Historical FATF Grey List exits

Below is the trend of countries that exited the FATF Grey list after improving their AML/CFT regimes and addressing technical and strategic deficiencies:

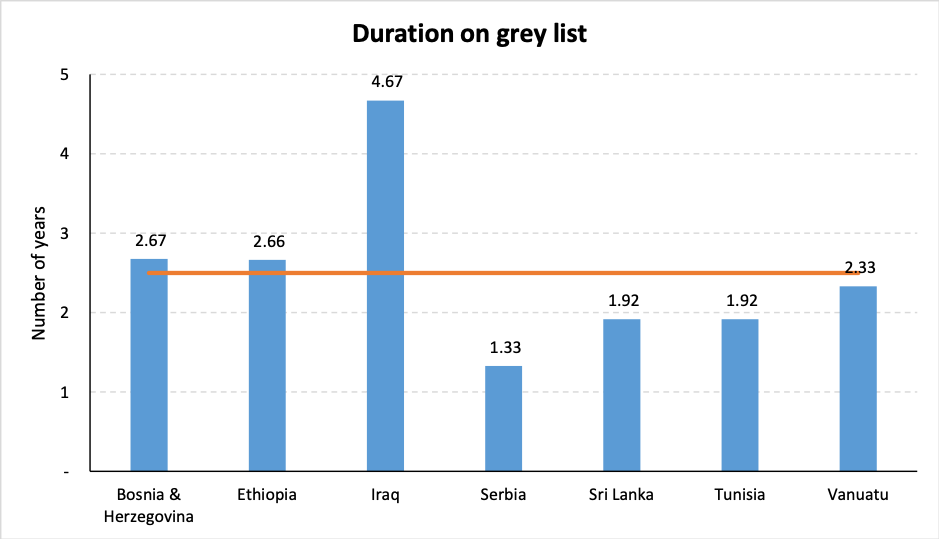

The table below shows when strategic deficiencies were idenitifed for these countries and when they were finally removed from the FATF’s grey list:

| Country | Strategic deficiencies identified in | Exited list in | Duration on list |

| Ethiopia | February 2017 | October 2019 | 2 years 8 months |

| Sri Lanka | November 2017 | October 2019 | 1 year 11 months |

| Tunisia | November 2017 | October 2019 | 1 year 11 months |

| Serbia | February 2018 | June 2019 | 1 year 4 months |

| Iraq | October 2013 | June 2018 | 4 years 8 months |

| Vanuatu | February 2016 | June 2018 | 2 years 4 months |

| Bosnia & Herzegovina | June 2015 | February 2018 | 2 years 8 months |

*Note: No country exited the grey list in October 2018 or February 2019.

In the immediately prior plenary to the one in which these countries exited the grey list, FATF had confirmed that their respective action plans were largely completed. Furthermore, an onsite assessment prior to the next plenary was needed to verify that the implementation of AML/CFT reforms had commenced and was sustainable based on the degree of political commitment.

Even the published statements before the immediately prior plenary set a progressively positive and encouraging tone, indicative of the FATF decision a couple of plenaries down the line.

The average duration that a country has remained on the grey list as witnessed from the past six plenaries is around 2.5 years. However, the duration on the list largely boils down to the commitment demonstrated by the country and how fast it was willing and able to achieve, implement and complete with satisfaction the items on its action plan, showing commitment to a sustainable AML CFT regime that met FATF’s recommendations.

Based on the commentary accompanying the on-going process published statements by FATF on Pakistan for the past several plenaries, the progress made by the country is sufficiently wanting and the tone is decidedly negative.

Hence, it is highly unlikely that Pakistan will exit the grey list in February 2020 given the large number of action items that remain uncompleted. There is no reassuring statement in October 2019’s FATF release stating that Pakistan has completed its action items and is awaiting an on-site confirmation and review visit by FATF.

A June 2020 exit is only likely if:

- Prior to February 2020’s plenary Pakistan manages to complete all action items

- the language from FATF carries a positive tone

- an onsite assessment is planned and scheduled prior to the June 2020 plenary meeting

- and Pakistan has demonstrated the political commitment at the level that FATF is looking for.

