GEMS Education School System and its tango with institutional private equity investors, financial markets and banks in the region makes for a fascinating read. As an investor if you have been following the K-12 and high school education segment in Middle East, it is impossible to not come across GEMS Education. GEMS has run the course with three rounds of private equity investments (2007, 2013, 2019) two public debt issues (US$200 million and US$900 million) and multiple bank refinancing and credit extensions.

In its most recent round, CVC Capital Partners paid US$1 billion to acquire a 30% stake in GEMS Education, valuing the enterprise at US$4 billion. Considering GEMS was planning to go public at a slightly higher valuation a year ago, the CVC’s deal seems to be fairly valued. Is it? That is the question we want to ask and answer here. Did CVC overpay for GEMS or did they manage to get a discounted deal in at the aftermath of GEMS cancellation of its IPO?

Data for GEMS private equity case study was sourced from publicly available information. GEMS financial statements till half year 2018 were sourced from investor relations. Prospectus and investor memorandum for GEMS earlier publicly listed debt issues are available online. Investor and institutional press releases filled in remaining gaps. Other items such as outlook for 2019, 2020 and 2021 were generated by extrapolating historical trends and proforma financial statements.

GEMS Education – An introduction

Started six decades ago in 1968 with a small school in Dubai, United Arab Emirates, GEMS Education today operates the largest school system in Middle East. As of August 2018, GEMS operated 48 schools with 119,000 students and projected annual revenues of US$ 1.01 billion. GEMS’ recent growth was fueled by bank financed borrowing and strategic private equity investments over a thirteen-year run beginning 2006.

By August 2018, GEMS had borrowed US$ 1.25 billion dollars across multiple facilities secured by US$ 1.3 billion in assets. Growth in primary school market was slowing, expansion focused joint ventures in North America had ended on a bitter note yet Saudi, Egyptian and European markets were looking to be promising.

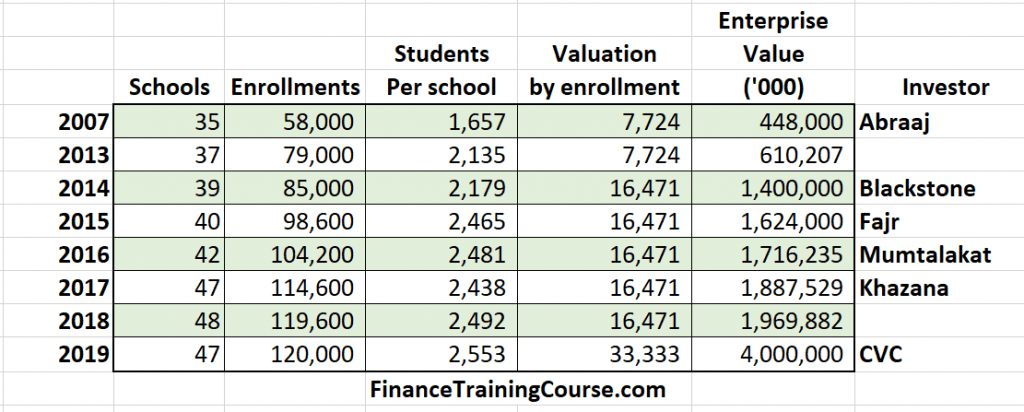

In 2007 when GEM closed its first private equity round with Abraaj, it was already a significant player in school education in Dubai. With 35 schools and 58,000 students, future growth trajectory with Abraaj’s backing projected a tenfold increase in schools and students to 350 schools and 500,000 students. A US$ 112 million stake for 25% valued the enterprise at US$ 448 million.

GEMS story dove tailed with Dubai’s transformation as a regional banking, finance and trading hub. Dubai outlook in 2006-7 called for doubling expat population over 5 years. GEMS planned to ride that wave and expand in the region opening markets in Saudi Arabia, Europe and North America with its newly raised capital treasure chest. Education was a safe demographic play that also hedged against future slow downs because irrespective of how bad things were, kids still had to go to school. Education was the last expense expat or south Asian parents would cut.

