Market Analysis

Crude Oil

- Crude oil prices had a range bound bullish run throughout the week due to ongoing crises in the Middle East.

- Armed conflict between Iraq and Kurdistan has reduced the flow coming out of Kurdistan from 600,000 BPD to 216,000 BPD.

- The market is also expecting an extension of OPEC production cut deal for next nine month.

- Production is still on the rise from the US, though the rate of increase is slowing down.

- All above factors are aggregating towards a stable bullish run for crude in the long run, however upside is limited as past $60 BBL mark we can see shale gas producer more in action.

- October 13th 2017 EIA report depicted an increase in US crude export oil to 1.79 million barrel per day from last week 1.27 million barrels a day, Brent-WTI spread this week remained between $5.94-$6.28/BBL.

- Brent prices closed on $57.23/BBL on Friday, while WTI closed at $51.47/BBL at CME.

- Brent future depicting strength and closed at $57.89/BBL, $57.67/BBL & $57.44/BBL for December, January & February 2018 respectively.

- CME WTI curve market closed on Friday at $52.07/BBL for December, $52.55/BBL for January and $52.37/BBL for February.

- EIA Weekly report reported a draw of 5.7 million barrels with stock at 456.5 million barrel on 13th October 2017; against a market expectation of 4.2 million barrels drawdown.

- Gasoline inventories at 222.3 million barrel reported on 13th October 2017, recording 0.9 million barrels build-up against a market expectation of 0.25 million barrels draw down on week on week basis.

- Baker Hughes rig count reported a decrease by 7 in oilrigs, with total standing at 736.

- Overall situation seems supporting for crude prices to remain at current level, Brent-WTI spread though needs to be monitored carefully.

NATURAL GAS

- Henry Hub prices kept moving up and down and touched $3.00/MMBTU level only once in a week before closing at $2.92/MMBTU on Friday, the bearish run is due to overall mild weather except for Midwest, which has demand for air-conditioning and Northern states where there is demand for heating.

- Baker Hughes reported a decrease in natural gas rigs by 2 and total number stands at 185.

- Working gas in storage was 3,646 BCF as of Friday, October 13th 2017, an increase of 51 BCF from the previous week, against an expectation of 50 BCF.

- CME Henry Hub future on Friday closed at $2.91/MMBTU for November, $3.10/MMBTU for December and $3.23/MMBTU for January 2018, depicting weakness in the price.

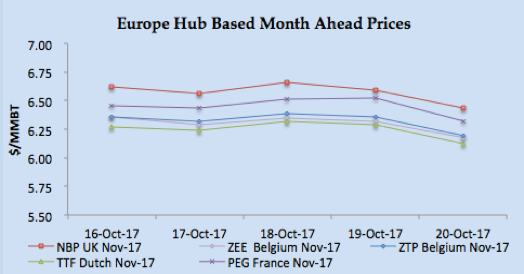

- European hub prices remained mixed, as the main factor has been weather and wind as pipeline gas supply from Norway and Russia is adequate. Prices taking direction from oil and coal prices along with weather spikes.

- NBP UK Day Ahead price closed at 44.33 Pence/Therm ($5.85/MMBTU) on Friday, increased by 2.65% from last Friday.

- NBP UK curve market remained range bound majority of the week before closing down at 48.79 Pence/Therm ($6.43/MMBTU) & 50.99 Pence/Therm ($6.72/MMBTU) for November & December respectively on Friday.

- TTF Day Ahead closed at €16.48/MWH ( the equivalent of $5.69/MMBTU), PEG Nord France closed at €16.59/MWH ($5.99/MMBTU) on Friday, depicting bearish tone.

- TTF November at €17.73/MWH ($6.12/MMBTU) and December at €18.05/MWH ($6.23/MMBTU) on Friday, reduced from last week.

- Spain and Portugal weather is easing and bearish factor for demand and prices, price remained stable in Iberian gas market and closed at €20.70/MWH ($7.15/MMBTU).

- November & December PEG Nord forward prices closed downward at €18.31/MWH ($6.32/MMBTU) & €18.73/MWH ($6.47/MMBTU) on Friday.

Currency

- Dollar remained volatile throughout the week on positive news on US industrial and production numbers, major tax reform discussion along with bearish factor being weak data from housing along with Fed new Chairman speculation.

- S. dollar index, measured against a trade-weighted basket of six major currencies closed at 93.66 on Friday.

- Euro remained strong throughout the week and had two spikes primarily on ECB meeting next week with an expected announcement on tapering off the asset stimulus program. Euro closed at 1.17189 on Friday after spiking to 1.18441 on Thursday.

- GBP/USD remained stable and range bound throughout the week, and closed at 1.31880.

- AUD/USD closed at 0.78182 on Friday, mixed throughout the week due to fluctuation in USD.

- Japanese Yen remained volatile and followed US Dollar direction, Friday YEN/USD closed at 0.00881 (113.511 USD/JPY).

- The People’s Bank of China set the Yuan parity rate against the dollar at 6.6092 on Friday, compared to the previous close of 6.6170.

Weather

- North West Europe; Weather remained mild in UK, Germany, Belgium and Netherland and the outlook is also for mild temperature, weather related demand is low.

- South West Europe: Spain and Portugal were warm in the beginning however eased off with France already in a mild temperature range, next week outlook is for mild weather.

- Latin America: Brazil is hot and expected to be hot next week, while Argentina this week remained mild with the same outlook for next week.

- Middle East still in hot weather with the same outlook for next week.

- South Asia: India and Pakistan mixed weather with demand is expected to be high due to the winter season.

- North East Asia: Taiwan still hot, however Japan, China and Korea remained mild but expected to be cold next week.

- South East Asia: Thailand, Indonesia and Malaysia still in hot weather and expected to remain same next week.

- North America: Mexico remained mild and expected to remain same next week.

- USA Weather: US weather seems mixed with demand only generated from Midwest for air-conditioning and Pacific North West for heating, rest of US is enjoying a mild weather.

LNG

- Global LNG prices turned bearish throughout the week after starting on Monday at higher price momentum from last week.

- The bearish tone is attributed to mild weather in Europe, adequate supply situation, the absence of Chinese buyer and focus on contract based LNG procurement.

- Weather in Europe is mild and has bearish impact on hub prices, there were price spikes in French market along with bullish Spanish market but eventually subsided due to regular pipeline supply from Norway and Russia.

- There is demand heard from India, Brazil and Turkey for December cargoes, however, buyers will now negotiate harder.

- There are spot supply tenders for November and December loading from Russia, Nigeria and Australia’s Wheatstone.

- Buyers in North East Asia have partially fulfilled their winter procurement demand and relying on contract based procurement. Last two weeks 27 vessels carrying 100.79 BCF discharged at China.

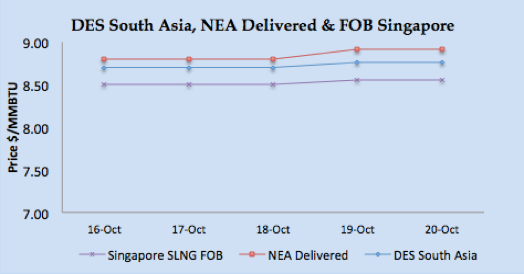

- Asian price closures on Friday were; SLNG NEA Delivered at $8.91/MMBTU and FOB Singapore at $8.56/MMBTU.

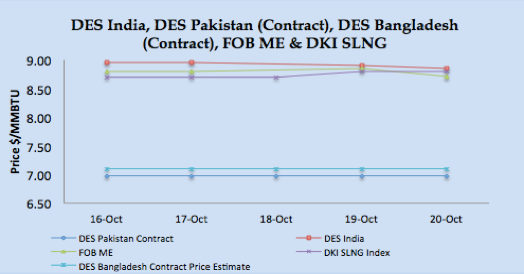

- Based upon FOB Singapore and the Middle East, DES India is calculated around $8.76/MMBTU level. DKI SLNG Index on Friday reported at $8.81MMBTU.

- JKM Future curve market jumped to $8.90/MMBTU, $9.00/MMBTU & $9.10/MMBTU for December 2017, January & February 2018 delivery respectively, depicting uncertainty in the market and expectation of winter spot procurement in coming weeks.

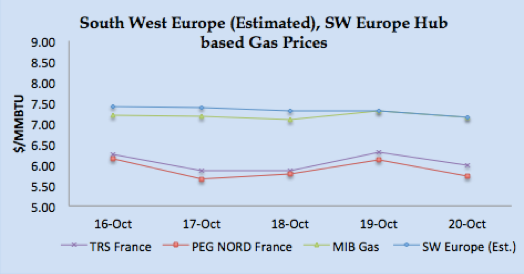

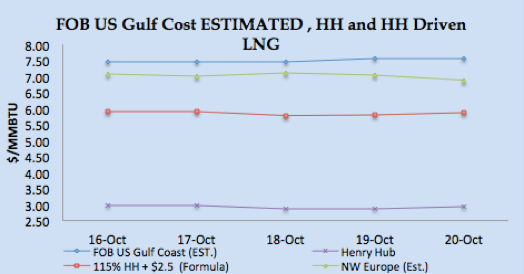

- The arbitrage window still open for reloads from European ports as netback based upon Chinese/Taiwanese destination still better than European prices, $7.40/MMBTU FOB is the price level from South West European ports.

