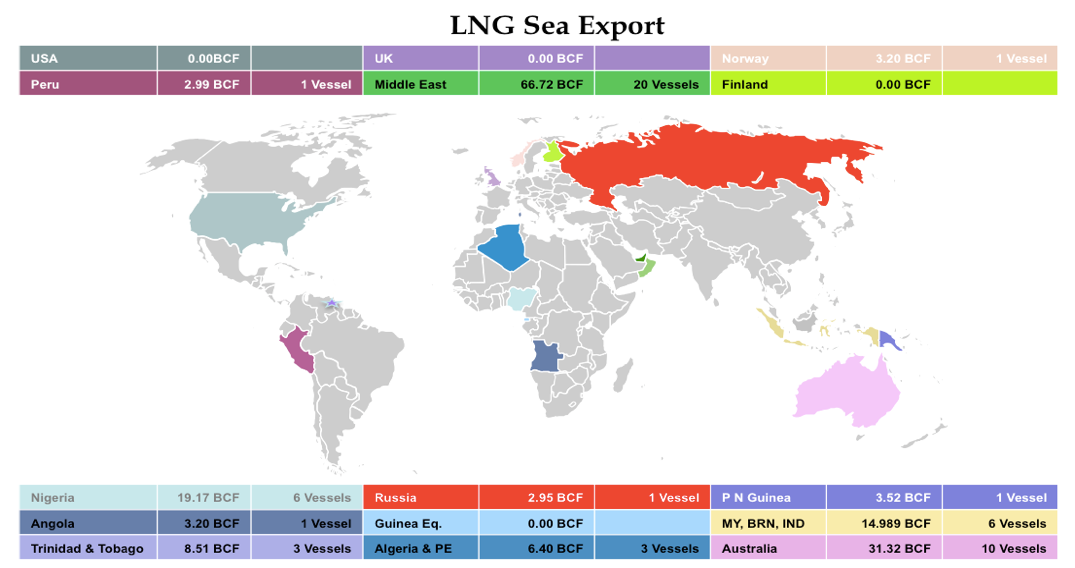

54 vessels carrying 3.19 million tons (162.96 BCF) loaded from various supply centres, an increase by 0.44 million tons from last week.

Primarily decrease in the quantities is from USA and Qatar.

82 vessels carrying 5.71 million tons, have been dispatched from Ras Laffan, Qatar in the month of August, this represent 35% of total global trade

5 vessels left for Indian ports with 16.20 BCF from 4 from Qatar and one from Nigeria.

Two vessels carrying 5.90 BCF for Pakistan from Qatar.

Six vessels carrying 19.17 BCF departed from Nigerian port, two for European destination and one for India.

Algeria loaded two vessels carrying 3.06 BCF for Italy and Spain.

Pont Fortin, Trinidad & Tobago loaded three vessels with 8.51 BCF, two cargoes destined for South Americas and one for a European destination.

Two vessels loaded from Brunei with load of 5.83 BCF.

Ten vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China and Korea carrying 31.32 BCF.

One cargoes left for Denmark with 3.05 BCF from Norway.

Middle Eastern terminal at Qalhat (Oman) loaded two vessels carrying 5.90 BCF for Korea and one unknown destination.