One thing though is completely clear. Irrespective of FATF’s final decision and the sequence of actions required to be undertaken before Pakistan gets off the grey list, financial journalists from Pakistan have done a terrible job when it comes to informed and educated reporting on FATF related challenges.

Right from the point before Pakistan got onto the grey list to the point where Pakistan was either getting off the grey list or sliding lower into the even more maligned blacklist, print and financial media reporters from Pakistan and the region have gotten it wrong every single time. By playing to the two extremes without doing a basic cross check on facts, FATF processes, a history of exits and two reviews, they have done a great disservice to readers everywhere. A neutral, factual discourse rather than one based on opinions, biases and hopes would have been appreciated. It would have also made the piece that follows unnecessary.

How does the FATF review process work? How do you get on FATF’s Grey list? How do you get off the FATF Grey List?

FATF technical compliance and effectiveness ratings are determined for all countries. The rating process is conducted keeping in mind the money laundering and terrorism financing risks the country is exposed too, the materiality of each FATF Recommendation for the given circumstances of a particular country, the structural elements that are in place to enable an effective AML/CFT system (e.g. an efficient & independent judiciary), and other contextual factors such as the level of corruption, etc.

The first component of the process is a Technical Compliance. This is an assessment of the compliance of the legal & institutional frameworks and power & procedures of competent authorities of a country’s AML/CFT systems with the requirements of the 2012 FATF Recommendations. Compliance with each Recommendation is assessed at one of four compliance ratings – compliant, largely compliant, partially compliant or non-compliant.

Compliant means that for each of the criteria assessed in a given Recommendation there are no shortcomings. Largely compliant means there are minor deficiencies in some of the criteria. Partially compliant means there are moderate weaknesses, while non-compliant is an indicator of major deficiencies and criteria not being met. If a Recommendation does not apply to a given jurisdiction a rating of not applicable will be given.

The second component of the process is an evaluation of the effectiveness of the implementation of a country’s AML/CFT systems to mitigate the risks of money laundering and terrorism financing. The evaluation is based on the extent that a country’s legal and institutional frameworks have achieved a set of expected Immediate Outcomes. The achievement level of each Immediate Outcome is assessed for effectiveness at one of four levels – high, substantial, moderate level or low signaling the need for minor to moderate to major to fundamental improvements in AML/CFT systems respectively. Assessors will present their recommendations for improvements as part of the Mutual Evaluation Result (MER).

There are eleven Immediate Outcomes (IO) that help achieve three Intermediate Outcomes which in turn lead to fulfilling a High Level Objective. The objective is to have a financial system and economy that is protected from the threats of money laundering and terrorism financing.

The eleven outcomes assessed cover:

- IO.1 – Risk, policy and coordination

- IO.2 – International cooperation

- IO.3 – Supervision

- IO.4 – Preventive measures

- IO.5 – Legal persons and arrangements

- IO.6 – Financial intelligence

- IO.7 – ML investigation and prosecution

- IO.8 – Confiscation

- IO.9 – TF investigation and prosecution

- IO.10 – TF preventive measures and financial sanctions

- IO.11 – PF financial sanctions

A country does poorly on its MER if any of the following are true:

| Technical Compliance Ratings | Effectiveness/ Immediate Outcomes Ratings |

| ≥ 20 Non-compliant or Partially Compliant Ratings | ≥ 9 Low or Moderate Level of Effectiveness, with a minimum of 2 lows |

| ≥ 3 Non-compliant or Partially Compliant Ratings for Recommendations 3, 5, 6, 11, 20 | ≥ 6 Low Level of Effectiveness |

For example, Country A’s MER shows:

- Technical compliance: 15 recommendations have a partially compliant rating, 4 recommendations have a non-compliant rating, while the remaining 21 recommendations (including recommendations 3, 5, 6, 11 & 20) have a largely or fully compliant rating

- Effectiveness: 2 immediate outcomes have a low level of effectiveness rating, 5 have a moderate rating while the remaining 4 IOs have a high level of effectiveness rating

Hence, Country A’s MER would not be termed poor as it does not meet any of the four criteria for a poor result.

