Option value is dependent on the following variables:

- The current spot price of the underlying security

- The strike price at which the option has been struck

- The price volatility (Vol) of the underlying security

- The risk free interest rate

- The time to expiry

- The dividend yield on dividend paying securities

Option value changes when any of the above variables change. The magnitude of the option value change depends on where the option is in terms of “money-ness” and the variable in question.

Option Price Drivers – Money-ness

Money-ness is a function of how far the strike price is from the current spot price. For call options:

a) When the strike price is greater than the current spot price and based on volatility levels it would take a large price movement for the option to expire in the money, the option is deep out of money.

b) When the strike price is less than the current spot price and based on volatility levels it would take a large price movement for the option to expire out of money, we say the option is deep in the money.

c) When the strike price is close to spot price in either direction, the option is regarded as at or near money.

Deep out of money options increase more in value for changes in volatility and spot price levels compared to at or near money option. While they have a higher probability of expiring worthless if you can trade premiums deep out of money options also generate higher trading profits in relative terms for the similar increases in volatility and price levels.

Pricing Models

There are three pricing models available for determining option value. They are:

- The Black Scholes formula for European Call and Put Options

- Binomial Trees for American & Exotic Options

- Monte Carlo Simulation for Exotic Options

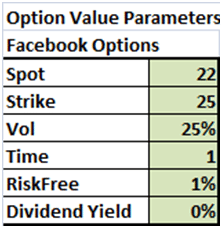

Option Price Drivers – Facebook Call Option example

Let’s take a look at a simple example using a American call option issued on Facebook. For our Facebook option value example we will use Binomial Trees for valuing American Call Options issued on Facebook. The parameters used for Option Value are given below:

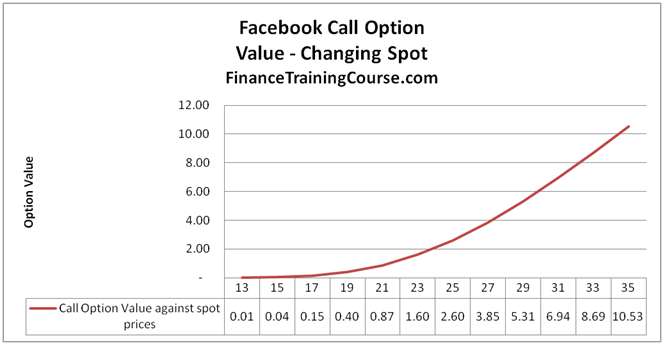

Here volatility refers to implied volatility and Time refers to time to maturity of 1 year. The starting value of the call option using the above parameters is US$1.202. As we change the spot price of the underlying Facebook share, the option value from 1 cent a share at $13 dollars to $10.53 a share at $35 dollars as show below.

If the underlying share hits $35 and you were to exercise the call option immediately, cash received by exercising the option would be $ 10 dollars. Facebook share is worth $35, the strike price is $25, you could buy the share for 25 and sell it immediately in the market for 35 to book a cash gain of $10 (ignoring premiums).

But the option is worth $10.53. The extra 53 cents represent the intrinsic value of the option because as long as there is time available till expiry, the underlying can still increase (or decrease) in value and change the final payoff from exercising the option.

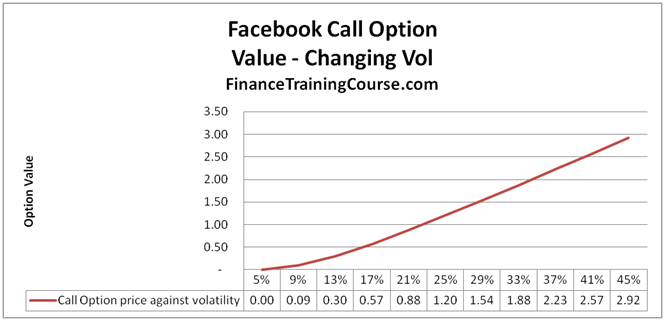

Examining the impact of volatility

Our second example looks at the impact of changing volatility on Option Value while holding all other parameters constant. Using the same parameters as above we calculate the value of a call option by changing volatility levels. Option value moves from 0 cents at 5% volatility to $2.92 dollars at 45% price volatility.

There are many ways that you can calculate volatility but for option pricing, the only relevant measure is implied volatility. Implied volatility is the volatility level at which the price generated from your model and the market price match.

Volatility measured using historical price levels and returns is known as empirical or historical vol and while relevant and useful for analysis and discussion is not applicable for measuring the market price of an option. Just because historical volatility levels have been high, does not guarantee that they will be high in the future and vice versa. The market uses implied volatility as a measure of the volatility level the market is comfortable trading at for Facebook shares.

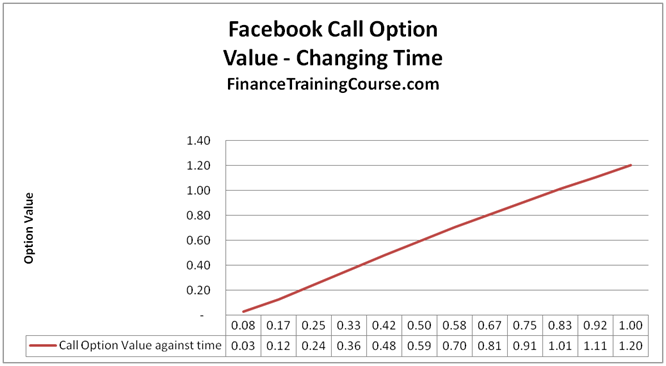

Examining the impact of time

Our third example looks a the impact of changing time to maturity on option value. We move time to expiry from one month (.0833) to one year (1.0) and track the change in the value of the call option on Facebook.

You can see that unlike volatility and spot prices, the relationship with time is almost linear.

To track changes in option value and extend this analysis to interest rates and other relevant parameters it is important to build an intuitive understanding of option pricing, option price sensitivity and option pricing models. Option Greeks simplify that analysis by examining the impact of each of the above drivers on the option price. Also, check out: