Market Analysis

Crude Oil

- Crude oil prices ended the bullish rally since mid August 2017 on over supply situation along with profit taking during the week, however Thursday spike was due to Saudi Arabia and Russia comment on extending production cut along with incoming Tropical Storm Nate.

- Since Monday, investor took a profit taking stance as producers increased hedging, since late August 2017 115 million barrels have been hedged, which also depicted market lack of confidence on bullish rally.

- During Saudi King visit to Moscow, Saudis comments on being flexible on Moscow’s suggestion on extending the production cut until end of 2018 has brought some bullish temp in the market with Brent went up to $57.00/BBL, whereas WTI jumped to $50.79/BBL.

- Tropical storm Nate has shut down 70% of off-shore oil and gas production in US, however the impact is subdued as market has already incorporated the hurricane season impact.

- Wednesday, EIA report US crude export oil by 2 million barrel per day has raised the concern of oversupply and price declined.

- Brent prices closed on $55.62/BBL on Friday, decreased by 3.3% from last Friday price of $57.54/BBL, while WTI retreated to $49.29, decrease by 5.6% from last week price of $52.22/BBL.

- Brent/WTI spread this Friday was $6.33/BBL in comparison with last week spread of $5.87/BBL, depicting increasing interest in WTI by refiners.

- Brent future closed at 55.33/BBL, $55.31/BBL & $55.20/BBL for December, January & February 2018 respectively, a decrease from last week closure of $56.73/BBL, $56.48/BBL & $56.36/BBL for December, January & February 2018 respectively, depicting fundamental back to oversupply situation.

- For WTI curve market, Friday closure were $49.29/BBL for November, $49.60/BBL for December and $49.84/BBL for January 2018, depicting downward price direction..

- US crude export rose to record high of 1.98 million barrels/day during September 23-29, as reported by EIA.

- EIA Weekly report reported a draw of 6.0 million barrels with stock at 465.0 million barrel on 29th September 2017; against a market expectation of 0.756 million barrels build up.

- Gasoline inventories at 218.9 million barrel reported on 29th September 2017, recording 1.6 million barrels build-up against a market expectation of 1.1 million barrels buildup on week on week basis.

- US refineries operated at 88.1% of their operable capacity and input to crude oil refinery decreased by 0.145 million barrels a day from last week, exhibiting normalization of refinery operations.

- Baker Hughes rig count reported a decrease by 2 in oil rigs, with total standing at 748.

- Crude oil back to bearish run due to oversupply situation, long-term outlook is bearish, as OPEC production cut has to be implemented along with US production to support the oil-balancing attempt.

NATURAL GAS

- Natural gas futures finished lower last week amid forecasts for rising production and mild weather over the next two weeks, with lower demand for heating and cooling across US.

- Henry Hub prices kept on moving south through out the week and closed at $2.86/MMBTU on Friday.

- Market didn’t believe any disruption in production due to tropical storm Nate, so overall bearish tone prevailing around Henry Hub.

- Average total supply of gas remained around same level as last week of 79.7 BCFD, with overall demand decreased by 14% from power generation sector in comparison from last week. Natural gas exports to Mexico increased 1%.

- Baker Hughes reported a decrease in natural gas rigs by 1 and total number stands at 188.

- Working gas in storage was 3,508 BCF as of Thursday, September 29th 2017, an increase of 42 BCF from previous week, against an expectation of 51 BCF. Stocks were 161 BCF less than last year at this time and 8 BCF below the five-year average.

- November Natural Gas futures settled at $2.865/MMBTU, whereas for December $3.045/MMBTU and $3.169/MMBTU for January 2018 were settled on Friday, decreased from last Friday.

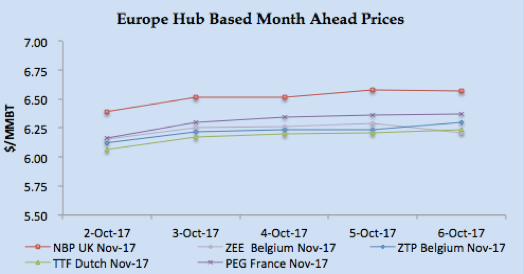

- European hub prices are getting support from rising coal prices along with weather driven demand.

- Gas prices in UK remained bullish due colder weather during the week along with Norwegian planned outage and unplanned outage affecting Heimdal and Segal. Overall market direction is now governed by winter season.

