Master Credit Analysis course

Business need cash to function and grow. However the nature of business creates timing mismatch between cash coming in and cash going out. A timing mismatch occurs because there is a lag between the time it takes us to produce a product, sell it and collect the payment. The manufacturing cycle leads into the inventory cycle which feeds the sales cycle which feeds the collection cycle. Raw materials and production process convert into finished goods and inventory, inventory converts into sales, sales convert into account receivables convert into cash.

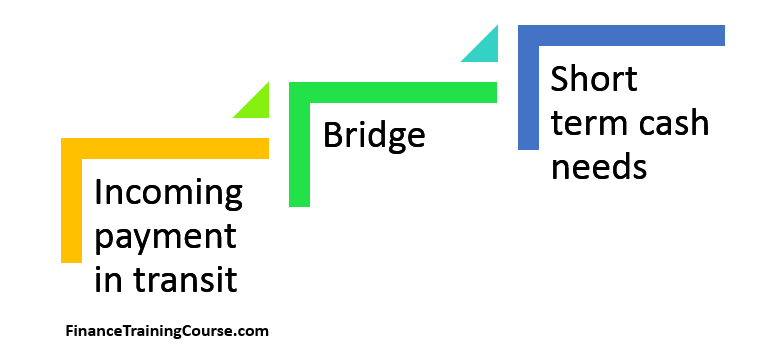

While our capital as owners is tied into non liquid assets required to run the business (Plant and Machinery, Other Fixed Assets and goodwill) bank credit serves as a much needed bridge between incoming payments and short term cash needs. It provides us the cash we need to buy raw material, pay bills and salaries and produce and manufacture products as well as finance our ability to carry inventory of finished goods.

This relationship is the basis of credit analysis. When we cut down to the bone what really matters is the ability of both the customer and the relationship manager to understand that credit is just a temporary bridge and that respect for that temporary nature will determine how far a credit relationship will travel.

Business and collection cycles are influenced by economic cycles. Regional and national economies grow and shrink based on a number of factors. Commodity driven economies do well when raw material prices rise on account of demand and global growth. They shrink when demand slows down and prices tumble. A growing economic cycle feeds growth, margin and liquidity and makes it possible for businesses to invest for the future. Growth in turns creates a requirement for short term cash that can be used to bridge temporary shortfall. A shrinking economic cycle feeds caution and if identified in time leads to cash conservation. Cash conservation focuses on reducing inventory, head count and discretionary expenses.

If we could predict cycles we would start investing and consuming cash when the growth cycle begins to take advantage of new demand. Conversely when we see indicators of a coming slow down we focus on conserving cash and converting as much of our assets into cash as possible. If in a growing economy our conversion cycle runs for 60 days and our collection cycle for another 90 days with the arrival of recession we cut both down as much as possible. In growth mode we carry inventory that may support 40 days of sales, with recession, we shrink it down to less than half.

Credit Analysis – Core questions.

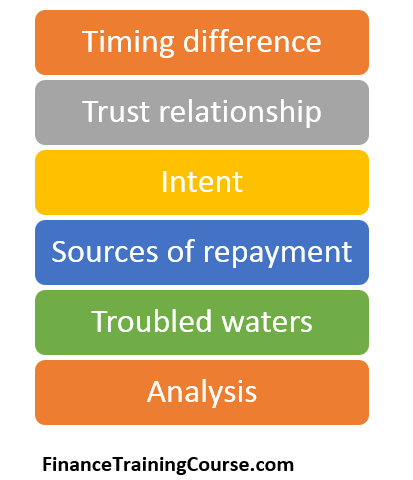

Credit analysis therefore focuses on a few key questions.

The first is the timing difference. If a shortfall occurs, what is the nature and timeline for the shortfall? What drives it? Do we understands factors that can change the timing and magnitude of the shortfall? What portion of the shortfall will be addressed by the amount being borrowed? What will be the source of repayment? Would it be the incoming payment? What proportion of the credit exposure is covered by the incoming payment? Do we have any prior signals on this relationship that give us a clear indication about the intent of the client and the transaction? Prior history with us or with other banks in the region? What happens if the primary source of repayment doesn’t materialize? Is there a backup? What asset or commitment pledged by the borrower would secure the exposure? How easy would it be for us to collect, claim and liquidate the security if this transaction runs into difficulty?

Credit analysis aims to answer all of the above questions and then test the answers for both a growing economic cycle as well as for an economy in recession. The template or format for this analysis is the credit proposal (CP) also known as the credit memo (CM) or the application for credit limit (AFL)and while the template and format may differ, it presents answers to the above questions in a summarized form.

The credit analysis course.

