Here is the course on pricing IRS (Interest Rate Swaps) and CCS (Cross Currency Swaps) divided into three separate sections that address basics of interest rate swaps, term structure modeling, bootstrapping zero and forward curves and mark to market and valuation.

We close the session with a short two step case study that walks through the process of building the forward curve and completing an MTM exercise for a Swap using a live example presented as a test question.

Introductions

A short review of the pricing process and swap terminology. Feel free to skip if you are already comfortable with the language.

Modeling the Zero & Forward Rate Term structures for pricing IRS

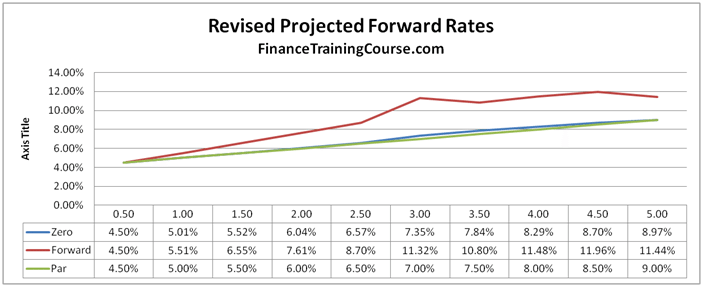

Plot zero and forward curve using the bootstrapping process in Excel. A step by step guide to building your Excel spreadsheet.

Pricing IRS & CCS

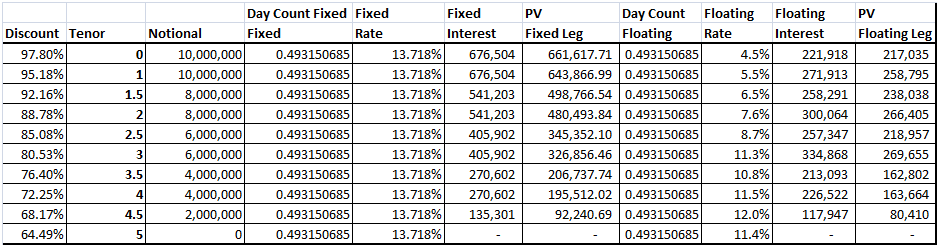

Extending the material covered in section II above. Review MTM & Valuation.

MTM & Valuing IRS – Case study

A detailed case study that walks through the topics covered in prior sections using a detailed step by step case study. The case study is a sample exam used for assessment in the derivative pricing course taught by yours truly at EMBA and MBA programs in Singapore.

- Pricing Interest Rate Swaps – Bootstrapping Zero and Forward Curves

- Pricing Interest Rate Swaps – MTM & Valuation Partial Solution

If you liked this material you may want to check out our other risk and treasury case studies covering option pricing, Monte Carlo simulation, Asset Liability Management, Value at Risk, Capital Adequacy, risk management and EXCEL Hacks

For a complete reference to equations and calculator referred to in this course, please see the Derivative Pricing and Financial Risk Equation Glossary.

For topic specific equations, please see the following links:

- Calculating Value at Risk

- Duration, Convexity and Asset Liability Management

- Black Scholes, Derivative Pricing, Binomial Trees

- Calculating Forward Prices and Forward Rates

- Valuation of Interest Rate Swaps and Future Contracts

- Financial Risk, Reward metrics and measures

- Black Formula’s, Valuing Interest Rate Caps and Floors