Market Analysis

Crude Oil

- Crude oil prices rallied strong through out the week on the premises of Iraqi Kurdistan along with discussion on stronger demand for oil.

- Kurdistan referendum yielded almost 93% vote in favor of secession from Iraq which has created tension within the region and there is uncertainty as 500,000-600,000 barrels/day flows from Kirkuk field and Northern Iraq.

- Lot has been discussed in last week petroleum summit where participants took a bullish point on crude prices and new price level of $60/BBL was echoed during that summit.

- Brent prices closed on $57.54/BBL on Friday, retreated a bit after crossing $59/BBL mark on Monday. WTI also closed a bit lower on Friday after reaching $52.22/BBL on Monday.

- Brent/WTI spread this Friday was $5.87/BBL in comparison with last week spread of $6.20/BBL. Start of the week the spread was $6.80/BBL.

- Brent future closed at $56.73/BBL, $56.48/BBL & $56.36/BBL for December, January & February 2018 respectively, depicting non-confidence on $60/BBL level.

- For WTI curve market, Friday closure were $51.64 /BBL for November, $51.90/BBL for December and $52.08/BBL for January 2018, depicting a contango.

- US crude export rose to 1.5 million barrels/day during September 15-22, as reported by EIA, justifying the increase spread between Brent and WTI.

- EIA Weekly report reported a draw of 1.8 million barrels with stock at 471.0 million barrel on 22nd September 2017; against a market expectation of 3.4 million barrels build up.

- Gasoline inventories at 217.3 million barrel reported on 22nd September 2017, recoding 1.1 million build-up against a market expectation of 0.91 million draw on week on week basis.

- US refineries operated at 88.6% of their operable capacity and input to crude oil refinery increased by 1.0 million barrels a day from last week, exhibiting normalization of refinery operations.

- Baker Hughes rig count reported an increased by 6 in oilrigs, after three weeks of decline, with total standing at 760.

- Crude oil bullish run seems like short-run as on the basis of fundamentals there is not much support in term of demand growth and Kurdistan supply hurdle of 500K seems too small keeping in view the over supply situation.

Natural Gas

- Henry Hub remained bullish most of week before the correction on Friday as weather outlook is a bit cool which will ease off the warm weather conditions.

- Henry Hub prices went up to $3.07/MMBTU from Monday starting price of $2.92/MMBTU and closed at $3.01/MMBTU on Friday.

- The rationale for $3.07/MMBTU level during the week was positive economic data upbeat along with warmer weather forecast which eventually got corrected and brought it the bearish tone.

- Average total supply of gas remained same as last week of 80.1 BCFD, with demand increased by 6% from last week due to contrasting temperature during the week, reported by EIA.

- Baker Hughes reported a decrease in natural gas rigs by 1 and total number stands at 189.

- Working gas in storage was 3,466 BCF as of Thursday, September 28th 2017, an increase of 58 BCF from previous week, against an expectation of 66 BCF. Stocks were 127 BCF less than last year at this time and 41 BCF above the five-year average.

- November Natural Gas futures settled at $3.018/MMBTU, whereas for December $3.192/MMBTU and $3.306/MMBTU for January 2018 were settled on Friday.

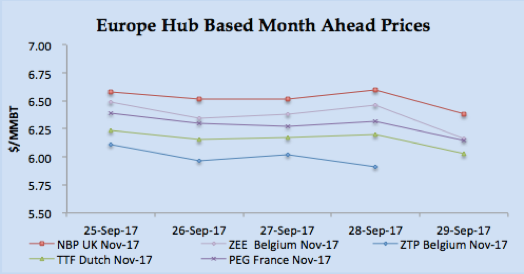

- Gas prices in UK remained bullish due to rising oil prices, maintenance at Doornum terminal, which curtailed Norwegian gas supply, however in term of demand weather seems mild in the coming week.

- NBP UK DA prices closed 46.4939 Pence/Therm (equivalent $$6.23/MMBTU) on Friday, increased by 2.20% from last Friday of 45.4930 Pence/Therm.

- NBP UK curve market for November & December closed at 47.6660 Pence/Therm & 49.6300 Pence/Therm (equivalent of $6.38/MMBTU & $6.65/MMBTU) downward trend based upon falling coal prices.