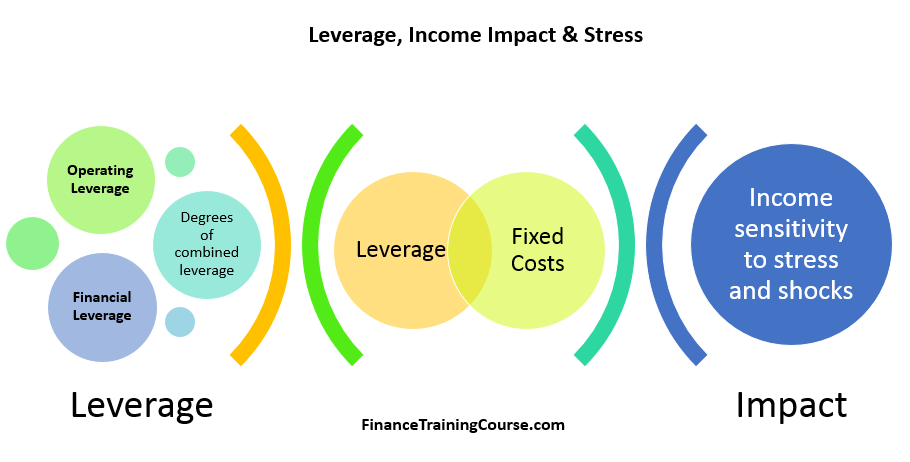

Our credit analysis course begins with a focus on leverage and business. While we will discuss the credit analysis process and ratio analysis separately, an understanding of the impact of leverage is key to decoding how a given business will perform under times of stress. We want students to understand how leverage impacts a business before they begin to prescribe it as financial advisers and engineers.

We look at two different instances of leverage – one financial, one operational and use that to calculate degrees of combined leverage. Degrees of combined leverage or DCL is an interesting concept that allows you to measure the impact on earnings for every dollar increase/decrease in sales on account of the combined leverage of a firm.

- Leverage: A first look.

- Credit Analysis: Break even and leverage

- Credit Analysis: Fixed Costs and Operating leverage

- Credit Analysis: Understanding Financial Leverage

Credit Process and the Credit Proposal

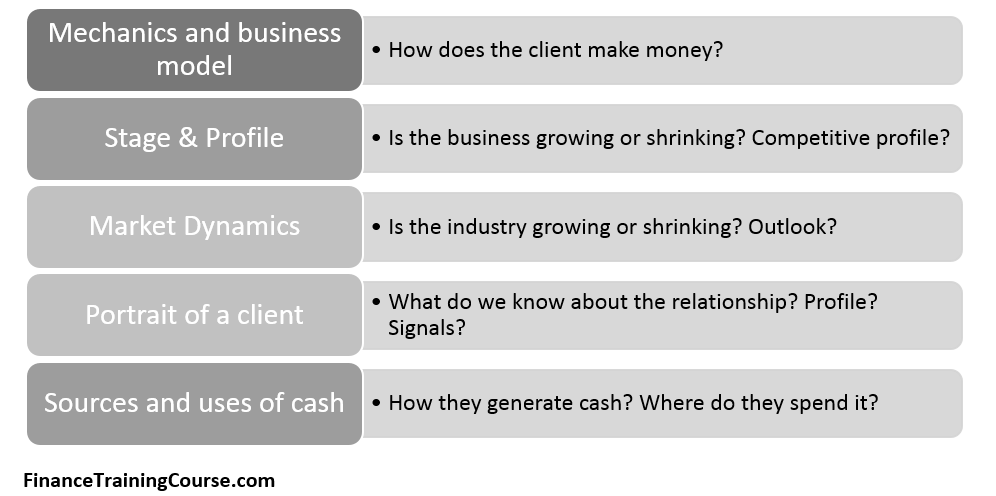

The credit proposal also paints a portrait of the client with broad brush strokes. This includes a review of the business and the business model including its current stage – growth, maturity or decline. A review of the industry outlook to give an indication of external pressures on the business in future years as well as at the time of repayment. The profile of the client include market repute, history and existing credit relationships. Finally a detailed and in-depth analysis of the ability of the business to generate cash and how that cash has been used in the past. To invest and grow? Or paid out to the owners and shareholders?

While we started the discussion with financial and operating leverage and the mindset behind the borrowing decision, the second part of our course focuses on the lending side of the equation. Let’s take a quick look at the credit process.

- Credit Process: Mindset

- Credit Process: Why do businesses borrow money?

- Credit Process: Lending products?

- Credit Process: Review

- Credit Process. The role of the loan officer / relationship manager

- Credit Process: Credit Culture and Information Gathering Foundations

- Credit Proposals and Credit memo: information gathering and processing

- Baldwin Piano – Industry and Non Financial analysis case

- Finance Case: Ratio Analysis: ODP and Staples

- Credit Process: The Credit Decision

- Credit memo presentation to the credit committee. Tips for loan officers

- The credit decision. Factors.

- Analyzing Cash flow Statements: Examples

- Credit Process: Understanding the language – I

- Credit Process: Understanding the language – II