I am often asked if there is a suggested sequence that I would recommend to finance newbie(s) when it comes to picking up risk, derivative pricing & valuation concepts in a rush. When I teach the Quant evening crash course, I start with basic products and then jump straight into building pricing models in Excel. Over the years I have realized that the only way to teach this subject and help students retain this topic is to let them build their own models.

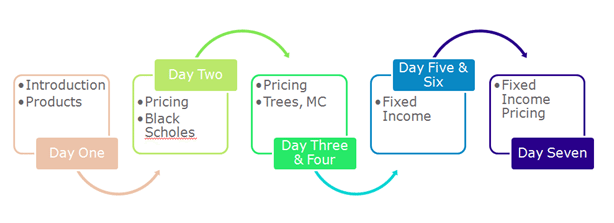

If you are thinking about jumping into the world of Quantitative Finance this weekend, the following collection of posts roughly follows the direction I use in class when I teach the 18 hour derivative pricing and models course at the SP Jain Campus in Dubai and Singapore.

Take a night each for topics below, repeat as much as necessary and follow through with building your own excel spreadsheets.

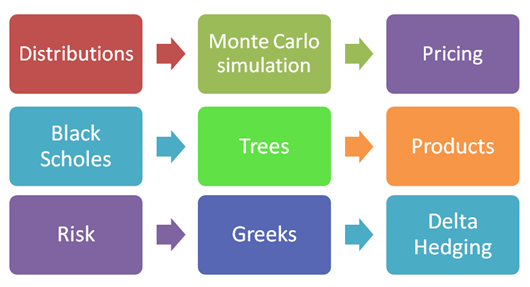

Risk & Quant Training Day One – Introducing Monte Carlo Simulation

Some overlap. The first link takes you to the resource page for building MC models as well as their extension in the interest rate simulation world. The second is a complete collection of everything we have ever written on MC Simulation on this blog.

- Monte Carlo Simulation Guide

- Monte Carlo Simulation Post Collection

Risk & Quant Training Day Two – Pricing and Black Scholes

Option Pricing review and a quick recap linking the Black Scholes model with Trees and the Monte Carlo simulation (MC) world.

Risk & Quant Training Day Three – Exotics

A products terminology crash course, some advanced topics

- The Derivative Products Universe

Risk & Quant Training Day Four – Risk Management & Value at Risk (VaR)

Everything you ever wanted to ask about value at risk and risk management but were afraid to ask.

Risk & Quant Training Day Five – Greeks & Delta Hedging

Proceed at your own risk. Advanced Topics. Need a quiet corner and repeat readings.

Comments are closed.