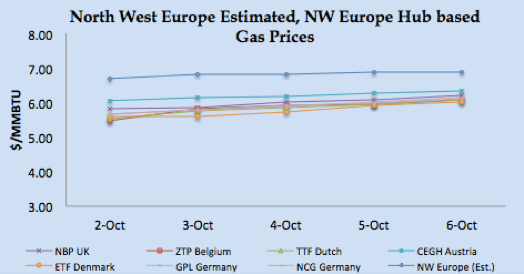

- NBP UK curve market jumped to 50.280 Pence/Therm & 52.470 Pence/Therm for November & December respectively on Friday, a more than 5.50% increase from last Friday price.

- Weather is expected to be cold in Netherland, Germany and Belgium and demand is expected to be strong. Continental supply from Russia is normal however from Norway, there is a planned outage from 10th – 12th October 2017.

- France is expected to be cold and French Nuclear plant issue still pushing the price upward.

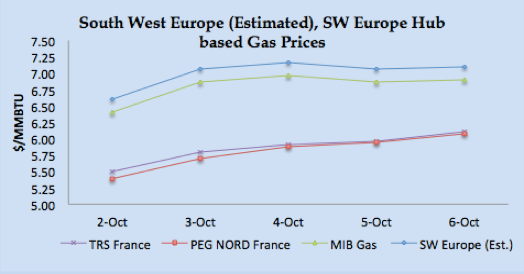

- In the Day Ahead market TTF closed at €17.63/MWH (equivalent of $6.06/MMBTU), PEG Nord France closed at €17.67/MWH ($6.08/MMBTU) on Friday, depicted bullish run through out the week.

- Spain and Portugal are expected to be warm and requirement for natural gas is high due to air-conditioning requirement.

- In the curve market the prices, TTF November jumped to €18.13/MWH ($6.23/MMBTU) and December at €18.35/MWH ($6.31/MMBTU) on Friday

- November & December PEG Nord forward prices closed at €18.53/MWH ($6.37/MMBTU) & €18.95/MWH ($6.52/MMBTU).

- Iberian Peninsula prices settled at €20.05/MWH ($6.89/MMBTU) on Friday, jumped by 7.80% since start of the week.

- MIBGAS e forward market there were transactions closed on 2nd October at €21.05/MWH ($7.23/MMBTU) level.

- European price outlook is bullish, however bullish run in Asian LNG price is dictating the prices currently, US and all other supply centres are getting better netback selling to Asian market of China and India.

Currency

- Dollar remain strong through out the week due to positive data coming out from economic and labor from along with rate hike and tax overhaul news.

- Index of national factory activity surged to a reading of 60.8 last month, the highest reading since May 2004, from 58.8 in August.

- The greenback found support after the U.S. Department of Labor said initial jobless claims fell more than expected to 260,000 last week.

- Rising exports and falling imports cut the U.S. trade deficit to $42.4 billion in August, the lowest in 11 months.

- Philadelphia Federal Reserve Bank President Patrick Harker said on Thursday that he is still planning on one more rate hike this year and three next year.

- Greenback got support after the U.S. House of Representatives approved a 2018 spending bill, an important step to advance an eventual tax reform plan.

- The S. dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies closed at 93.80 on Friday.

- Euro remained volatile during the week more towards weaker ground due to political uncertainty around Catalonia referendum and poor PMI from Europe, with Italy and France performing worse and Germany falling short on composite PMI. Towards the end of the week Euro got support from German factory order better performance of 3.8% increase on M-o-M basis. EUR/USD closed at 1.17323 on Friday.

- GBP/USD remained volatile as positive PMI data on composite and service exceeded expectation and printed 53.6 and 54.1, however Prim Minister May speech at Conservative Party conference has negative impact on GBP, GBP/USD closed at 1.30651 on Friday.

- Japanese Yen remained range bound and closed at Yen 112.707 (0.00887 JPY/USD) on Friday.

- AUD/USD closed at 0.78393 on Friday, bearish trend through the week due to USD bull run along with weak external and domestic market scenario, like China credit rating down grade along with RBA Governor comments that Central bank is not considering any monetary tightening.

- AUD/USD continues to weaken after RBA board member Harper unexpectedly talks of possible rate cuts from the central bank. AUD/USD closed at 0.77647 on Friday.

- Chinese Yuan remained range bound and closed at 6.64813 as China Central bank had reduced control measures on FX.

Weather

- UK, Germany, Belgium & Netherland entered in cold season with temperature around 13-17oC and expected to remain same as per seasonal level of around 13-18oC next week.