On the other hand, Country B’s MER shows:

- Technical compliance: 12 recommendations have a partially compliant rating (including recommendations 3 &5), 4 recommendations have a non-compliant rating (including recommendations 6 &11), while the remaining 24 recommendations have a largely compliant rating

- Effectiveness: 1 immediate outcome has a low level of effectiveness rating, 7 have a moderate rating while the remaining 3 IOs have a high level of effectiveness rating

In this case country B would be assessed a poor MER because it meets the technical compliance rating criteria of “≥ 3 Non-compliant or Partially Compliant Ratings for Recommendations 3, 5, 6, 11, 20”.

A poor result on its MER is one reason why the FATF will continually review and monitor a country on an on-going basis for strategic AML/CFT deficiencies. Other instances when a review will be carried out is when a jurisdiction does not take part in a FATF-style regional body (FSRB) or does not allow the timely publication of the MER; or when the country/ jurisdiction is nominated for review by a FATF member or an FSRB based on specific ML/ TF risks or threats. The review process is overseen by FATF’s International Co-operation Review Group (ICRG).

A country with a poor MER will have a year to work with FATF or FSRB to address the strategic deficiencies identified. FATF will review the progress made and develop action plans for any remaining strategic deficiencies.

The FATF holds plenary meetings three times a year in February, June and October, following which it publishes two statements. Jurisdictions with strategic deficiencies but which show a high level commitment to the action plan developed by FATF is listed in the first statement, the “Improving Global AML/CFT Compliance: On-going process” statement. In FATF shorthand this is the Grey list.

The second statement, “FATF’s Public Statement” (the blacklist) identifies two groups of jurisdictions

- Jurisdictions with serious strategic deficiencies in its AML/CFT systems that FATF calls its members and other jurisdictions to apply counter-measures to protect the international financial system from the ongoing and substantial money laundering and financing of terrorism (ML/FT) risks.

- Jurisdiction with significant strategic deficiencies in its AML/CFT systems that the FATF calls its members and other jurisdictions to apply enhanced due diligence measures proportionate to the risks arising from the jurisdiction.

A jurisdiction may be removed from ongoing FATF monitoring and from the published statements at the next FATF plenary meeting only after it has addressed satisfactorily all elements of its action plan and an on-site visit confirms that this is so. After its removal, it will continue to work with FATF/ FSRB on improving its AML/CFT systems through the normal follow up process.

Timeline

20th February 2018: 37 nation plenary meeting held its first meeting on Pakistan where the country was nominated to be placed on the FATF grey list by USA backed by Britain, France and Germany for having “strategic deficiencies” in “countering financing of terrorism”. China, Turkey and Saudi Arabia (which was representing the Gulf Cooperation Council (GCC)) opposed the move which stalled the nomination.

22nd February 2018: An unprecedented second meeting on Pakistan called by the US, saw Saudi Arabia rescind its opposition to the nomination, after being offered full membership to FATF. This was followed by China opting out of the process to save face, leading to a confirmation from FATF that it would place Pakistan on the grey list in June. Pakistan would need to prepare an action plan on how it would curb terrorism financing and address the strategic deficiencies in its AML/ CFT regimes. The plan was to be submitted to FATF in May 2018 for approval in June 2018. Failure to prepare an action plan or its rejection by FATF could see Pakistan on the blacklist.

29th June 2018: Pakistan was officially placed on the FATF grey list, i.e. a list comprising jurisdictions with strategic AML/ CFT deficiencies. A high level political commitment was made to work with the FATF and its FATF-style regional body, the Asia Pacific Group (APG) to address the weaknesses in its AM/CFT regimes. According to the plan, substantial progress would need to be demonstrated by the country such that:

- Terrorism financing risks posed by terrorist groups were understood

- Remedial actions and sanctions on AML/ CFT compliance violations by financial institutions were implemented

- Competent authorities could identify and take enforcement action against illegal money and value transfer services

- Authorities could identify and curb cash couriers and illicit movement of currency

- There was improved coordination between agencies, including between provincial and federal authorities, to fight TF risks

- Law enforcement agencies (LEAs) could identify, investigate and prosecute persons & entities responsible for TF activity & prosecutions resulted in commensurate prohibitive sanctions and enforcing actions

25th October 2018: APG’s mutual evaluation team visited Islamabad, Pakistan from 8 – 19 October 2018 and conducted a two-week on-site visit for Pakistan’s third round mutual evaluation.