- Weather is expected to be mild in Netherland; demand is expected to be low along with improved pipeline gas outlook in the continental system from Norway and Russia.

- France is expected to be mild in term of weather, however EDF has been ordered by French Nuclear Authority (ASN) to temporarily shut down its nuclear plant for a month, this has been a bullish factor which kept the prices stable.

- TTF closed at €17.68/MWH (equivalent of $6.12/MMBTU), PEG Nord France closed at €17.75/MWH ($6.15/MMBTU) on Friday.

- Spain and Portugal are expected to be warm and requirement for natural gas is high due to air-conditioning requirement.

- Iberian Peninsula prices settled at €19.05/MWH ($6.60/MMBTU) on Friday.

- In the curve market the prices, TTF November closed at €17.41/MWH ($6.03/MMBTU) and December at €17.69/MWH ($6.12/MMBTU).

- November & December PEG Nord forward prices closed at €17.75/MWH ($6.15/MMBTU) & €18.16/MWH ($6.29/MMBTU), bearish trend based upon mild weather, falling coal prices and improved gas pipeline supply.

- European price outlook is bearish keeping in view SPOT prices in Asian market, Based upon current Asian prices all the producers are getting better netback on Asian destination. Current Asian prices seem very attractive for reload of cargoes from European terminals.

Currency

- Dollar remained bullish for the first three days on Fed President hawkish comment along with positive economic news on durable goods along with Euro weak performance due to German election.

- However USD fell from Thursday due to weak economic data on labor and inflation.

- Fed Chairwoman Janet Yellen remarks on Tuesday where she re-iterated interest rate hike gradually.

- On the economic front US made capital goods orders increased by 0.9% in August along with shipment by 0.7%, maintaining upward trend from July.

- Euro preformed poor due to recent German election, where German Chancellor will have to build a coalition to form a government.

- USD DXY closed at 93.44 on Wednesday based upon above facts, however USD fell from Thursday as US department of Labor reported weaker data with job less claims increased to 12,000 on week on week basis against market expectation of 10,000.

- The S. dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies closed at 93.08 on Friday.

- Euro remained weak through the week due to German election, however the pair got some strength in the later part of the week due to USD weak performance, next week will be interesting to watch as Fed is going to give a clear picture on interest rate hike for December plus release of economic data. EUR/USD closed at 1.18138 on Friday.

- GBP/USD remained weak in the beginning due to bullish USD however, later part of the week GBP bearish run was due to second quarter economic slow down as growth rate decelerated to 1.5% in Q2 on annualized basis. GBB/USD closed at 1.33993 on Friday.

- Japanese Yen remained weak through out the week as Japanese government announced early elections. USD/JPY closed at Yen112.651 (0.00888 JPY/USD) on Friday.

- AUD/USD closed at 0.78393 on Friday, bearish trend through the week due to USD bull run along with weak external and domestic market scenario, like China credit rating down grade along with RBA Governor comments that Central bank is not considering any monetary tightening.

- Chinese Yuan declined to 6.66676 before getting strength to close at 6.64984 as China Central bank is holding sort position on foreign currencies against Yuan.

Weather

- UK, Germany, Belgium & Netherland weather remained mild around 16-20oC and expected to remain the same next week around 14-20oC with rain in Netherlands and Germany.

- France was around 19-22oC and expected to be a cooler in the beginning around 15-18oC before getting warm around 22o

- Weather remained warm in Spain & Portugal around 27-31oC and expected to remain warm next week.

- Temperature in Argentina was very volatile ranging between 16-21oC, as it was sunny in the beginning of the week and closed at 16o Next week outlook is warmed around 19-23oC.

- Brazil remained hot with temperature around 28-30oC, with two days around 22-24oC due to cloud and rain. Next week is expected to remain same with one day around 24oC due to rain.

- Mexico this week was around 19-24oC and expected to remain same next week.