- France was around 14-19oC and expected to remain cold next week around 16-18o

- Weather remained warm in Spain & Portugal around 27-33oC and expected to ease a bit at 24-31oC next week.

- Temperature in Argentina was around 19-24oC, with some rain, next week outlook is around 18-22o

- Brazil remained hot with temperature around 27-32oC, next week is expected to remain same around 30-33o

- Mexico this week with clouds and bit of rain was around 2024oC and expected to remain same next week.

- Middle East region summer season still prevailing, with Egypt around 29-33oC and expected to ease a bit next week around 28o Kuwait most of the week at 39-43oC before easing up to seasonal level of 36oC and expected to remain at 36oC next week. Dubai also eased to 35oC during the later half of the week from 39-41oC, expect to remain 35oC majority of next week before warming back to 38oC level.

- Pakistan weather remained around 35oC along with India and expected to remain the same next week. November onward demand increased in part of Indian Subcontinent due to cold weather.

- Temperature still hot in North East Asia, with temperature around 35-37oC in Taiwan before cooling it to 30oC due to rain and expect to be around 35oC next week, 20-24oC in Korea and expected to remain same next week, China 20-24oC this week and cooler next week around 16-19oC, and Japan is around 20-24oC with next week around 24-27o.

- South East Asia still warm with temperature in Thailand, Indonesia and Jakarta around 30-32oC, and expected to remain same next week.

- USA Weather: US weather remained warm with few days of rain easing up the weather, next week weather is expected to be warm except Pacific Northwest, which is getting cold.

LNG

- Overall LNG prices remained bullish with Asian price dictating the overall price for pre-winter season.

- Asian prices through out week remained bullish due to strong demand from Indian and China and traditional price upward movement before winter season.

- Indian state owned companies floating tender for November and December delivery, and this demand is being generated from power sector as post monsoon coal supply is being hampered.

- China demand is growing due to its gasification program where the objective is to move millions of household from coal to gas heating, last eight months Chinese imports are at 22.1 million tons, highest ever.

- Coal prices also supporting LNG prices, Indonesian Coal prices closed at $93.99, increased by 2.13% from $92.03/MT last week.

- Oil indexed contract pricing based upon 14.5% slop (3-0-1) are coming around $7.55/MMBTU level, which is keeping buyer from Japan, Taiwan and Korea to focus on maximizing the contractual buying.

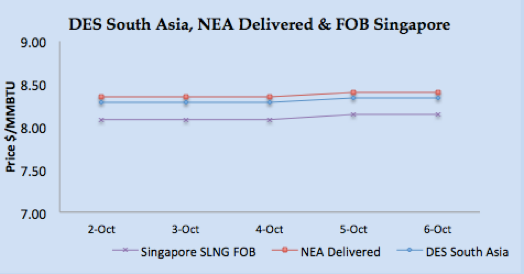

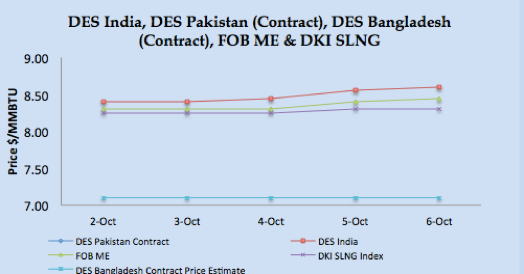

- Asian price closures on Friday were; JKM at $8.600/MMBTU, SLNG NEA Delivered at $8.395/MMBTU and FOB Singapore at $8.140/MMBTU.

- Based upon FOB Singapore and Middle East, DES India is calculated around $8.340/MMBTU level. DKI SLNG Index on Friday reported at $8.300/MMBTU.

- JKM Future curve market jumped to $8.230/MMBTU, $9.150/MMBTU & $9.350/MMBTU for November, December 2017 & January 2018 delivery respectively, depicting historical pre-winter price trend.

- European hub curve prices remained bullish through out the week on cold temperature in North West Europe along with warm weather in Iberian Peninsula and rising coal prices.

- Keeping in view Asian spot prices along with few forward transactions in Iberian Peninsula hub, North West Europe prices are driven on the basis of NBP premium and estimated at $6.90/MMBTU, 30 cents premium on NBP UK November price.

- Based upon Iberian Peninsula gas hub price and freight cost from Algeria for Spanish market and Asian market netback, South Western Europe prices are estimated in the range of $7.05/MMBTU.

