Risk Models, Option Pricing & Bank Regulation training for practitioners

A typical MBA program allows a candidate to take a maximum of two Derivative pricing courses. Most candidates do a review of basic products in their core courses followed by a specialized course focused on product market, applications or pricing, but not all three. These leaves a big gap that needs to be filled if you are interviewing for a Sales & Trading role or if you are (un)fortunate enough to get assigned to that desk.

For undergraduate students the picture is even bleaker. There is little room in the course work to take an advance derivative pricing course before graduation and both banking and sales and trading desks hire heavily for their analyst programs.

a) Understanding derivative pricing and modeling at a sales and trading desk requires expertise from multiple fields. A successful pricing and modeling resource needs to balance modeling, practice and intuition in equal measures.

b) Theory is easy, intuition is difficult. Passing an exam or getting a degree is no assurance for competence. Intuition can only be learned with experience or practice. Experience comes from trading and trades, especially trades on which you are on the losing side.

c) If you run a Sales and Trading desk you are generally limited to people who have worked on the desk and understand trading discipline and intuition. How do you show the ropes or teach someone who has the right pedigree and the right attitude but is missing the experience?

There is really no solution to the above challenge. Which is the reason why most money managers and Sales & Trading teams dislike hiring fresh talent. It is also the reason why Sales and Trading jobs are the most difficult to break into and also come with the highest gross annual compensation figures.

But derivative pricing and modeling is not just a challenge for fresh intake and candidates for the Sales and Trading desk. Imagine being a board member or senior executive who suddenly finds himself responsible for derivative exposure that he or she doesn’t understand. Put yourself in the shoes of an accounting partner required to issue a fair value statement for a portfolio he doesn’t get. Where do you get relevant training material written in a language that you do understand – a language that is not completely made of partial differential equations and Greek symbols.

Textbooks are either too simple and superficial or too mathematical and difficult. When they are able to strike a balance they tend to be too academic or esoteric. What is needed is a training guide that allows readers to develop intuition by following practical exercises that build up foundations for more difficult materials. A guide that doesn’t stop with exercises but helps explore trading, pricing and risk themes. Sort of like a build yourself a chemical rocket in your backyard kit. Except that you are building pricing models and MS Excel becomes your backyard.

Risk Models & Bank Regulation Training Courses

Our most popular risk models and bank regulation training materials from the first six weeks of 2013. Topics include:

- Risk & Risk Management

- Value at Risk

- Asset Liability Management

- Monte Carlo Simulation & Option Pricing

- Option Greeks & Delta Hedging

Risk & Risk Management

A short and sweet introduction to risk, risk management and risk exposures. Written and shared by a request from a regulatory client for a basic note on risk management

Bank Regulation

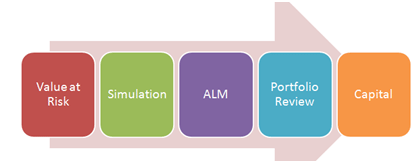

From Value at Risk & Asset Liability Management to Capital Adequacy Ratios we take a look at metrics, models and Excel spreadsheets. While there is enough here for a short course on all three themes, we also speak about what bank regulation fails in emerging markets because of an unfortunate focus on Capital Adequacy Ratios. Materials sources from the Risk Management and Advance Risk Management courses we run in Dubai and Singapore.

Value at Risk – Methods & Metrics

Why does bank regulation fail?

Calculating Conditional Value at Risk

Asset Liability Management – Assumptions, Convention, Tweaks & Hacks

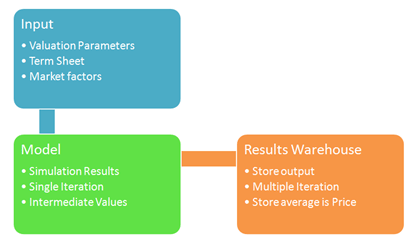

Option Pricing using Monte Carlo simulation

Using Monte Carlo Simulation, Binomial Trees and Black Scholes equation to vanilla and exotic options. If you were looking for a single & comprehensive resource for Monte Carlo Simulation and Option pricing, you have found it. Based on the Derivative pricing course we teach at the SP Jain campus in Dubai and Singapore.

Monte Carlo – How to reference

Pricing Exotic Options using Monte Carlo Simulation

Advance Topics – Greeks, Optimization, Delta Hedging

The War on (Option) Greeks post collection and the Advance Risk Management workshop resource page.

War on Greeks – The weekend challenge

Advance Risk Management Workshop – Dubai & Singapore Campus