Solved Solution for Value at Risk (VaR) Margin Lending Margin. Prime Brokerage Case Study

36 hours ago we posted our Value at Risk (Margin Lending applications for Prime Brokerage) question and case study as part of the weekend Quant Challenge series. Here is the high level solution for the questions and some pointers. For those of you who missed the original post, the case is reproduced at the end of the solved solution.

The original data set for the case study download link – Gold oil and WTI price series

Value at Risk Margin Lending Prime Brokerage Case Study Practice Test Questions

a) Volatility for Oil and Gold for the complete period of the data set (10 points)

Preferred Solution to the Case Study Question – Calculating Volatility

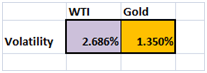

While it would have been enough to simply quote SMA daily volatility of 2.686% for WTI and 1.35% for Gold, it would be better to also calculate trailing volatility for 2, 4 or 6 weeks and present it for use later in the case study.

Figure 1 Volatility for Case Study data set – WTI & Gold Spot prices

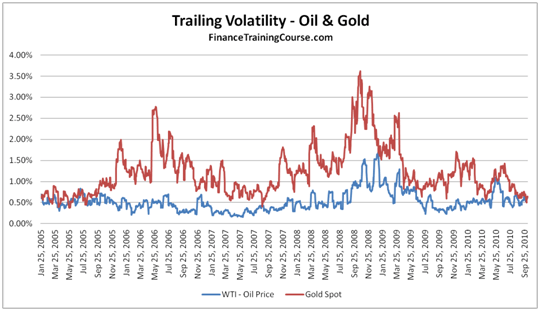

Figure 2 Case Study – Trailing Volatility for WTI and Gold Spot prices using a 2 week moving window

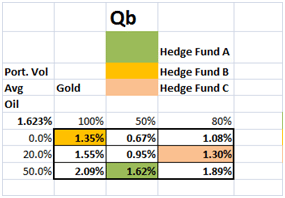

b) Portfolio volatility for Hedge Fund Manager A, Hedge Fund Manager B and Hedge Fund Manager C (15 points)

Solved Solution to Picking Portfolio Volatility – Min, Max, Average or something else

The fastest way of answering this question is through a simple data table and a color code representing each Hedge Fund Manager. Rows and Columns are the two respective commodities. You obviously can’t scale this approach to more than two commodities but for this specific case study question, a data table is the way to go. We have used Value at Risk – Portfolio Shortcut approach to calculate Value at Risk using Variance Covariance (VCV) method.

Figure 3 Portfolio Volatility – Oil & Gold

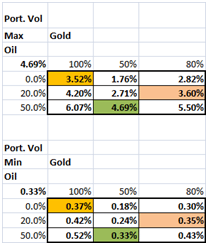

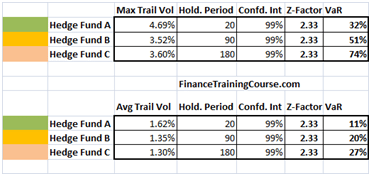

However a better and preferred solution would be to also work with maximum and minimum volatility thresholds

Figure 4 Portfolio Volatility – Oil & Gold @ Min and Max Vol levels

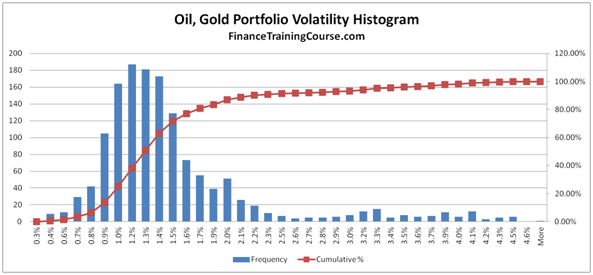

A perfect solution would take this one step further and generate a histogram of trailing volatility which gives us a better and more complete picture than a simple minimum, maximum or average volatility pick. The histogram below shows you clearly that median volatility is between 1% and 1.3%, that you are likely to see jumps to 2.5% to 3.3% quite frequently and possibility of seeing daily volatility levels of 4.6% and higher.

Figure 5 Portfolio Vol – Histogram – Tracing median volatility and the long tail effect

If you didn’t make the jump to trailing volatility earlier you will never reach the perfect solution. You will also need this when you see the impact of your suggested Margin numbers in the next case study question and get skewered by your board for suggesting impractical thresholds that will kill the underlying business.

c) Suggest a suitable deposit (margin account / account equity) that each hedge fund manager should agree to make before your desk will release funds? (10 points).

Should this deposit (margin) be linked to the holding period of trades or the number of days it would take to liquidate the position? (5 points). The objective of the margin is to secure the interest of the desk and protect it against adverse price movement if the desk is forced to liquidate the position of the hedge fund.

