Regulation, Monte Carlo, VaR & Option Pricing Courses

Browse through our inventory of free and paid courses on:

- Value at Risk

- Option Pricing

- Monte Carlo Simulation

Take a trial, walk through a sample model or buy our popular Excel model and PDF guide combinations. Based on our popular executive MBA series delivered by our faculty on campuses in Singapore, Kula Lumpur, Dubai and Abu Dhabi.

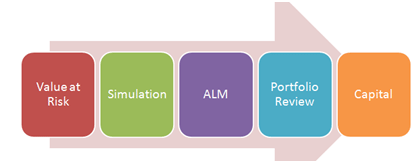

Bank Regulation, VaR & ALM

From Value at Risk & Asset Liability Management to Capital Adequacy Ratios we take a look at metrics, models and Excel spreadsheets. While there is enough here for a short course on all three themes, we also speak about what bank regulation fails in emerging markets because of an unfortunate focus on Capital Adequacy Ratios. Materials sources from the Risk Management and Advance Risk Management courses we run in Dubai and Singapore.

Free Value at Risk Courses

Value at Risk – Methods & Metrics

Why does bank regulation fail?

Calculating Conditional Value at Risk

Asset Liability Management – Assumptions, Convention, Tweaks & Hacks

Premium Value at Risk Course – PDF & Excel files package

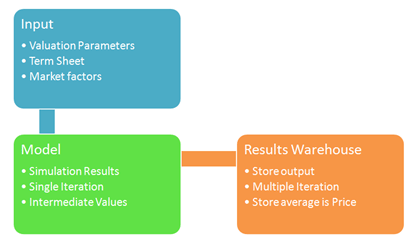

Option Pricing using Monte Carlo simulation

Using Monte Carlo Simulation, Binomial Trees and Black Scholes equation to vanilla and exotic options. If you were looking for a single & comprehensive resource for Monte Carlo Simulation and Option pricing, you have found it. Based on the Derivative pricing course we teach at the SP Jain campus in Dubai and Singapore.

Free Courses

Monte Carlo – How to reference

Pricing Exotic Options using Monte Carlo Simulation

Option Pricing with Monte Carlo Simulation – PDF & Excel files

Advance Topics – Greeks, Optimization, Delta Hedging

The War on (Option) Greeks post collection and the Advance Risk Management workshop resource page.

War on Greeks – The weekend challenge

Advance Risk Management Workshop – Dubai & Singapore Campus