The Option Pricing models 5 nights crash course

2 mins read I am often asked if there is a suggested sequence that I would recommend to finance newbie(s) when it comes

2 mins read I am often asked if there is a suggested sequence that I would recommend to finance newbie(s) when it comes

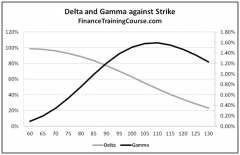

3 mins read Understanding Option Greeks – Introducing Gamma Gamma is the second derivative of the option price with respect to the price

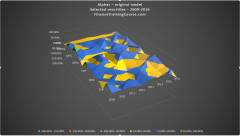

6 mins read Stability and robustness of portfolio Alphas – the excess return metric – and its implication for portfolio allocation and optimization

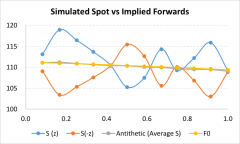

3 mins read Convergence between closed form and simulation model prices is enhanced with variance reduction procedures. It encourages model extension to complex

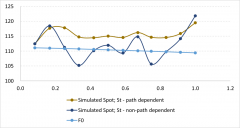

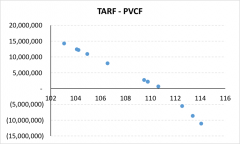

4 mins read Our alternate EXCEL TARF Pricing model uses the Black Scholes close form solution to find a price. The TARF contract

5 mins read Our two part series on TARF pricing models begins where we stopped with our analysis on TARF hedge effectiveness. We