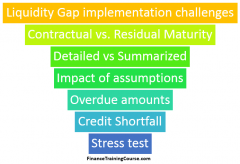

Liquidity Gap Implementation Challenges

5 mins read A quick review of common liquidity gap implementation challenges as part of the bank asset liability management platform implementation. What is

5 mins read A quick review of common liquidity gap implementation challenges as part of the bank asset liability management platform implementation. What is

3 mins read I have long felt a need for a high level overview course on ALM training for board members, executive committee

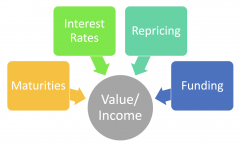

4 mins read NII, Earnings, Gaps, Asset & Liability Sensitivity In our previous post, we encountered the curious case of interest rates rising

6 mins read The two elements used within bank ALM analysis are Economic Value (EVE) and earnings as given by Net Interest Income

3 mins read Asset Liability Management Training Guide. 3rd Edition. The brand new, revised 3rd edition of the ALM Study Guide is out.

3 mins read Why ALM? This post looks at ALM’s purpose, the principal ways banks make use of it, and its core drivers.