A collection of everything we have ever written about understanding Delta, Gamma, Vega, Theta & Rho (the Greeks). To help you prepare for your upcoming Sales & Trading interview at the Sales & Trading desk.

Understanding Option Greeks – Relevant Sales & Trading Interview Guides prior posts

Understanding Greeks – Introduction

Understanding Greeks – Analyzing Delta & Gamma

Understanding Greeks – The Guide to delta hedging using Monte Carlo Simulation

Understanding Greeks – The Delta Hedging Simulation extended for Put Options

Understanding Greeks – Quick Reference Guide to Delta, Gamma, Vega, Theta & Rho

Delta Hedges – Cash PnL (Profit & Loss) Calculation Simulation for a Call Option

Understanding Greeks – The analysis framework for interview prep

Evaluate an option’s in the Moneyness.

a) Is it Deep Out (Will it take a big move for it to expire with some value at maturity?),

b) Deep In (Will it take a big move for it to expire worthless at maturity?),

c) At or Near Money (the spot price is now close to or very near the strike price?)

Then think about how the Greek in question will behave against a change in the following:

a) Spot prices

b) Strike price

c) Implied volatility

d) Time to maturity

e) Interest Rates

Calculate & plot the results for each (Delta, Gamma, Vega, Theta, Rho) in Excel. That is the only way you can decode and get comfortable with the material. Irrespective of how much you read, till you actually build the sheet by hand, the Greeks will not open up.

Greeks Pop Quiz – Put your thinking hats on

Here is quick pop quiz. Please note that these are not interview questions. They are question that will help you assess what proportion of the material covered in the above posts have you actually digested?

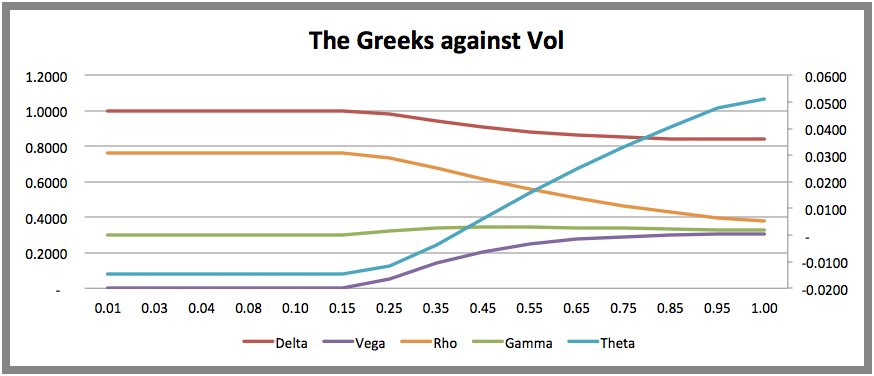

Take a look at the following image. We have plotted all five Greeks against changing levels of volatility.

Figure 1 Understanding Greeks – Plotting Greeks against implied volatility

Here is the first question. The option that has been used for this plot is:

a) Deep In the Money

b) Deep out of Money

c) At Money

d) Near Money

Second question. Using the same graph above think about the relationship between Gamma & Theta. How will this relationship change if the underlying option is deep out, deep in, at or near money.

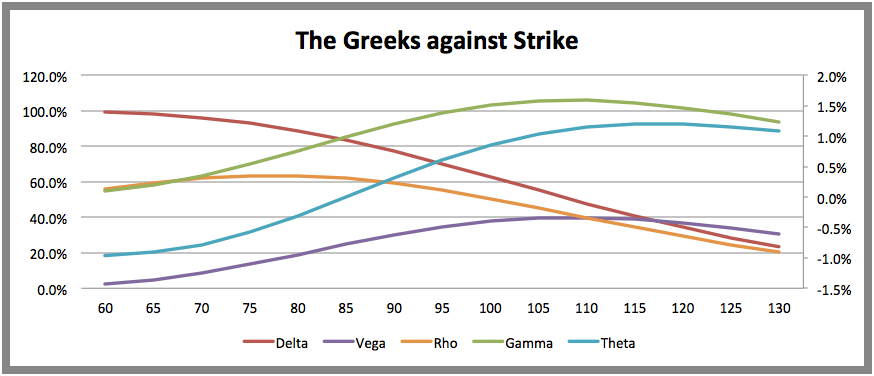

Third question. Look at Gamma’s plot against strike. What do you think is happening here? How does that impact profitability? What is the best and most cost effective way of hedging this risk?

Fourth Question. Now take a look at all the Greeks against strike. You have already looked at the relationship between Gamma & Theta. Why does Vega’s plot also has a similar shape?

Figure 2 Understanding Greeks – Plotting Greeks against strike

Go ahead and build an Excel spreadsheet that allows you plot the Greeks against changing interest rates, time to maturity and spot prices. When you are done come back and we will take the next step for your interview prep. Also keep an eye out for updates posted on this page.

Comments are closed.