CIR Interest Rate Model

5 mins read The Cox-Ingersoll-Ross, CIR, interest rate model is a one-factor, equilibrium interest rate model. One factor in that it models the

5 mins read The Cox-Ingersoll-Ross, CIR, interest rate model is a one-factor, equilibrium interest rate model. One factor in that it models the

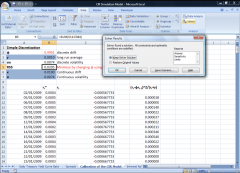

2 mins read Addendum: How to conduct a Principal Component Analysis in EXCEL There are a couple of problems that the user may

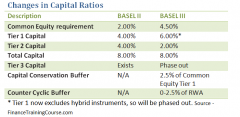

4 mins read In preparation for Basel III and the requirements for banks to hold higher (and better quality) minimum amounts of tier-1

10 mins read Asset Concentration Limits: Limits set to control the amount of any particular asset held by the company usually applied to more

4 mins read The mandate of the ALM (ALCO) committee has increased with changes in the Basel II framework to accommodate liquidity and funding concentration concerns. Commonly known as Basel II extensions or the Basel III framework, the changes put a renewed focus on liquidity coverage ratio and funding concentration. To be fair both interest rate mismatch and liquidity profiling were already areas of focus under the original Pillar III Internal Capital Adequacy Assessment Process requirements.

5 mins read Calculating EAR Earnings-at-Risk (EAR) is computed in order to evaluate the impact of interest rate change on earnings. The approach