- Middle East region summer season still prevailing, with Egypt around 31oC and expected to be bit warmer next week before easing to 26oC by end of the week. Kuwait 39-44oC and Dubai around 39-41oC, next week weather easing a bit with Kuwait and Dubai around 38o

- Pakistan weather remained around 25-32oC whereas in India temperature was around 27-34oC with some cloud cover. Next week weather is expected to remain around 31oC with sunny condition and India around 28-30o

- Temperature still hot in North East Asia, with temperature around 35-38oC in Taiwan before cooling it to 32oC, 26-30oC in Korea and 23oC by end of the week, China 27-30oC in the beginning of the week and went down to 22oC from Tuesday till Thursday, and Japan is around 24-28o Weather expected to be cooler in the coming week with Taiwan 31-36oC, Korea around 21-26oC, China 20-27oC & Japan 20-26oC.

- South East Asia already in hot weather, Thailand around 30-35oC, Indonesia and Malaysia around 33-35oC, and will remain same next week.

- USA Weather: US weather was mix with South West, South East, North East and Mid West remained warm whereas Pacific remained cold and overall next week is expected to be cold in US till Thursday.

- Overall weather remained is warm this week with outlook of colder weather in coming week.

LNG

- LNG prices remained bullish primarily due to northbound crude price, recent tender closure for November delivery, strong Chinese demand along with buying interest from India.

- Crude prices remained bullish along with coal prices, which added into overall bullish trend for LNG. Brent price went up to $59.02/BBL before easing up at $57.54/BBL.

- Coal price also bullish with Indonesian Coal pries closed at $92.03/MT, increased by 9.60% on month on month basis.

- Recent tender closure from PNG for November delivery was heard at $8.40/MMBTU level.

- Chinese LNG appetite is growing by 44% for January –August period in comparison with last yearly Experts are of the opinion that China may overtake South Korea in LNG procurement in order to improve air-quality numbers.

- Chinese buyer lack of long term contract will always have bullish impact on LNG prices, CNOC recently concluded to buy 4 cargoes for November delivery at around $8.40/MMBTU.

- Indian buyers are also in the market as Gail India has launched a tender to buy three cargoes, one in November and two in December 2017. Oil ministry in India has announced 17% increase in natural gas prices effective from October 1 for 6 months.

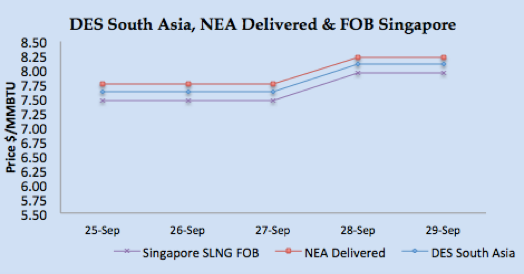

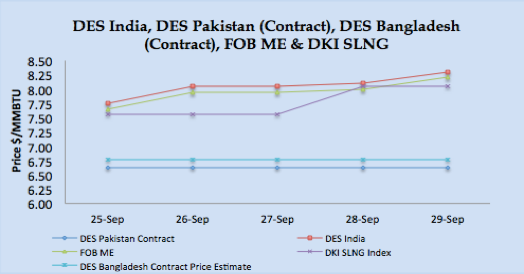

- Asian price closures on Friday were; JKM at $8.4000/MMBTU, SLNG NEA Delivered at $8.2230/MMBTU and FOB Singapore at $7.9470/MMBTU.

- Based upon FOB Singapore and Middle East, DES India is calculated around $8.1500/MMBTU level. DKI SLNG Index on Friday reported at $8.0400/MMBTU.

- JKM Future curve market closed at $8.1650/MMBTU, $8.8750/MMBTU & $9.150/MMBTU for November, December 2017 & January 2018 delivery respectively, depicting strength in price for winter.

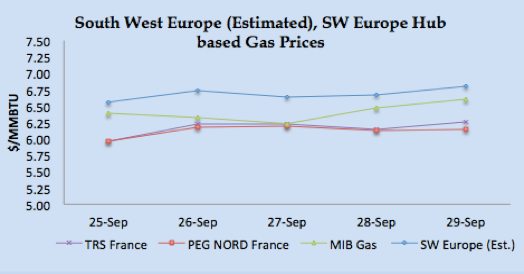

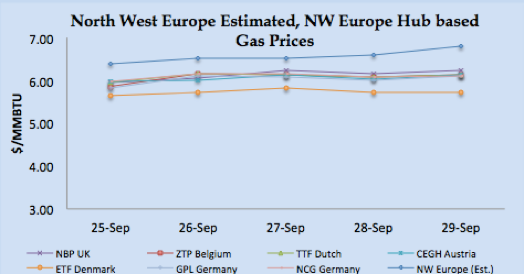

- European hub curve prices remained bullish through the week on rising crude prices along with French Nuclear plant stoppage.

