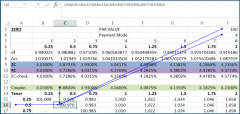

Bootstrapping the Zero Curve and Forward Rates

6 mins read Deriving zero rates and forward rates using the bootstrapping process is a standard first step for many valuation, pricing and

6 mins read Deriving zero rates and forward rates using the bootstrapping process is a standard first step for many valuation, pricing and

3 mins read This post is a continuation of our earlier post that describes the usage of historical simulation for VaR calculation of

2 mins read Valuing and marking to market over the counter interest rate (IRS) and cross currency swaps (CCS) has always been a

3 mins read And now for the last and final part of our Practice Exam Test Question series on how to price &

4 mins read Here is an abbreviated partial solved solution to the practice exam question posed earlier. The practice exam question was used

2 mins read I teach the Derivative Pricing and Risk Management courses to EMBA and MBA students in Dubai and Singapore. In a