The 350 school, 500,000 student plan died with the 2008 financial crisis and the ensuing real estate downturn in Middle East. To its credit in the years that followed GEMS still managed to double its student body and increase geographic exposure to other markets. Growth was not painless and included wrong turns, challenges and hairy moments. The latest of which was a freeze on school fees by Dubai education authorities in 2018 which put a hold to GEMS plans to go public at US$4.5 to US$5 billion valuation.

Faced with new question marks, GEMS extended credit lines, borrowed an additional US$400 million from bankers and went back to the drawing board to find a new deal to facilitate Blackstone, Mumtalakat and Fajr Capital’s planned exit as investors.

GEMS School System Timeline – 2007 to 2019

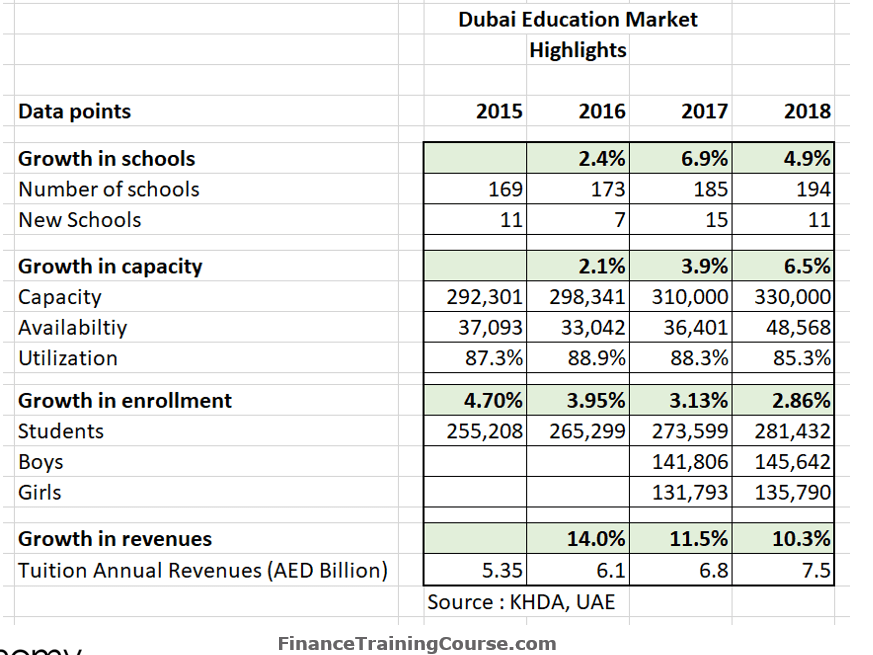

Dubai’s education Market

As per KHDA, Dubai’s school education system in 2018 had 281,000 enrolled students and a capacity to serve 330,000. Annualized school tuition revenues in August 2018 were AED 7.5 billion (US$ 2.04 billion) growing at 10% annually.

While significant investment in new capacity had been made, utilization had begun to fall in recent years as the economy softened. Growth rates in enrollment and new capacity have both slowed. GEMS represents the largest single school system operator within this network. As enrollment and annual tuition revenue growth falters, GEMS with its significant debt burden and limited free cash flows, stands at risk when the expected slowdown arrives and persists.

Economic outlook for 2019 is not encouraging. While Expo 2020 is expected to provide much needed lift, the region has suffered from shortfall of liquidity due to sinking oil prices, regional conflicts, tensions and trade sanctions.

UAE economy has been under pressure because of real estate supply overhang with no signs of immediate relief in coming years. Trade is also unlikely to jump back to pre-crisis levels. Beyond GCC, global economic outlook is also in trouble. Warning signs coming out of Chinese, Indian and Eurozone economies are a cause of additional concern. Souq.com and Careem’s multi-billion exits have provided short term cheer and hope for the technology sector, the size is too small relative to other segments of economy. The outlook has also depressed valuation multiples for UAE domiciled businesses.

With this background a story centered around growth in education is unlikely to sell. The one upside is expansion outside of UAE, especially in other regional markets in Middle East. GEMS has already been at work on that. There are indications of exploring European markets but given GEMS experience with its US JV a few years ago, opinions on the success of that particular stream are divided.

To lend or not to lend?

