Doha Oil Output Freeze talks. 7 Questions for Oil trading playbook in April.

On April 17th 2016 a dozen key oil producers, OPEC members and non-members, will meet in Doha, Qatar to discuss the future of oil prices. The big item on the table is the crude oil production output freeze that has been in and out of news since the beginning of this year and a public stance worth a billion dollars a day.

News reports indicate that the items on agenda are follow up discussions on the length of the production cap and its implementation in the coming months, primarily between Saudi Arabian and Russian delegates. The other fourteen producers excluding Iran, Libya and Iraq have already indicated a willingness to follow the path set by the two leading producers in the world.

Ahead of the Doha meeting, here are seven questions for your oil trading playbook for the week starting Monday.

- Will the Saudis attend? Yes, but expect a fair bit of fireworks before the meeting as Iran and Saudi Arabia are likely to trade jabs and release news to create pressure on other partners at the producers’ conference. The Saudis are big believer in indirect communication before and after negotiating events and are likely to use this medium again to communicate their official and unofficial stance.

- Will the Iranians attend? Yes, but see above. There is a complex background ballet at work between the new oil triumvirate comprising of Saudi Arabia, Iran and Russia. Saudi Arabia, Iran and Russia control the excess marginal supply today and in the coming months. While Libya and Iraq are factors in the equation, their ability to significantly add to oil output in the next six months compared to the top three is limited. Iraq has been adding capacity in 2015 and will add more in 2016, but it has been plagued by security and law and order challenges.

- Will there be a big announcement? Yes, that is the objective of the entire production in Doha but don’t read anything into it.

- Will they commit to a freeze? Yes, but enforcement is going to be another story. The Russians would like the world to believe that they are committed to it. The Saudis would want to make it work but only if everyone else plays fair. Iran and Iraq are more than happy to make soothing comments as long as they are not bound to a freeze and prices rise. Everyone is waiting for the big producers to work it out between themselves so that prices can finally settle above their current lows.

- Will oil prices rise? Yes, leading up to the meeting, absolutely yes. Subject to the fireworks mentioned above. You also have to understand the Russian, Iranian and Iraqi mindset. A ten dollar increase in crude oil prices that can last a month adds an additional one hundred million dollars a day to Russian oil revenues. Given the state of Russian finance that is much needed relief. For the global community of oil producers it represents a bump of 900 – 940 million dollars a day depending on how their respective blends are priced with respect to the benchmark. Expect a number of press conferences leading up to the event with language and gestures geared towards bullish sentiments. Words are cheap; especially if they don’t cost anything and the posturing add up to a billion dollars.

- For how long? The forecast window for oil is about two to six weeks. The next OPEC meeting is scheduled for 2nd June 2016. US refinery turnarounds end first quarter and the crude stock draw down that surprised everyone this Wednesday is likely to be a result of post turnaround refinery pick up gearing up for summer driving season and the delayed restart of the Keystone pipeline. The US summer driving season starts April and peaks in May. So if we want a clear picture of fundamental driven outlook, it will have to wait till about end June, early July which is when mid-June data would come out. In the meantime, the media treatment of crude oil prices would be based on the most vocal explanations, not necessarily the correct ones.

- Will the Doha meeting lead to an extended price rise or the big announcement mean anything? No. You have to look at the fundamentals before you commit to a longer term future outlook. In the short term the Doha meeting will certainly feed price volatility but without a significant change on the demand front (read: China) or supply imbalance (read: drop in production – not output freeze), you can’t commit to a long term positive outlook on oil.

- Why the hell not? The only thing that is certain is that leading up to the Doha meeting and post the event is there will be price volatility. If we had to take a bet it would be prices heading upwards as we lead into the Doha and heading downwards on the day official news breaks and trading positions are cut.

To understand the impact of Doha meeting, you have to understand the context behind the fall in oil prices. The question you have to ask is “Has that context changed?” If the answer is yes, then yes the Doha meeting will change how oil prices behave. If the answer is no, then whatever price changes we see will be driven by perception, not reality. Fundamentals always catch up with air.

The context for oil prices – Q2, Q3 2016

The Supply and Demand mix

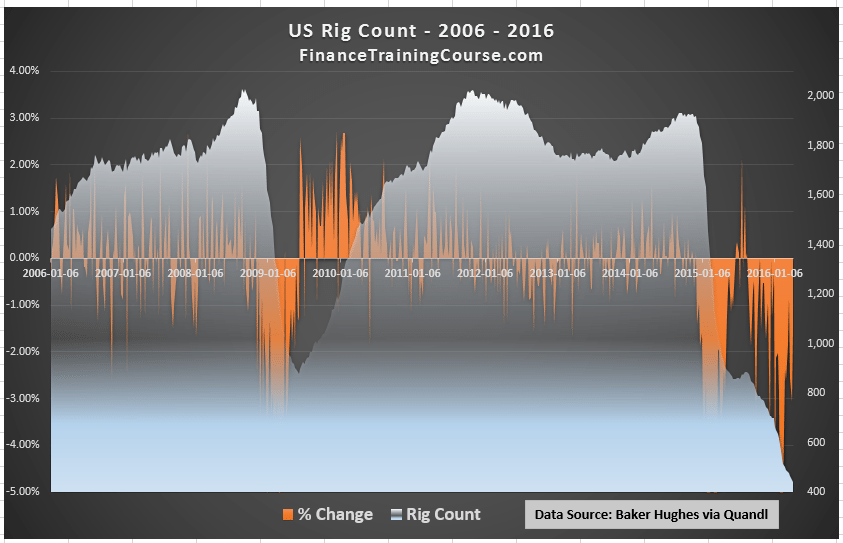

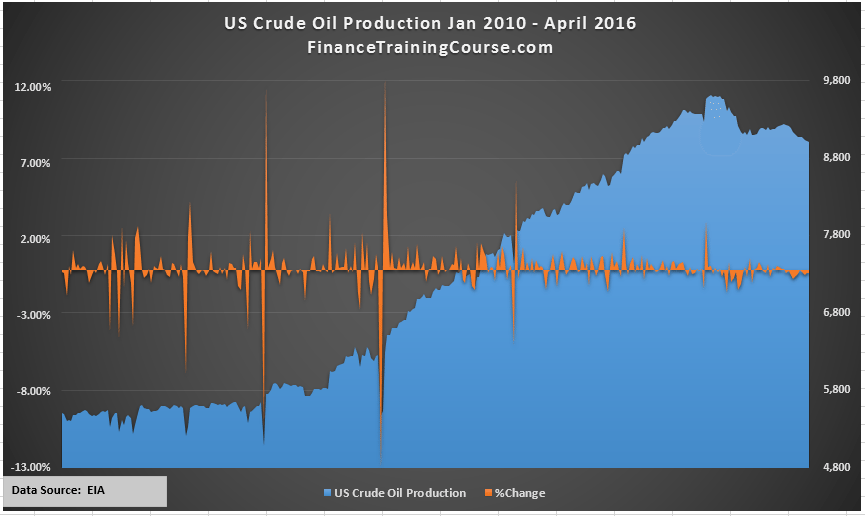

In the background of Doha output freeze talks, the big item in the news was the fall in US production, the surprise fall in crude stocks and the sharp drop in US rig count figures from a year ago. Two of the three items fed into the “Saudi strategy has worked” conversation but what would be the likely impact on prices. Let’s take a look.

