Portfolio alpha stability and allocation optimization models.

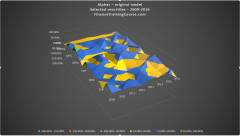

6 mins read Stability and robustness of portfolio Alphas – the excess return metric – and its implication for portfolio allocation and optimization

6 mins read Stability and robustness of portfolio Alphas – the excess return metric – and its implication for portfolio allocation and optimization

7 mins read Big Short Takeaways for investors and traders – II Part two of our three part series on The Big Short

8 mins read For value investors and portfolio managers For portfolio management and fixed income students the 2008 – 2009 financial crisis represents

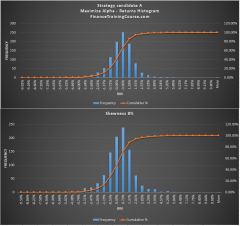

5 mins read So far in the portfolio optimization course our focus has been on single dimension analytics. With both risk and performance

3 mins read This is a sample portfolio management and optimization assessment exam used for the Executive MBA version of the course. Enrolled

3 mins read As part of our case discussion in the Portfolio Optimization course, we proposed a simple question to eighteen odd apprentice