BASEL III Updates – November 2014

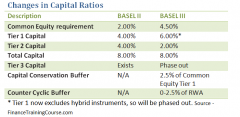

4 mins read In preparation for Basel III and the requirements for banks to hold higher (and better quality) minimum amounts of tier-1

4 mins read In preparation for Basel III and the requirements for banks to hold higher (and better quality) minimum amounts of tier-1

4 mins read The mandate of the ALM (ALCO) committee has increased with changes in the Basel II framework to accommodate liquidity and funding concentration concerns. Commonly known as Basel II extensions or the Basel III framework, the changes put a renewed focus on liquidity coverage ratio and funding concentration. To be fair both interest rate mismatch and liquidity profiling were already areas of focus under the original Pillar III Internal Capital Adequacy Assessment Process requirements.

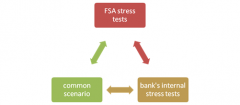

5 mins read Stress testing refers to a process through we which we try and assess the impact of abnormal and extreme conditions on our processes, control systems and organizations.

Within financial services stress testing takes a second dimension where the focus shifts from assessing impact to identifying breaking points; the maximum amount of stress a financial institution would be able to bear before it breaks down and fails. The level of interconnectivity between financial markets and institutions has made this threshold of failure even more important since a since the failure of a single institution can trigger a deep and painful system wide crisis that can very easily turn into a regional or global contagion.

2 mins read Trailing volatility or Volatility Trend Analysis Trailing Volatility or volatility Trend Analysis is the analysis of volatility trend lines. Volatility

3 mins read The put premium gives the conditional expectation of loss beyond the worst case loss, if the worst case loss occurred.

3 mins read Sharpe Ratio The Sharpe Ratio measures total risk-adjusted return. The value specifically is the ratio of excess return over the