As one of the lenders invited to the GEMS debt refinancing conversation you have a difficult ask in front of you. Should you lend to GEMS Education and become part of the consortium that underwrites the new debt facilities or not?

GEMS has a documented historical tendency to refinance every few years when rates favor the transaction so any potential upside or benefits from a long term relationship with the school system is likely to be limited. On the downside front, in addition to the US$ 1.25 billion in debt GEMS is also burdened by US$ 1.6 billion in operating leases and a slowing market.

Questioning Private Equity valuation.

As a private equity investor, GEMS track record in creating value and ensuring profitable and credible exits for its investors is quite respectable. GEMS finance team has been able to borrow in most difficult of times from institutional lenders as well as public markets on a consistent basis. Its most recent US$ 900 million sukuk is a prime example. Proceeds from the sukuk will most likely be used to pay down bank debt and lock down rates at 7.125% for the next 7 years reducing the risk of a rising yield curve.

In its twelve-year history with private equity investors GEMS has successfully stepped up its enterprise valuation 8 fold. Starting off with a cheap US$448 million enterprise value via Abraaj in 2007, GEMS most recent investment round via CVC values the enterprise at US$4 billion in 2019.

Remarkably GEMS has been able to do this by increasing the number of schools from 35 to 47. Not the 350 planned originally with Abraaj. Increasing enrollments in existing schools, rising tuition fees and mature school properties have made it possible for GEMS to move valuation metrics in its favor.

In 2007 Enterprise value divided by enrolled students, valued a GEMS student life time value at US$ 7.7 thousand. In 2019, the same figure stood at US$ 33.3 thousand per student.

Between 2007 and 2019 a few things changed. According to the Abraaj transaction review GEMS added an additional 22% of revenue by 2010 in non-tuition revenues by consolidating teacher training, student activities, transportation and assessment services. This did not exist in 2007. School fees went up. According to KHDA the average annual tuition fees paid across Dubai schools in 2018, stood at US$ 7.3 thousand per student. In 2012 the figure stood at US$ 4.7 thousand per student. In 2018 GEMS valuation metrics projected 4.6 years of student years with its school system. In 2012 the same figure was 1.65 years.

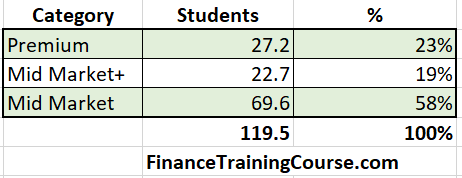

GEMS classified 42% student enrollments in Mid Market+ and higher schools more or less in alignment with KHDA estimates. But Premium and Mid Market schools had that highest capacity utilization while the Mid Market+ category had softer figures.

So where is the disconnect?