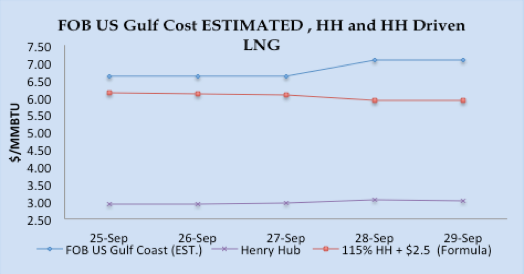

- Keeping in view Asian prices, North West Europe prices were estimated to be around $6.80/MMBTU, 20 cents premium on NBP UK November price equivalent of $6.60/MMBTU level.

- Based upon netback from Algeria for Asian market, South Western Europe prices are estimated to be in the range of $6.95/MMBTU.

- US Gulf Coast producer price on FOB basis for November delivery for Asian destination comes around $7.05/MMBTU level as currently Asian prices are dictating global LNG prices.

|

|

|

|

|

|

Author’s Comments

- Crude based LNG prices at 13.5% or 14% on last three months average is much lower than current Spot prices, as buyers Japan, Korea and Taiwan are buying on long term contract basis whereas Chinese buyers are buying on Spot for winter season.

- Lack of fundaments in the crude market will have bearish impact on crude price and with public holiday in Taiwan and China in the coming week, I believe LNG price bullish will be short lived.

- Weather is getting cold in North West Europe, whereas South West Europe still warm. North East Asia is also getting cold whereas South East Asia still warm. US weather is expected to remain cold this week. Weather based bullish tone is adding into Asian and European market prices.

LNG Merchant Activity

LNG merchant data is developed in collaboration with Clipper Data LLC.

