Understanding Option Greeks – Introducing Gamma

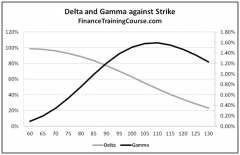

3 mins read Understanding Option Greeks – Introducing Gamma Gamma is the second derivative of the option price with respect to the price

3 mins read Understanding Option Greeks – Introducing Gamma Gamma is the second derivative of the option price with respect to the price

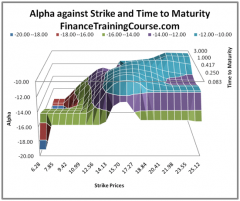

2 mins read N. N. Taleb explains Alpha or the Gamma Rent, in his book Dynamic Hedging, as ‘Theta per Gamma ratio’. At

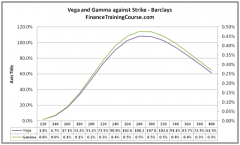

3 mins read 1. What is Vega? Vega is the change in the value of the option with respect to change in volatility.

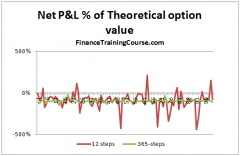

3 mins read A simple case study Theoretically speaking in the Black Scholes world the cost of the hedge should be close to

6 mins read We use a simple example to illustrate the calculation of Shadow Gamma as describe by Taleb in Dynamic Hedging. Gamma

2 mins read We build a simple Excel spreadsheet that allows us to hedge Gamma and Vega exposure for a single short position