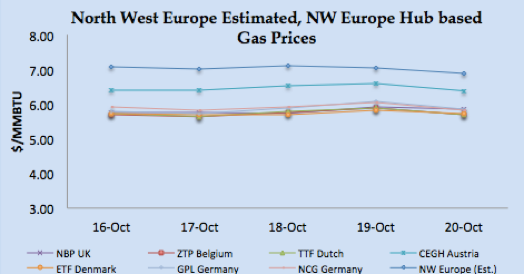

- North Western European hub curve prices were weak through the week due to supply balance, along with the correction in South West Europe prices.

- Keeping in view Asian spot prices bearish tone North West Europe prices are driven on the basis of NBP UK premium and estimated at $6.88/MMBTU, 45 cents premium on NBP UK November price.

- Based upon Iberian Peninsula gas hub price and freight cost from Spain to the Asian market, South Western Europe prices are estimated in the range of $7.20-$7.40/MMBTU.

- US Gulf Coast producer price on FOB basis for December delivery for Asian destination comes around $7.45/MMBTU level as currently Asian prices are dictating global LNG prices, for European destinations the netback comes around $6.33/MMBTU.

|

|

|

|

|

|

Author’s Comments

- LNG prices right now seem bearish as the buyers are on the sidelines for Spot transaction and covering their requirement through contractual procurement. Crude price impact on LNG prices as of today is minimal as last three month average Brent price is around $52.17/BBL and LNG Brent linked price comes around $7.61/MMBTU on 14.5% slope and $7.82/MMBTU on 15% slope. We expect prices to remain bearish unless the weather gets colder in North East Asia and China comes back in the market.

LNG Merchant Activity

LNG merchant data is developed in collaboration with Clipper Data LLC.

|

|

|

|

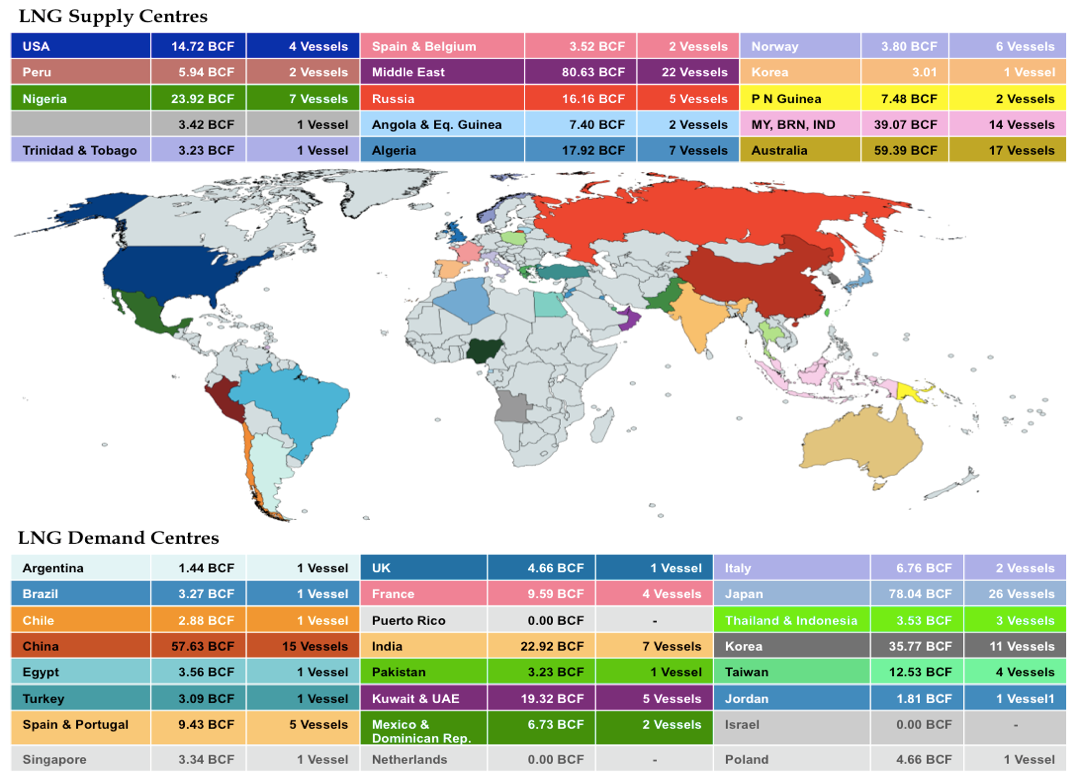

LNG SUPPLY CENTRES

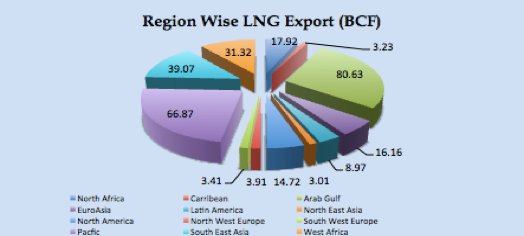

- 93 vessels carrying 6.02 million tons (289.24 BCF) loaded from various supply centres, during the week from 14th -20th October 2017.