4th January 2019: The Government of Pakistan submitted a Terror Financing Risk Assessment Report to FATF. The report assessed Pakistan’s National Terrorist Financing Risk as ‘medium’.

January 2019: FATF action plan items for January deadlines were not completed.

May 2019: FATF action plan items for May deadlines were not completed.

23rd August 2019: APG members adopted the Mutual Evaluation Report of Pakistan in the 22nd Annual Meeting in Canberra, Australia.

2nd October 2019: APG published its Mutual Evaluation Report 2019 report. The report assessed Pakistan’s progress with respect to compliance with FATF’s 40 technical recommendations and the level of effectiveness of its AML/CFT system. The assessment was of AML/CFT measures in place as of October 2018. Report findings showed that out of the 40 recommendations, Pakistan was fully compliant (C) on 1 recommendation, largely compliant (LC) on 9, partially compliant (PC) on 26, and non-compliant (NC) on 4 recommendations. Effectiveness ratings for 10 of the eleven immediate outcomes were low while one was moderate. Based on the adverse results APG has decided to place Pakistan on its Expedited Enhanced Follow up reporting list.

18th October 2019: Assessed against FATF’s criteria for a poor MER result, Pakistan remains on the October 2019 published grey list and would be subject to on-going monitoring by FATF:

| Criteria | Pakistan’s performance |

| Technical Compliance Ratings | |

| ≥ 20 Non-compliant (NC) or Partially Compliant (PC) Ratings | 26 PC 4 NC |

| ≥ 3 Non-compliant or Partially Compliant Ratings for Recommendations 3, 5, 6, 11, 20 | R3: LC R5: LC R6: PC R11: LC R20: PC |

| Effectiveness/ Immediate Outcomes Ratings | |

| ≥ 9 Low or Moderate Level of Effectiveness, with a minimum of 2 lows | 10 Low 1 Moderate |

| ≥ 6 Low Level of Effectiveness | 10 Low |

Based on the FATF criteria shared above, it should be clear that there is still a great deal of work that needs to be done before we come off the FATF grey list. There is certainly progress being made but as of now, there is a very low chance that we will get off the grey list in June 2020. The biggest challenge remains in the technical compliance score where we need to bring about the most significant change. Within the effectiveness and immediate outcome rating, significant improvements have been made and we are likely to clear the meet the FATF requirements before June 2020’s plenary meeting.

Further, all deadlines for FATF action plan items have expired with Pakistan having met only 5 of the 27 items outlined in the plan. Only partial progress has been made on the other 22 action items. In order to be considered for removal from the on-going monitoring list at the next plenary in February 2020, Pakistan will need to complete all items in the action plan which will need to be verified by FATF in an on-site visit prior to that plenary.

Failure to demonstrate “significant & sustainable progress” in all items of the action plan could result in stricter action by FATF. This would entail issuing a more severe warning to its members, including providing advice to their financial institutions about being cautious when having business relations and transactions with Pakistan (i.e. a possible blacklisting?).