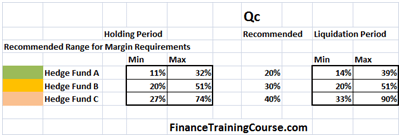

Suggested Margin requirement for Hedge Fund Margin lending business

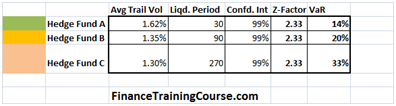

Here is the sufficient solution if you decided to use holding period. We use Value at Risk as a proxy for Margin requirements. We have used 99% here as an illustrative confidence threshold, in real life you are more likely to use 95%.

However the right approach is to use estimated liquidation period based on trading volume or turnover and estimated impact costs. You can also see that we have used both maximum volatility and average volatility levels.

Figure 6 – Value at Risk and suggested Margin requirement for Margin lending

This is where the median volatility levels calculated above (take another look at the histogram) come to your aid and allow you to suggest usage of average volatility levels rather than maximum trailing historical volatility.

Figure 7 Volatility & Margin Lending Margin Requirements – Suggested using average or median volatility

Alternate solutions – Margin Lending – Prime Brokerage – Margin Requirements

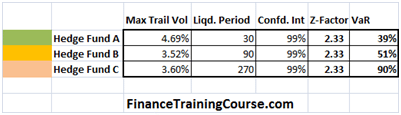

You can actually go ahead and even suggest margin thresholds or margin lending using maximum volatility levels but you will get laughed out of the board room based on your impractical suggestion. It is an acceptable examination solution but a suicidal real life suggestion.

Figure 8 Value at Risk based margin requirements – using maximum trailing volatility

If you are thoroughly confused and not sure, the safest solution would be to simply put the ranges out there and then quote your recommendation so that you can hedge your bets.

Figure 9 Alternate solution – Margin requirements for margin lending using value at risk

d) Your technology and operations team suggests that in order to reduce the systems overhead, only one margin requirement should be charged across all customers and commodities. Your sales team agrees. Is this a good idea or bad idea? In 100 words or less describe your reasoning (10 points)

The simple, clear & concise answer is no, using one margin threshold across all products and customers is statistically incorrect. The correct practical answer is that while you can get away with different margin requirements across different products, doing the same across different customers may bring its own challenges. For the exam test question there was no right answer. The objective of the question was to see how you would respond to the challenge.

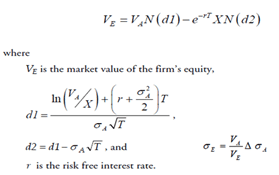

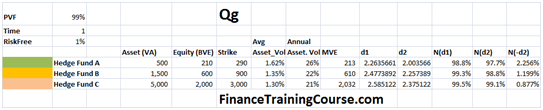

e) Using the Black Scholes Merton Structured approach, calculate the probability of default for each Hedge Fund under your suggested Margin regime? (30 points)

For background on using Merton Structured approach for calculating probability of default see the Advance Risk Management models page.

Figure 10 Merton Structured Approach – Using Black Scholes to calculate probability of default

Figure 11 Calculating Probability of default for margin lending customers

The trick here was acknowledging that the volatility you were calculating were actually asset vols so there was no need to do the iterative Asset/Equity Vol calculation required for the Merton approach. You could go directly to the solution.

Presenting Results to the Board – Margin Lending – Margin Requirements – Prime Brokerage – Hedge Funds – Probability of Default

The last three sections were the toughest sections to tackle and answer. Here are the questions and the solved solutions.

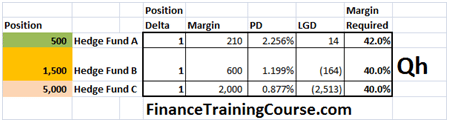

f) Using Value at Risk as a tool, create a simple model for calculating Loss Given Default (LGD) for each of the three Hedge Fund Managers.

g) Your Margin requirement regime has now been reviewed by the Board of Directors and in their infinite wisdom that Board has suggested a change in your calculation process. Margin requirements should now be set in a such a fashion that the probability of default (PD) measure as per your PD model should not exceed 2% for any client. In addition loss given default after taking the margin under account should not exceed 5% of net exposure. Please recalculate your margin requirements and share your results.

h) With your new margin requirements do all hedge fund managers now represents equal risk? Plot the four elements above in the form of a graph against rising and declining volatility. Or is there a difference between them? Which one of these would you like to lend more? Exposure to which one of these should be reduced? (25 points)

Figure 12 – Margin Lending – Margin Requirements – Loss Given Default (LGD) – Position Delta