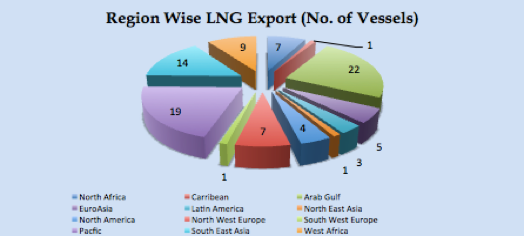

- 19 Vessels left from Qatar carrying 70.99 BCF for India, Korea, Japan, China, UK & Latin America.

- Seven vessels carrying 23.92 BCF departed from Nigerian port, for France, Spain, Mexico, India and Egypt.

- Algeria loaded seven vessels carrying 17.92 BCF for Turkey, France, Spain, Greece and UK.

- Pont Fortin, Trinidad & Tobago loaded one vessel with 3.23 BCF for Pacific Basin.

- 14 vessels loaded from Brunei, Malaysia and Indonesia with loads of 39.07 BCF for China, Japan, Korea, Thailand and Taiwan.

- Seventeen vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, Taiwan, China and Korea carrying 59.39 BCF.

- One cargo left for Lithuania with 3.15 BCF from Norway, besides four small vessels within region exports.

- One reload from South Korea, POSCO Gwangyang LNG Terminal carrying 3.01 BCF.

- Two reloads one each from Zeebrugge & Enagas Cartagena for Korea and Dahej, India carrying 3.52 BCF.

- Five vessels left from Russia for Japan, Korea & Taiwan carrying 16.16 BCF.

- 14.72 BCF loaded into 4 vessels from Cheniere Sabine Pass for Asian destinations along with South American and European destinations.

LNG DEMAND CENTRES

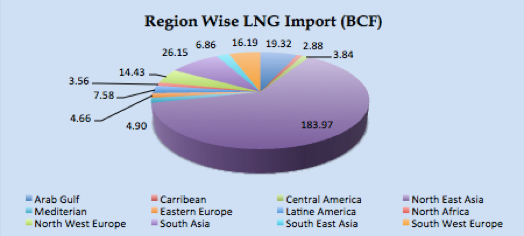

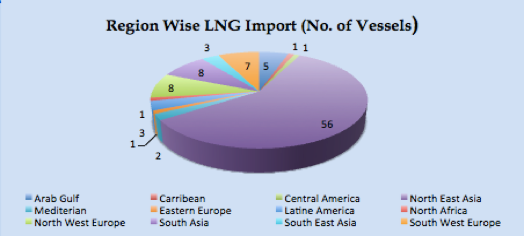

- 96 vessels carrying 6.18 million tons (294.36 BCF) discharged at various ports the week from 14th-20th October 2017.

- Japan being the biggest importer with 78.04 BCF and 26 vessels discharged, 17.28 BCF more than last week, North East Asia block comprising of Japan, Korea, China and Taiwan discharged 183.97 BCF (56 vessels) approximately 61.89% of total discharged global volume. Increased by 46 BCF from last week.

- Argentina receives 1.44 BCF (1 vessel) from Point Fortin, Trinidad & Tobago.

- Mexico received 3.84 BCF (1 vessel) from Nigeria.

- India receives 7 vessels with 22.92 BCF, 5 at Petronet, on3 each at Hazira and Ratingiri from Equatorial Guinea, Nigeria, Qatar and Australia.

- Pakistan received one vessel carrying 3.23 BCF from Qatar.

- France receives 4 vessels with 9.59 BCF, three vessels from Algeria and one vessel from Nigeria.

- Spain received 5 cargoes with 9.43 BCF, three from Peru, one each from Norway & Nigeria.

- Italy received 2 vessels carrying 6.76 BCF from Qatar.

- One vessel discharged 4.66 BCF at Isle of Grain LNG terminal, UK from Qatar.

- Two vessels arrived at China and Brazil carrying 6.51 BCF from Sabine Pass this week.

- One vessel carrying 3.31 BCF arrived Aqaba, Jordan from Oman, and one vessel arrived Hadera Deepwater LNG terminal Israel carrying 2.88 BCF from Trinidad & Tobago.