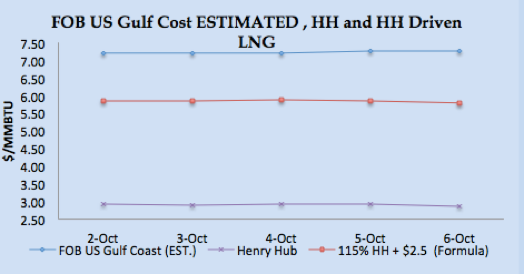

- US Gulf Coast producer price on FOB basis for November delivery for Asian destination comes around $7.25/MMBTU level as currently Asian prices are dictating global LNG prices.

- On the supply side, more production is expected to emerge from Papua New Guinea and Russia’s Sakhalin II plant, and output in Australia is also expected to rise as the last batch of its mega-projects gradually starts up production.

- BW Integrity to be moored at Port Qasim, Pakistan, for the second terminal, has arrived.

- Gazprom and Saudi Aramco has signed an MoU to examine possibilities for cooperation in exploration, production, transportation and storage of gas, as well as LNG projects.

|

|

|

|

|

|

Author’s Comments

- LNG market has entered in pre-winter buying mood, which is further supported by strong demand from China and India. Typically this is a bullish run till January, however important dimensions to be considered here are winter severity in North East Asia along with supply situation. European LNG demand will also be bullish especially in UK due to lack of gas storage this year.

- Overall supply situation seems to bring bearish tone with commissioning of Australia Wheatstone along with Chienere fourth line production. Overall market is expect to remain bullish in the short run.

LNG Merchant Activity

LNG merchant data is developed in collaboration with Clipper Data LLC.