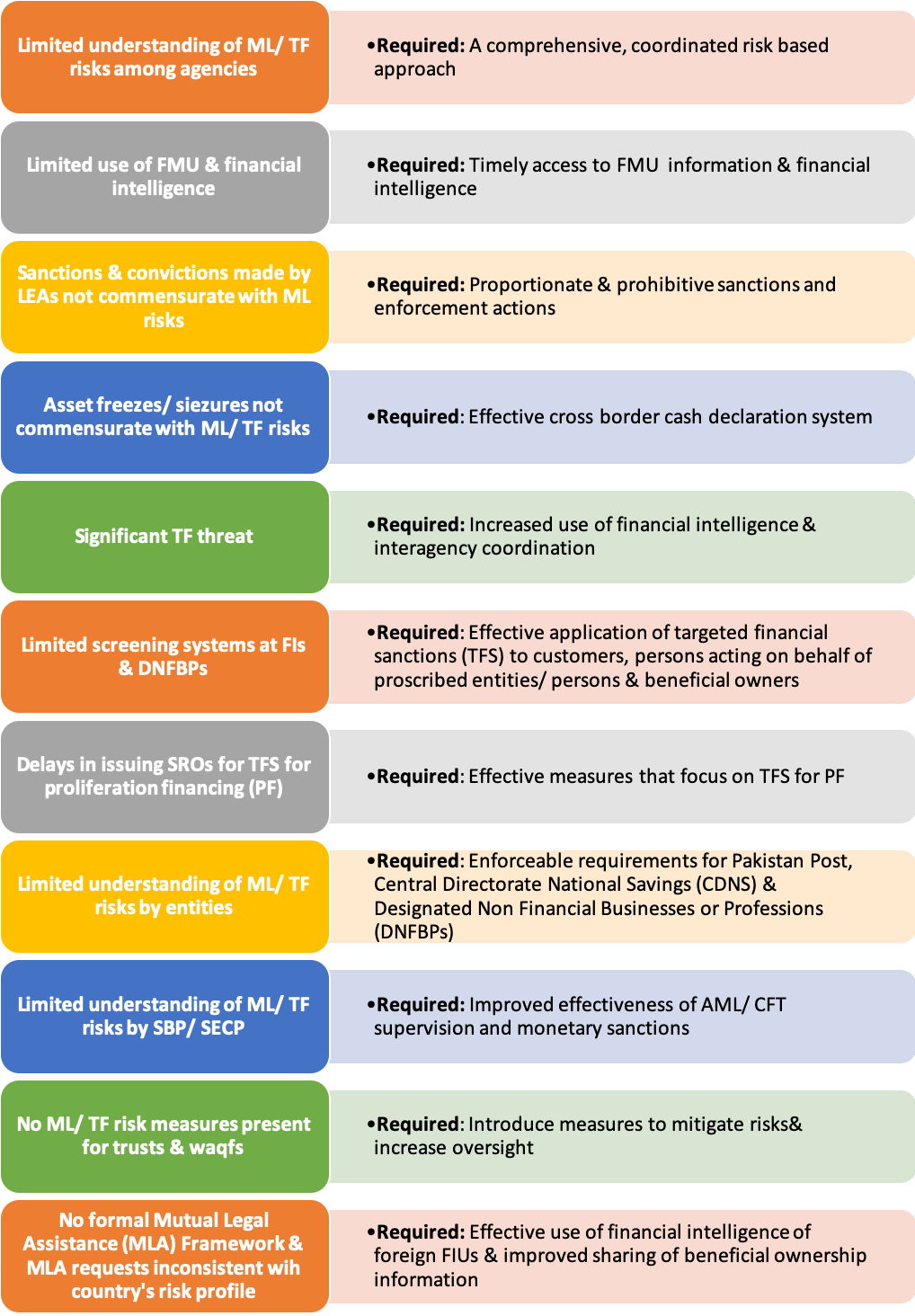

Key findings of Pakistan’s 2019 MER – Deficiencies in AML /CFT measures in place as of APG’s October 2018 on-site visit

Actions taken by Pakistan since February 2018

22nd May 2018: SBP enhanced the KYC standard and documentation requirements for Exchange Companies.

2018:

- AML/CFT Guidelines for Real Estate Agents are circulated through the Federation of Realtors of Pakistan

- All Pakistan Gems Merchants and Jewellers Association (APGMJA) have issued guidelines for their dealers

7th June 2018: SECP issued the Associations with Charitable and Not for Profit Objects Regulations, 2018, in order to strengthen the AML/CFT regime for non-bank financial and corporate entities.