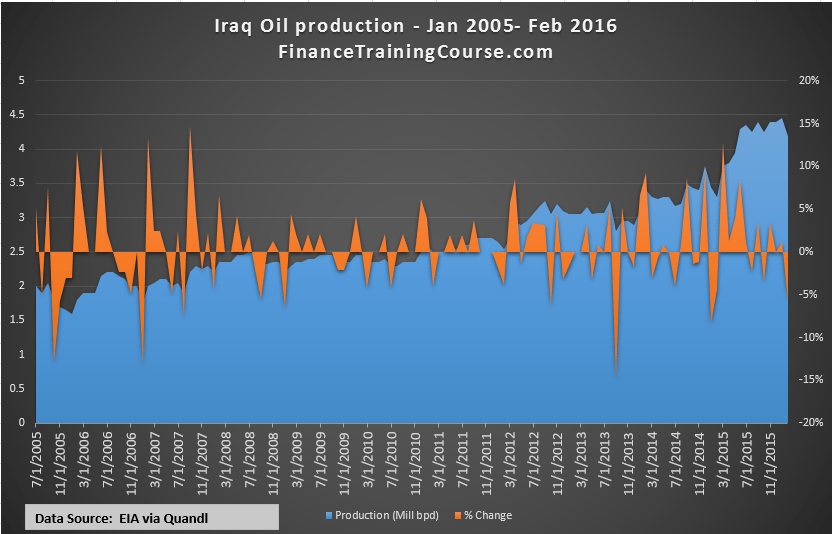

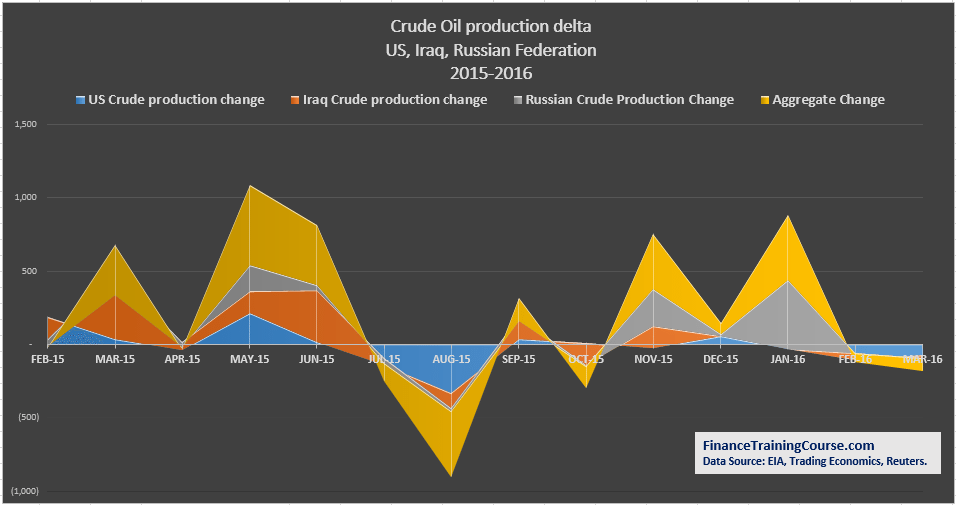

First, production losses in the US have been more than offset by the ramp up in production in Iraq, Iran and Russia.

While US crude oil production has declined by 600,000 bpd, Iraqi oil production has increased by 750,000 bpd, Russian production had added another 900,000 bpd and Iranian claims indicate that they have or will add another 500,000 bpd. In addition to these increases in supply, the Saudi and Kuwait joint production projects kick started in early 2016 will add another 350,000 bpd to the mix.

So while the reduction in US supply is still a welcome news for oil prices, it has not and will most likely not have an impact on the existing supply glut in the local market. Every barrel that goes offline in North American territories is being replaced by two barrels in the Urals, Siberia and the Middle East. While media coverage and recent price action suggest that the US output drop is significant, in the broader context of crude oil production it is not.

The Demand side

On the demand side, there was finally some positive news on the Chinese front as the chances of a run on the Chinese Yuan decreased with an improvement in capital flows as well as an uptick on the manufacturers’ confidence/purchase index. So a plus one on China. We are not out of the woods yet, but it appears that while China may not help with a demand take off in the immediate term, it may no longer take the global economy and oil prices down with it.

The US economy continues to chug upwards and the Federal Reserve meeting minutes and notes didn’t strike any alarming note other than hints on looking at oil and energy prices as part of the systemic risk equation. Indian demand for crude cargoes remained robust. But European numbers sent mixed signals. Two additional plus signs on the US and Indian front and a not so sure on Europe.