|

|

|

|

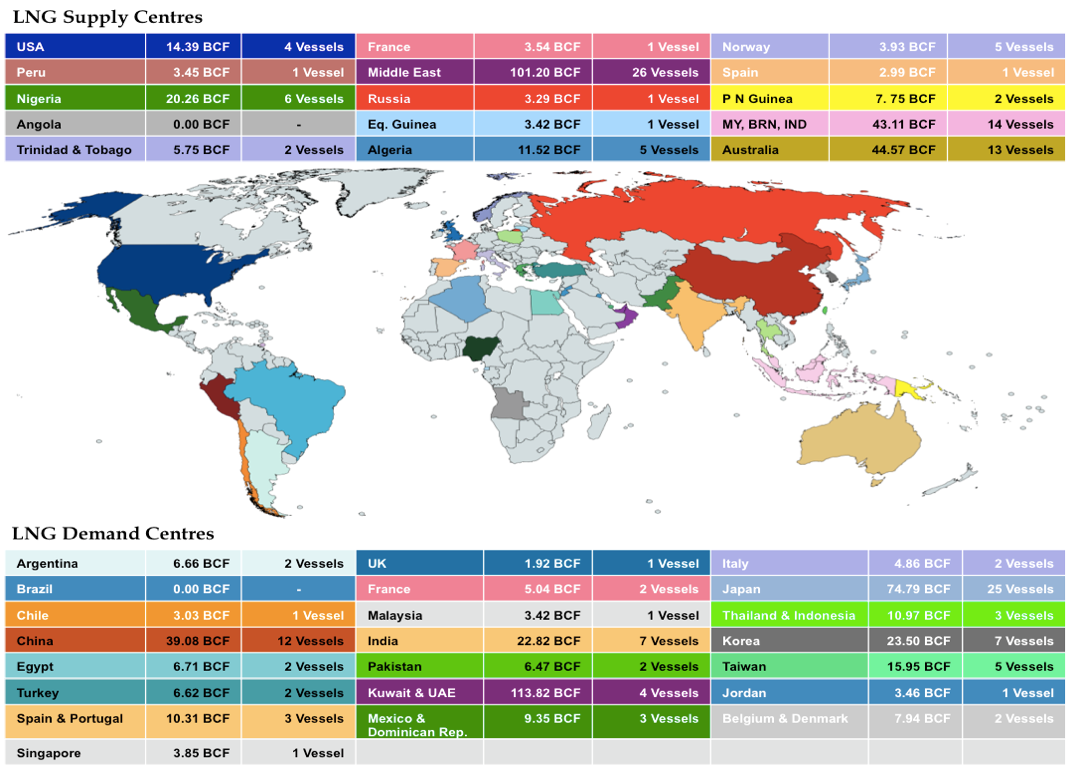

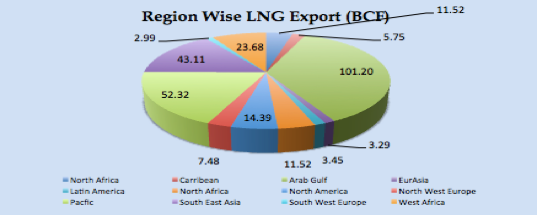

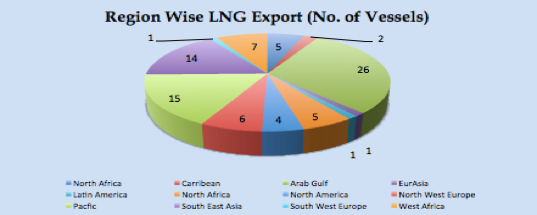

- 82 vessels carrying 5.65 million tons (269.20 BCF) loaded from various supply centres, during the week from 23rd -28th September 2017.

- 23 Vessels left from Qatar carrying 87.23 BCF for India, Korea, Japan, Latin America and Europe.

- Six vessels carrying 20.26 BCF departed from Nigerian port, for Europe and Asian destinations.

- Algeria loaded five vessels carrying 11.52 BCF for Italy, Spain, Turkey and Greece.

- Pont Fortin, Trinidad & Tobago loaded two vessels with 5.75 BCF for South American ports.

- One vessel loaded from Brunei with load of 3.25 BCF for China.

- Thirteen vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, Singapore, Taiwan, China and Korea carrying 44.57 BCF.

- One cargo left for China with 3.31 BCF from Norway.

- Two reloads from Montoir, France & Cartagena, carrying 6.54 BCF.

- One vessel left from Russia for Japan carrying 3.29 BCF.

- Middle Eastern terminal at Das (UAE) and Qalhat (Oman) loaded 3 vessels carrying 9.43 BCF for Japan.

LNG DEMAND CENTRES

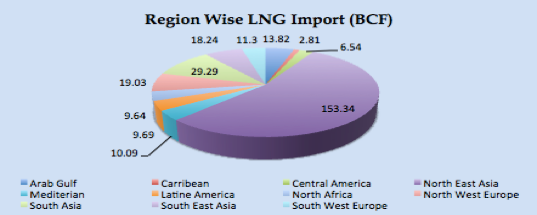

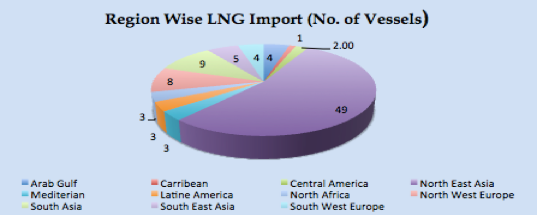

- 91 vessels carrying 5.90 million tons (283.79 BCF) discharged at various ports the week from 23rd-29th September 2017.

- Japan being the biggest importer with 74.79 BCF and 25 vessels discharged, North East Asia block comprising of Japan, Korea, China and Taiwan discharged 154.34 BCF (49 vessels) approximately 54.38% of total discharged global volume.

- Argentina receives 6.66 BCF (2 vessels) from Qatar and Nigeria., while Egypt received 6.71 BCF (2 vessels) from Qatar.

- India receives 7 vessels with 22.82 BCF, three vessels from Qatar, two from Nigeria and one from Algeria.

- Pakistan received two vessels carrying 6.47 BCF from Qatar.

- France receives two vessels with 5.04 BCF from Qatar and Algeria.

- Italy received two cargoes with 4.86 BCF from Algeria and Qatar.

- Spain receives 2 vessels carrying 6.45 BCF USA and Peru.

- Turkey received two vessels one from Cheniere and other from Etki LNG Terminal, Algeria.

- Isle of Grain, UK received one vessel, 1.92 BCF from Algeria