|

|

|

|

LNG SUPPLY CENTRES

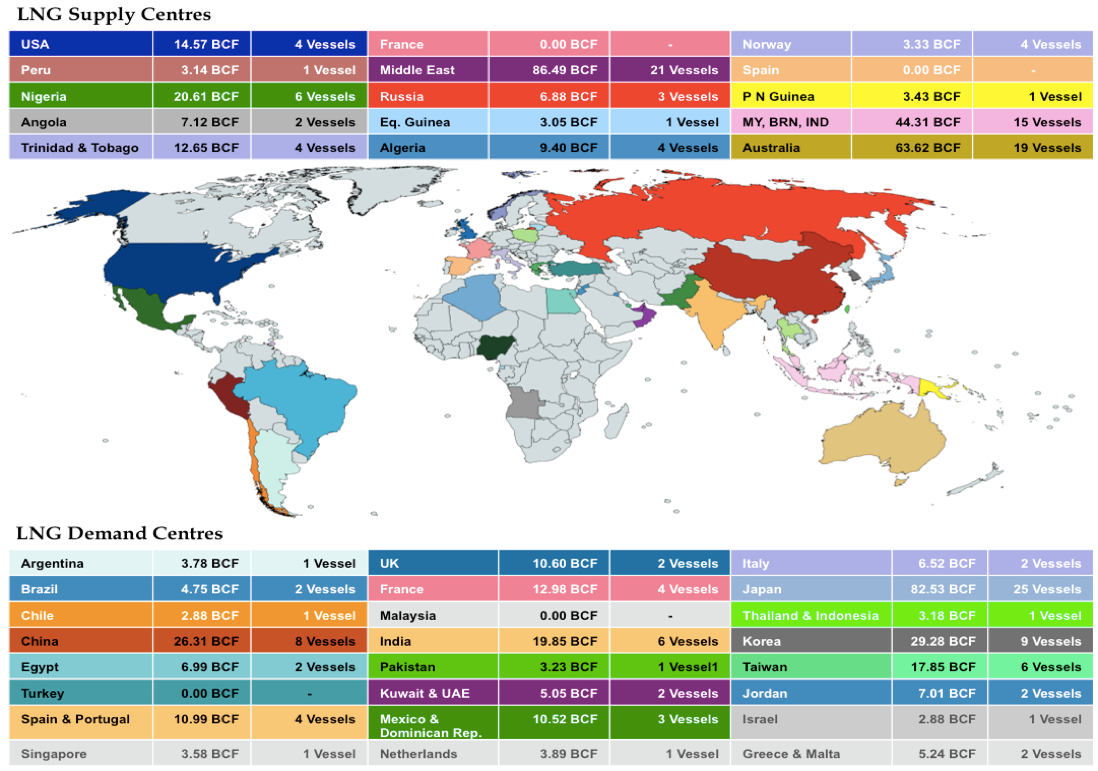

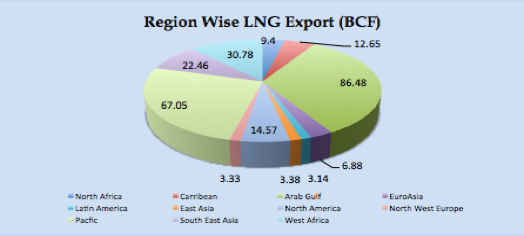

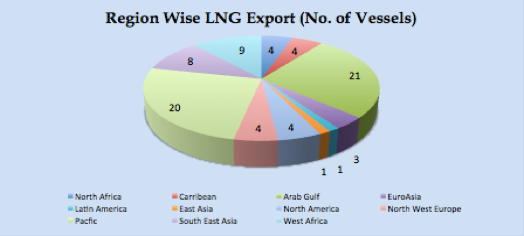

- 86 vessels carrying 5.87 million tons (281.95 BCF) loaded from various supply centres, during the week from 30th September – 6th October 2017.

- 19 Vessels left from Qatar carrying 80.37 BCF for India, Korea, Japan, Latin America and Europe, 6.86 BCF lower that last week.

- Six vessels carrying 20.61 BCF departed from Nigerian port, for Japan, Taiwan, Italy and Egypt.

- Algeria loaded four vessels carrying 9.40 BCF for France, Spain and Latin America.

- Pont Fortin, Trinidad & Tobago loaded four vessels with 12.65 BCF for European and South American ports.

- 15 vessels loaded from Brunei, Malaysia and Indonesia with load of 44.31 BCF for China, Japan, Korea and Taiwan.

- Nineteen vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, Singapore, Taiwan, China and Korea carrying 63.22 BCF, an increase of 19.05 BCF from Australian ports.

- One cargo left for Netherland with 3.15 BCF from Norway, beside three small vessels within region exports.

- One reload from South Korea, POSCO Gwangyang LNG Terminal for Japan, carrying 3.38 BCF.

- Three vessels left from Russia for Japan carrying 6.88 BCF.

- 14.57 BCF loaded into 4 vessels from Cheniere Sabine Pass for Asian destinations.

LNG DEMAND CENTRES

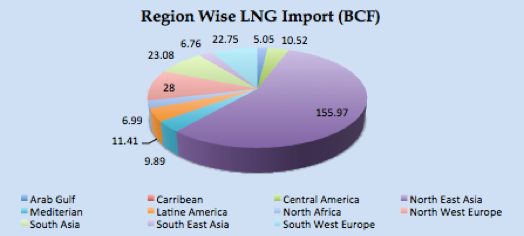

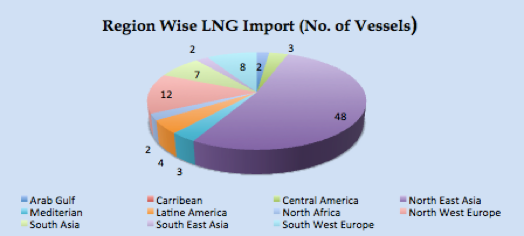

- 91 vessels carrying 5.83 million tons (280.42 BCF) discharged at various ports the week from 30th September – 6th October 2017.

- Japan being the biggest importer with 82.53 BCF and 25 vessels discharged, North East Asia block comprising of Japan, Korea, China and Taiwan discharged 155.97 BCF (48 vessels) approximately 55.62% of total discharged global volume.

- Argentina receives 3.78 BCF (1 vessels) from Qatar, while Brazil received 4.75 BCF (two vessels) one from each Sabine Pass and Bonny ports.

- Mexico received 10.52 BCF (3 Vessels) two from Sabine Pass and one from Indonesia.

- India receives 6 vessels with 19.85 BCF, 4 at Petronet, One at Hazira and Dabhol each , three vessels from Qatar, one from each Nigeria, Trinidad & Tobago and Angola.

- Pakistan received one vessel carrying 3.23 BCF from Qatar.

- France receives 4 vessels with 12.86 BCF from Qatar, Nigeria and Algeria.

- Spain received four cargoes with 10.98 BCF from Nigeria, Algeria, Norway and Qatar.

- Italy received 2 vessels carrying 6.52 BCF from Qatar.

- Two vessels carrying 7.01 BCF arrived Aqaba, Jordan from Equatorial Guinea and Algeria, and one vessel arrived Hadera Deepwater LNG terminal Israel carrying 2.88 BCF from Trinidad & Tobago.

- UK received two Q-Max vessels, 10.60 BCF from Qatar.