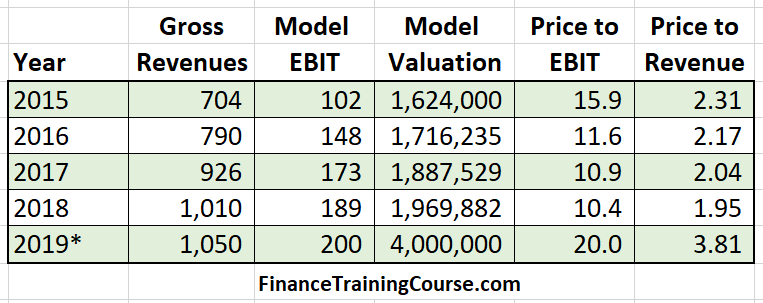

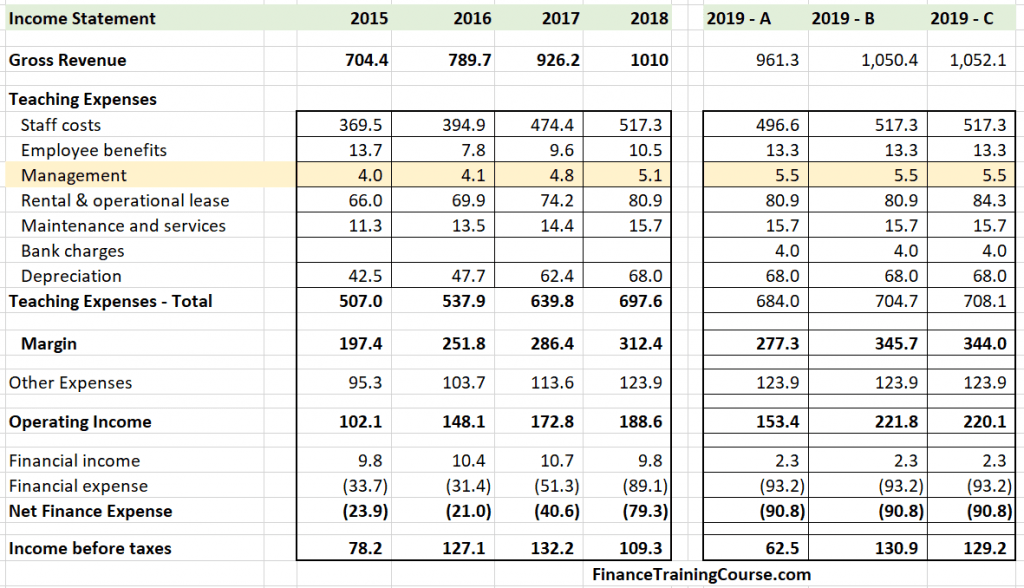

In the table above GEMS’s 2019 gross revenue and EBIT figures are best case estimates. 2019 was a difficult year for everyone in Dubai. Burdened with frozen tuition fees and a failed IPO, GEMS actual numbers are likely to be lower. Using both Price to EBIT and Price to Revenues as a valuation metric we see a steep step up for the CVC GEMS transaction. There is nothing in the context, in the environment or the outlook to justify that step up.

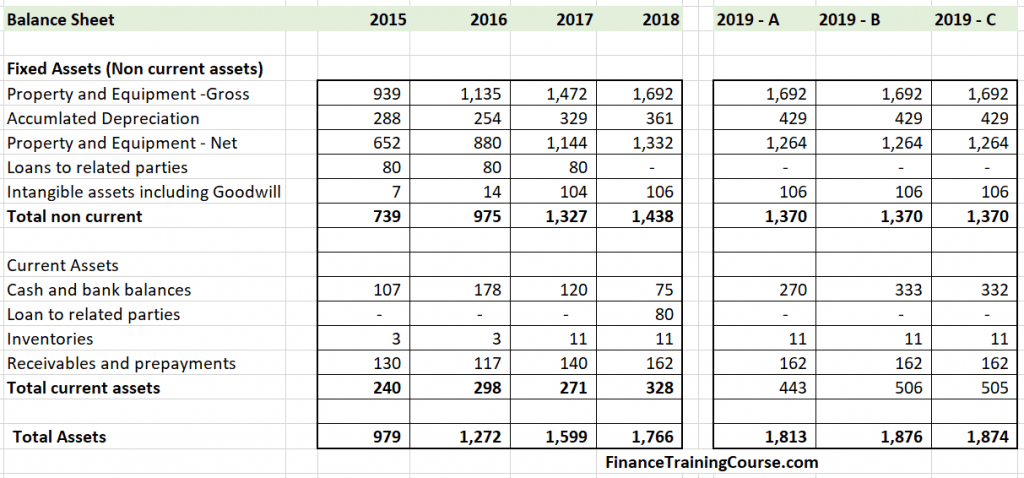

Beyond valuation multiples, the other challenge is that the step-up is not backed by a similar ten-fold increase in GEMS’ book value. The biggest item on GEMS balance sheet is land, property and equipment. Over the last decade value of commercial and mixed use real estate in Dubai has plunged on account of over supply.

Average tuition fees have gone up in twelve years, they haven’t gone up ten fold and the rate of growth in fees is slowing down, while expenses continue to grow at a faster clip. The same is true for growth rate in capacity and enrollments.

Did Abraaj and Blackstone beat their IRR on GEMS?

Given public numbers shared by Abraaj, Abraaj didn’t appear to have made its planned or projected IRR on GEMS. We don’t have exact details but we can make educated guesses based on publicly available data.