13th June 2018: SECP under recommendation from the Financial Monitoring Unit (FMU) Government of Pakistan issued AML/ CFT regulations 2018 for compliance by regulated persons such as securities brokers, commodities brokers, Insurers, Takaful Operators, NBFCs and Modarabas.

September 2018: SECP issued Guidelines on anti-money laundering, countering financing of terrorism, and proliferation financing for financial institutions falling under its ambit, including Modarabas, Insurers, Non-Bank Financial Companies (NBFCs), etc.

1st October 2018: SECP made some amendments to the SECP AML/ CFT regulations 2018.

2nd October 2018: Financial Monitoring Unit (FMU) Government of Pakistan issued AML/CFT regulations for compliance by Pakistan Post Offices for its Savings Bank and Money Transfer services.

October 2018: Institute of Chartered Accountants issued guidelines for Anti-Money Laundering and Counter Financing of Terrorism for its Accountants.

18th October 2018:

- SBP issued updated AML/CFT Regulations for Banks & DFIs to align existing regulations with FATF Recommendations. The revised regulations aim to provide further clarity on the implementation of AML/CFT requirements by banks/ DFIs, including customer due diligence (CDD), correspondent banking, wire transfers/ funds transfers and minimum documents required for opening accounts by customers.

- SBP issued detailed guidelines for Exchange companies on Targeted Financial Sanctions (TFS) for the prevention of Terrorism Financing and Proliferation Financing under the UNSC Act, 1948 and ATA, 1997.

- SBP required Banks/ DFIs to screen all sponsor shareholders/beneficial owners, directors, presidents and key executives subject to the Fit and Proper Test against the list(s) of designated/proscribed entities and persons. Disqualification would result if they are found designated/proscribed or associated directly or indirectly with designated/proscribed entities/persons under United Nations Security Council Resolution or Anti-Terrorism Act 1997.

November 2018: National Counter Terrorism Authority (NACTA) issued guidelines on actions to be taken by competent authorities for implementation of United Nations Security Council Resolution (UNSCR) no. 1373 by putting into place mechanisms enabling the designation of terrorist organizations and persons associated with terrorism at the national level and the consequent application of immediate sanctions.

11th May 2019: FBR Customs Operations have taken a number of steps to curb money laundering, such as implementing a currency declaration system (linked to the FIA database) at international entry/ exit points, installing baggage/ vehicle scanners at certain border checkpoints, increasing coordination between collector of customs and LEAs, establishing a new Directorate of Cross Border Currency Movement, improving investigations, etc.

August 2019: Ministry of Foreign Affairs, Government of Pakistan issued guidelines for the implementation of UNSCR 1267 concerning targeted financial sanctions (assets freeze), travel ban and arms embargo on designated persons and entities.

14th October 2019: The federal cabinet approved on Monday the establishment of a Real Estate Regulatory Authority (RERA) in the country to regulate that sector and as a consequence restrict the flow of black money in it.

FATF Grey List – The way forward

Pakistan technical compliance list currently includes 26 partially compliant (PC) and 4 non compliant items. This needs to be brought down to under 20 to get a favorable technical compliance review. Pick 6-9 partially compliant items on the list and upgrade them to largely compliant or reduce the list of non compliant items from 4 down to zero or one. This is not a hard ask for a dedicated and committed team and is likely to happen one way or the other by June 2020. Pakistan is likely to focus on the partially non compliant items and build upon existing momentum rather than start from scratch on the non-compliant items.

The bigger challenge, however, is the effectiveness and immediate outcome rating where we stand with 10 lows. We need to bring down this number down to 2. While enforcement and effective regulation have been largely successful in the formal sector and fairly successful in the formal financial sector, there is a lot of work that needs to be done in the informal sector. Prosecution and conviction also remain a challenge.

While the two financial regulators, SBP and SECP have built capacity as institutions over the last two decades, Law Enforcement Agencies (LEA) and Judiciary have lagged significantly behind. Despite their challenges both SBP and SECP enjoy a significant amount of trust and respect from regulated entities and businesses. This is not necessarily true for the other two pillars, especially at grass root levels. This is a hard ask and the area where Pakistan’s biggest challenge lies. To this challenge add an attempt for the first time to regulate and document Designated Non Financial Business Professionals (DNFBPs) – Lawyers, Jewellers, Real Estate Agents among others.

