A case study

There are some common questions that repeatedly get posed in my treasury products class about the variations available within exotic derivative instruments. Are these exotic contracts really needed? Who really benefits from selling these exotic products? Is their effectiveness real or over rated? Do zero cost structures add value or destroy value for customers and clients? Has anyone ever done a comparison of hedge effectiveness of vanilla products, TARF and participating forwards?

The primary questions come from relationship managers who have some history with a treasury transaction gone sour. When a product, transaction or structure blows up they are the ones who have to deal with the fall out. Given their history with customer blow outs and damaged relationships their level of comfort with exotic products is understandably low.

On the other side treasury can only sell products and transactions where immediate structuring is possible. They can only sell stuff for which there is ready inventory and active markets. Most treasuries rely on selling off the shelf products through institutional relationships rather than structure a transaction from the ground up. The rationale for that is simple. Most board would now allow a treasury team to run a derivatives book. Squaring exposure to zero through a counterparty is permissible. Running a book with net exposures in most instances is not.

Treasuries also quite often assume that the client has done appropriate diligence on the transaction and the trade and understands the buyer beware language in the term sheet and the ISDA master contract.

For clients costs drive the conversation. More often than not, the clincher for the client is zero cost. The road to exotic graveyard is littered with “I don’t want to pay for the structure” statements.

To walk a balancing line between these counterpoints is awkward at best, openly hostile at worst.

Our thesis is that while zero cost structure appear to be fairly attractive clients tend to shoot themselves first with their willingness to dabble with increasingly level of toxicity. Paying a little extra can create equally attractive solutions that are easy to structure, improve hedge effectiveness, are unlikely to blow up on customer balance sheets and yet make money for treasury and relationship management teams. But all of that goes out of the window when a client insists on not being out of pocket for hedging their exposures.

One way to answer this question is to put together a simplified model and simulate hedge effectiveness across a range of simple, vanilla and exotic products. We thought we would run such an exercise for a simple transaction and look at the actual out of pocket cost paid by a client over the life of the transaction. Are we better off with exchange traded vanilla contracts? Are exotic contracts all that they are made out to be? Let the simulator decide.

The game plan.

We have put together a hypothetical case that we discuss and review over three posts. In our first post we set the context for our case. In the second post we discuss the results. In the third and final post we reach for conclusions.

We will also do a high level review of the underlying model in a separate post after the case has been presented. That modeling review is optional and please feel free to skip it.

For the purpose of this case the hat that we are wearing is that of an adviser helping a client pick the right structure based on his hedging needs. Not the bank but effectively sitting between a bank and the client answering questions.

The transaction

Our client is an automobile importer in Dubai who imports 50 high end and midrange Japanese vehicles from Toyota every month. While his extended payment terms allow him to pay within 180 days at any given month he has a substantial amount of exposure to changes in the value of USD-JPY exchange rate because of his outstanding order book. Historically speaking using the last 12 months as a baseline he tends to import 50 vehicles a month and need to remit between 100 – 200 million yen a month, every month. For example end of June this month he has to pay 200 million yen for the cars imported in January 2017. Similarly end of July the payment for the lot imported in February would be due.

Since the UAE Dirham (AED) is pegged to the US dollar (USD), it make sense to work with the USD-JPY market because it is significantly more liquid than AED-JPY. It introduces some basis risk but given the fact that the structures we are working with have a maturity horizon of less than one year the basis risk is assumed to be acceptable.

While the client is only evaluating the next few settlements right now he is open to longer term structures that are proven to be cost effective and are not likely to blow up with changes in market volatility. The client is also quite concerned about products and tools that open him up to potential future liability, especially with changes in implied volatility. His current conflict lies between buying a series of vanilla calls versus a combination of TARF and participating forwards.

Who are we?

We are not the bank selling the solution since treasury mandates do not allow advising customers on products and structures. Treasury sales teams are allowed to sell and buy products and structures but advisory relationships tend to run into product liability issues. Internal policy and compliance guidelines prohibit the sales team from actually advising and suggesting a solution to a customer.

Hence the need for an independent advisor to step in, evaluate the range of structures available and suggest preference for a given solution. Enter our exotic FX structure modeling and advisory team.

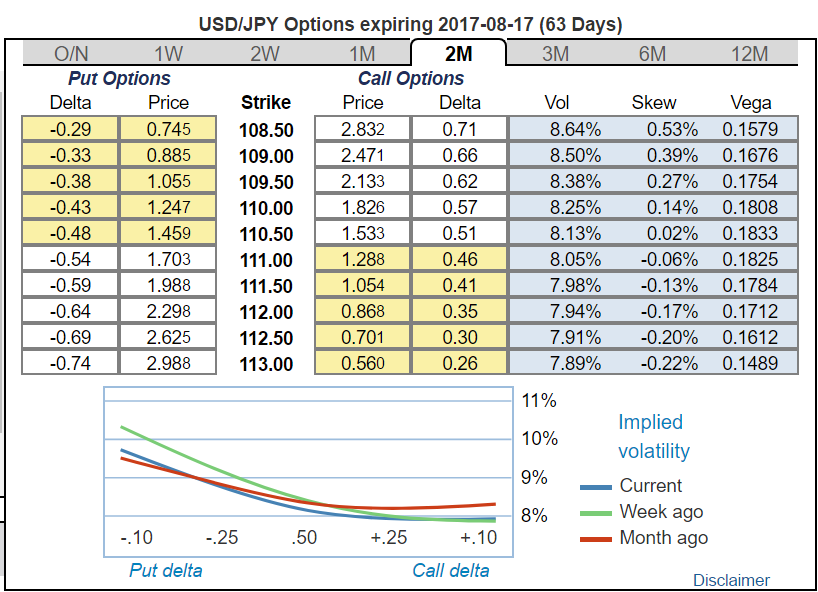

USD-JPY Price volatility

The USD-JPY exchange rate has been incredibly volatile and cyclical over the last 3 years. From seeing a high of 100 yen to a dollar to a low of 125 yen to a dollar. While historically our client has left his exposure unhedged given the shifts in volatility and his core business he is now a little worried about his conventional approach.

Our client would like us to roll out a model for the full range of products and solutions available and compare their hedge effectiveness for his CFO. The client feels that a little bit of upfront analysis before the transaction is executed will likely lead to a less painful future and will give him a better idea of which product would ultimately best serve his interests.

The product universe

For the purpose of our simulation model our product universe includes the following available solutions. We do a quick review of the products so that we understand the results from our simulation exercise in our next post.

Standard forward contract – default structure

The client has the right to buy JPY against USD at a rate agreed upon today on a future date. For instance, for the month end settlement, the client can lock in the rate today at 109.2 whereas the current spot rate is 109.66.

Irrespective of where the market is at the end of the month that client will have to buy 200,000,000 JPY at the agreed upon forward exchange rate of 109.2. There is no cost to enter into the forward contract. There may be a difference between the contractual rate (strike rate) and the market rate at the time of exercise. The downside is when the market moves against the customer (cheaper to buy from the market rather than through the forward contract).

For instance it is possible that on the exercise date the actual spot rate is 115.02 JPY to a USD. In this scenario it would have been cheaper for the client to buy from the market at the spot rate rather than at the agreed upon rate of 109.2. The difference (115.02 – 109.2) is the downside of the forward contract.

Vanilla call and put options – structure A

Rather than being obligated to buy at a fixed exchange rate of 109.2 YEN per USD, the client can also purchase a call option on JPY. The option will only be exercise if JPY appreciates against USD. If JPY depreciates the client can buy from the market at the market rate. There is a premium associated with the purchase of the call option that can be expressed in absolute terms or as a percentage of notional amount.

For instance in the case of the forward downside if the actual exchange rate on the day of exercise is 115.02, the client doesn’t need to buy using the option contract. He can simply buy from the market.

Participating forward – with cost – structure B

To reduce the effective cost of the premium associated with the call option, the client can also opt for a half and half strategy. He can buy a forward contract on JPY 100 million and a call option on the remaining 100 million. This way he has hedged the full exposure against unfavorable currency exchange movement but has limited downside exposure when the market moves against him. The strike price of the forward contract and the call option are the same. This means that the forward contract will most likely be an off market forward contract. An off market forward contract will result in a debit or a credit to the client account depending on the direction of the rate.

Since the objective is reduction of average cost and improvement of hedge efficiency, the structure is not a zero cost structure. A portion of the call option premium may be offset by the credit generated by the off market forward contract but the client will have to pay an out of pocket amount to enter into the structure.

In this structure the client is both long JPY Forward and long JPY call option. When the market is in the client favor (JPY has appreciated) he will buy JPY 200 million using the structure. When the market is not in client’s favor (JPY has depreciated) he will buy JPY 100 million using the structure and the other JPY 100 million from the market at the lower rate.

Participating forward – with zero cost – structure C

Similar to structure B but with a different orientation. The primary objective here is zero cost and not hedge efficiency. Which means that while the client will purchase one leg, the cost of that leg will be funded or offset by selling (shorting) the second leg. The structure will still be based on a vanilla call and an off market forward contract. However the net cost will be reduced to zero or as close to zero as possible.

Vanilla TARF – structure D

Take the participating forward (structure B) from above and rather than buying just one leg, buy 12 legs for each of the upcoming 12 monthly settlements. The idea is that rather than buying 12 options you buy one with 12 settlements. Allows you to average out your cost over 12 settlements.

Depending on the objective of the hedge the TARF may combine off market forwards contracts with long or short calls or puts for each leg. While the exact specification of TARF and participating forwards will differ from one term sheet to the next we have intentionally used simplified structures to illustrate a point.

KIKO TARF – structure E

A knock in knock out TARF that gets knocked in when rates reach a certain threshold and gets knocked out when the customer has benefited to a certain amount.

Asian option – structure F

Rather than buying 12 legs buy one contract that would average out 12 settlements over a given year. While an Asian option can only be purchased using OTC contracts, TARF make it possible to put together a crude proxy that can try to replicate an Asian payoff.

Unhedged spot – baseline

We will compare the numbers and the payoff from each of the above structure against the baseline choice – leaving our exposure completely unhedged.

The assignment

The assignment should you chose to accept it is to build a simple Monte Carlo simulation model that will simulate implied forward exchange rates and the potential all in cost of leaving the client exposure unhedged versus using any one of the above structures to hedge the transaction. When you are done you should be able to answer the client’s primary question. What should he buy? Vanilla calls or a combination of TARF and participating forwards.

You have 24 hours. On your marks, set, go.

This case study is part of the final assessment of a group of treasury students. The three part series will be updated over the next three days as different components of the exam are released to the students being tested. You are welcome to attempt the exam with them. The final solution will be posted on Monday – Tuesday morning. Best of luck.