Abraaj got their money back and over a six year investment horizon and earned a dollar denominated return between 11% – 13% on their GEMS investment. Blackstone and Fajr were luckier and booked 19% – 21% over their four and a half year association with GEMS. Will CVC be able to break or go beyond this benchmark is the question?

Blackstone’s return is more attractive because rates were higher when Abraaj raised their fund in 2006 compared to Blackstone and Fajr in 2012. So the step up may just be a function of private equity IRR rather than real world value creation.

Part of GEMS charm is Dubai and the central role GEMS plays in the education sector in that city. Lenders and investors believe that the school system has grown to be one of the few Too-Big-To-Fail (TBTF) enterprises in Middle East and will always be able to tap lenders and financial market. On the finance side the organization runs a tight ship and other than its tendency to favor investors over lenders and take full advantage of favorable terms and conditions, it is ranked as one of the more credible and professional borrowers on the lending circuit.

Modeling GEMS Education

The questions you want to ask as a lender on the GEMS transaction are:

- How much cash does GEMS generate annually? Is that enough to cover its debt servicing load?

- How is that cash used? How has GEMS used excess cash flows historically?

- How does Dubai’s current economic outlook impact these numbers?

- Will GEMS be able to pay its committed principal repayments? If cash flow from operations is not enough what other alternate sources exist for repayment?

- How do GEMS debt service coverage ratios change with changes in projected interest rates?

- Historically how do lenders feel about their relationship with GEMS? How do they view the effectiveness of the finance team at GEMS?

- Does the equity valuation step up makes sense. Since a projected IPO is one of the primary sources of exit and repayment, does the valuation holds up to an aggressive cross examination? One that public markets are likely to subject an controversial issue such as GEMS.

From a modeling point of view, we have quite a few choices. We can model GEMS revenues as a function of schools in the system (48), enrollments (120,000) or capacity utilization (85%). These would be the three core drivers for modeling revenues for GEMS.

Given the questions around book value raised in GEMS valuation step up, a school focused model (asset backed) makes more sense. From an economic outlook point of view a capacity utilization or enrollment driven model is more attractive. We share results from all three models for projected 2019 figures.

You can use the version that makes more sense to you. While getting a seat on the table with GEMS may be easy, walking away with terms that favor bankers over investors and shareholders is going to be a challenge. Assuming we can all ignore the questions around GEMS expensive valuation multiples.

Historical and Projected Financials for GEMS Education – 2015-2019

Founder Puzzles

This article is a chapter extract from Founder Puzzles, Build better businesses right from the start, a new book on financial modeling for founders and startups by Jawwad Farid. Scheduled release date 31-Jul-2020.

Learn more about the book at https://bit.ly/FounderPuzzlesBook. Preorders open now at https://bit.ly/FounderPuzzles

Sources and references

- https://www.forbes.com/sites/saritharai/2014/04/02/chalk-a-block/#493ac34d4e75

- https://www.abraaj.com/wp-content/uploads/2017/02/Abraaj-Case-Study-Gems-Education.pdf

- https://www.hoganlovells.com/en/news/hogan-lovells-advises-mashreqbank-and-the-syndicate-on-gems-educations-aed2bn-loan

- https://www.abraaj.com/wp-content/uploads/2017/02/Abraaj-Case-Study-Gems-Education.pdf

- https://www.blackstone.com/media/press-releases/article/fajr-capital-mumtalakat-and-blackstone-acquire-significant-minority-stake-in-gems-education

- http://www.educationjournalme.com/news/gems-education-refinances-%24818-million-loan_150

- https://www.ft.com/content/8e9dc55f-2c81-3f70-8b0d-008afd105178

- https://www.thenational.ae/business/malaysian-fund-khazanah-buys-3-stake-in-dubai-s-gems-education-1.692163

- https://www.reuters.com/article/gems-ipo/education-company-gems-shelves-multibillion-dollar-london-ipo-sources-idUSL8N1U728K

- https://www.zawya.com/mena/en/markets/story/Dubaibased_GEMS_Education_issues_900mln_bonds-TR20190731nD5N22E05FX2/

- https://www.nasdaq.com/articles/blackstone-fajr-foray-dubai-20-gems-stake-buy-analyst-blog-2014-08-28