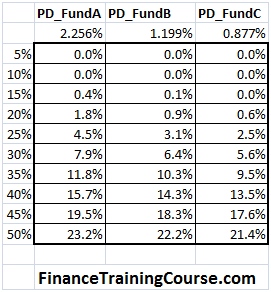

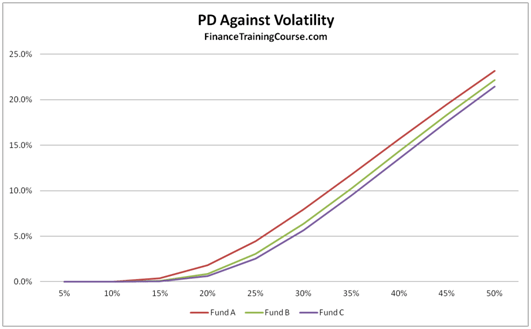

Figure 13 Margin Lending – Margin Requirement – Hedge Fund Probability of Default (PD) across Vol levels

Despite the higher Loss Given Default (LGD) and the size of the exposure from PD point of view customer C (Hedge Fund C) is the preferred customer.

The Value at Risk (VaR) Margin Lending Prime Brokerage Case Study

You are the head of Risk Management responsible for managing risk exposures at the Prime Brokerage desk at a large un-named bulge bracket investment bank on Wall Street. Three of your customers are Hedge Fund Manager A, Hedge Fund Manager B and Hedge Fund Manager C who all specialize in large, leveraged commodity trades.

The Prime Brokerage desk lends money on margin to hedge fund customers. As the Head of Risk Management it is your responsibility to decide and recommend a suitable margin haircut requirement in all margin lending transactions. As part of your agreement, the amount is lend against the security value of the account (the value of the commodity position) and will be liquidated if margin falls below a certain threshold. As the bank in question you are reputed on the street as “the” bank that hates writing off capital – (it is a capital offence) and since you report directly to the Board Risk Management Committee, your primary objective is to reduce the probability of capital loss.

| Risk Parameters | Hedge Fund Manager A | Hedge Fund Manager B | Hedge Fund Manager C |

| Commodities Traded with portfolio weights | Oil (50%), Gold (50%) | Gold (100%) | Gold (80%), Oil (20%) |

| Holding period of Trades | 20 days | 3 months | 6 months |

| Equity in Trades | 10% | 5% | 5% |

| Liquidation days (based on size of position as a percentage of market volume) | 30 days | 90 days | 270 days |

| Size of position | 500 Million US$ | 1.5 Billion US$ | 5 Billion US$ |

The attached MS Excel sheet includes the relevant data set (commodity prices for Gold and Oil). Please use the data set to calculate.

Value at Risk Margin Lending Prime Brokerage Case Study Practice Test Questions

a) Volatility for Oil and Gold for the complete period of the data set (10 points)

b) Portfolio volatility for Hedge Fund Manager A, Hedge Fund Manager B and Hedge Fund Manager C (15 points)

c) Suggest a suitable deposit (margin account / account equity) that each hedge fund manager should agree to make before your desk will release funds? (10 points).

Should this deposit (margin) be linked to the holding period of trades or the number of days it would take to liquidate the position? (5 points). The objective of the margin is to secure the interest of the desk and protect it against adverse price movement if the desk is forced to liquidate the position of the hedge fund.

d) Your technology and operations team suggests that in order to reduce the systems overhead, only one margin requirement should be charged across all customers and commodities. Your sales team agrees. Is this a good idea or bad idea? In 100 words or less describe your reasoning (10 points)

e) Using the Black Scholes Merton Structured approach, calculate the probability of default for each Hedge Fund under your suggested Margin regime? (30 points)

f) Using Value at Risk as a tool, create a simple model for calculating Loss Given Default (LGD) for each of the three Hedge Fund Managers.

Loss Given Default would be based on the worst case price that you would end up selling the Hedge Fund’s commodity portfolio if they fail to meet a margin call. Your holding period as the bank would be based on the liquidation period required to liquidate the portfolio and you would be subject to inventory losses on account of volatility as you try to sell the portfolio. Your loss should partially (or completely) be offset by your customers margin deposit. (15 points)

g) Your Margin requirement regime has now been reviewed by the Board of Directors and in their infinite wisdom that Board has suggested a change in your calculation process. Margin requirements should now be set in a such a fashion that the probability of default (PD) measure as per your PD model should not exceed 2% for any client. In addition loss given default after taking the margin under account should not exceed 5% of net exposure. Please recalculate your margin requirements and share your results. (30 points).

h) For a presentation to your board, in a simple table present a side by side comparison of the following metrics for each of the hedge fund manager

- Position Delta (%)

- Margin requirement

- Probability of Default

- Loss Given Default

With your new margin requirements do all hedge fund managers now represents equal risk? Plot the four elements above in the form of a graph against rising and declining volatility. Or is there a difference between them? Which one of these would you like to lend more? Exposure to which one of these should be reduced? (25 points)

Comments are closed.