A focused approach on outcomes under the control of SBP and SECP is the way to go. But the success of that effort would be determined by how quickly and how far LEA and Judicial branches of the government move. Our prosecution and conviction record for financial and non-financial crimes with financial impact has to improve.

This new push will raise the burden of compliance on the regulator and the regulated, as well as the cost of doing business in Pakistan. But it can’t be helped. For Pakistan to continue to be part of the international economy, this is the price that we all have to pay.

FATF related transformation within Pakistan’s formal and informal financial sector once complete will feed a dream many national reformists have had about Pakistan’s economy. For five decades we have dreamed of better documentation and disclosure. Side by side with internal reforms at the Federal Board of Revenue (FBR), in the long run, FATF driven initiatives, will push tax revenues higher.

They will also place an additional burden of responsibility on institutions and professionals associated with the financial sector and lead to significantly higher fees for governance and compliance professionals. Unlike earlier initiatives, this time the impetus for change comes from external sources and a threat of effective isolation from trade, investment and remittance flows. Compared to reforms linked to historical aid packages, this one is linked to sanctions and penalties.

Perception management and media reporting around FATF has also been a big fail. This needs to improve significantly. Rather than sugar coating how bad a job was done in the recent past, it is important to own mistakes, acknowledge challenges ahead and set realistic expectations. A narrative divorced from reality before and after plenary sessions and controlled by our national ego showcases us as naive, uninformed, incompetent and unaware of how the process works at FATF. We can certainly do better.

Sources and References

- “Pakistan may find itself on FATF blacklist after June” – Dawn – February 26, 2018

- Pakistan Mutual Evaluation Visit – 25 October 2018 – APGML.ORG

- “Pakistan sends Terror Financing Risk Assessment Report to FATF today” – The News – January 4, 2019

- 22ND APG ANNUAL MEETING, CANBERRA, AUSTRALIA – 23 August 2019 – APGML.ORG

- Anti-money laundering and counter-terrorist financing measures – Pakistan Mutual Evaluation Report – October 2019 – APGML.ORG

- Improving Global AML/CFT Compliance: On-going Process – 23 February 2018 – FATF

- Improving Global AML/CFT Compliance: On-going Process – 29 June 2018 – FATF

- Improving Global AML/CFT Compliance: On-going Process – 19 October 2018 – FATF

- Improving Global AML/CFT Compliance: On-going Process – 22 February 2019 – FATF

- Improving Global AML/CFT Compliance: On-going Process – 21 June 2019 – FATF

- Improving Global AML/CFT Compliance: On-going Process – 18 October 2019 – FATF

- Box 4: FATF and AML/CTF regime in Pakistan – State Bank of Pakistan

- Implementation of the UNSCRs concerning Targeted Financial Sanctions, Travel Ban and Arms Embargo – Ministry of Foreign Affairs, Government of Pakistan

- Government to form new authority to regulate real estate sector – Samaa.TV – October 14, 2019

- Effective Steps Taken By FBR Customs Operations to Curb Money Laundering – FBR

- Guidelines on actions to be taken by competent authorities for implementation of united nations security council resolution no. 1373 – NACTA

- Anti-Money Laundering and Counter Financing of Terrorism A Guide for Accountants – ICAP – October 2018

- All Pakistan Gems Merchants and Jewellers Association AML & CFT Guidelines, 2018

- High risk and other monitored jurisdictions – review process – FATF

- FATF issues new Mechanism to Strengthen Money Laundering and Terrorist Financing Compliance – FATF

- Guidelines on SECP’s anti-money laundering and countering financing of terrorism) regulations 2018 – SECP – September 2018

- Associations with Charitable and Not for Profit Objects Regulations, 2018 – SECP – June 2018

- AML/ CFT regulations 2018 – SECP – June 2018