The alternate thesis

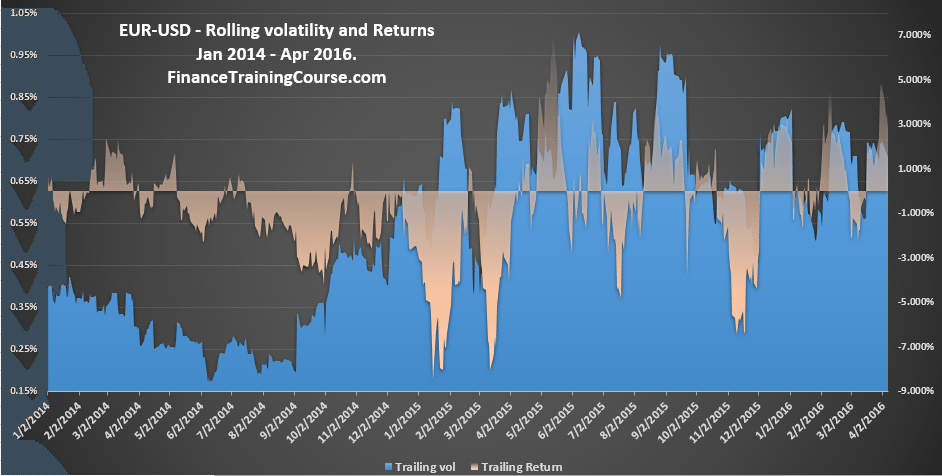

There is an alternate, possibly more credible thesis for the directional change in oil prices than the output freeze talks in Doha. The alternate thesis is the relative price of oil in US dollars. While Iran and Russia may no longer settle their crude export cargoes in USD, the reference price for both Brent and WTI is set in US dollars. Which implies that markets adjust prices due to appreciation or depreciation of the US exchange rate.

While the outlook at the beginning of 2016 was that a policy rate change was imminent recent remarks by the Janet Yellen, the Chairperson of the Federal Reserve indicate that the Fed is likely to go slow. Markets and economic environment need some additional breathing room and the Federal Reserve is in an accommodating mood. 2014 and 2015 were great years for the US dollar on the anticipated rate hike but starting off 2016 USD has given some of those gains back. And that weakness directly translates into crude oil price adjustment.

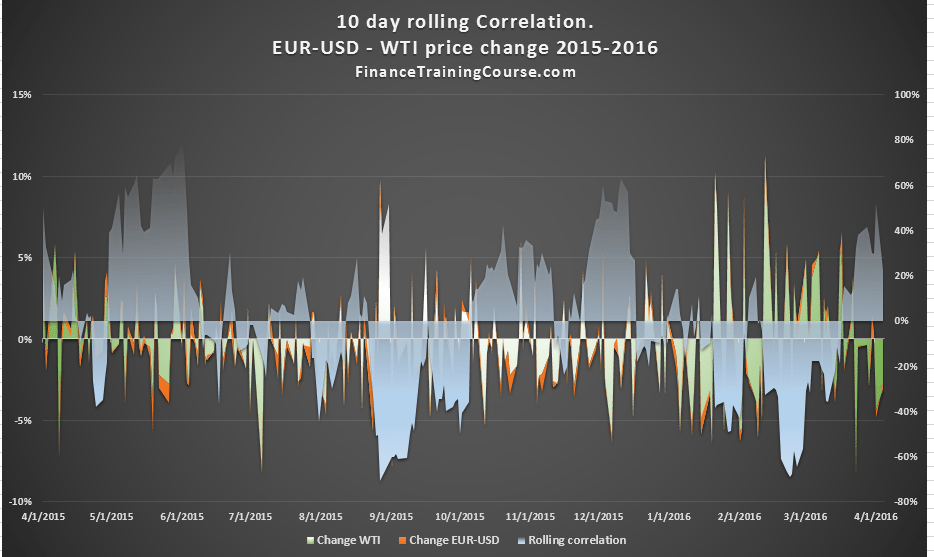

The switch to positive correlation in the late March, early April price change data set support the idea that post the Doha conversation, we may be looking at a correction in oil prices, given the recovery in the US dollar in the days leading into April. While the alternate thesis is significantly more believable than any impact the Doha oil output freeze talks are likely to have, its ability to predict the direction of oil prices still needs to be tested.

Combined with the absence of negative news coming out of China, Fed’s comments, the weakness of the USD, and the lift in refinery consumption of crude cargoes, it appears that the recovery of oil prices has deeper drivers. Atleast for the next few weeks. To see if these drivers have a permanent impact on oil price outlook, we have to wait for June numbers to come in.

In the interim, enjoy the volatility.