Duration and Convexity for US Treasuries

4 mins read To demonstrate how to calculate Duration and Convexity for specific US Treasuries we select instruments from recent US Treasury bill,

4 mins read To demonstrate how to calculate Duration and Convexity for specific US Treasuries we select instruments from recent US Treasury bill,

3 mins read Risk Models, Option Pricing & Bank Regulation training for practitioners A typical MBA program allows a candidate to take a

5 mins read ALM Banking models – Assumptions review In a recent class on Asset Liability Management Models, my MBA students asked a

2 mins read Treasury Option pricing & Risk lessons directory Over the last few years we have posted some interesting training materials cutting across

4 mins read Here is an abbreviated partial solved solution to the practice exam question posed earlier. The practice exam question was used

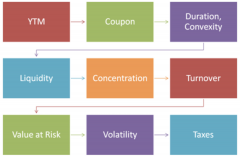

7 mins read In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration,