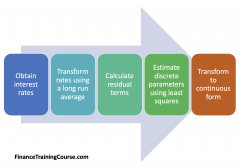

CIR Model Parameter Estimation

2 mins read In this post, we explore CIR Model parameter estimation. In other words, we consider how to calibrate the Cox Ingersoll

2 mins read In this post, we explore CIR Model parameter estimation. In other words, we consider how to calibrate the Cox Ingersoll

2 mins read We review the one-factor equilibrium Cox Ingersoll Ross (CIR) model and its primary features. The short-term interest rate is one of the

< 1 min read 9 commonsense Rules for implementing Value at Risk Earlier today, I wrote about the Jorian-Taleb debate on the relative

5 mins read One of the most common question I face as a consultant deals with how do you actually implement Value at Risk. Here implementation is used more along the lines of interpretation of value at risk rather than physical implementation. Clients understand that systems need to be purchased, controls need to be created, data needs to be gathered but once every thing is in place and you are getting your 2,500 risk reports every day, what do you do next. How do you actually read the VaR reports and how do you link it to controls

2 mins read This formula reference includes the following formula, sections and terms related to calculating Value at Risk

3 mins read Qualifications to using and Limitations of the Value at Risk (VaR) Metric VaR is dependent on historical data and therefore