Under Pillar 2 of the second Basel accord, a bank must have an Internal Capital Adequacy Assessment Process (ICAAP) in place. ICAAP consists of internal procedures and systems that ensure that the bank will possess adequate capital resources in the long term to cover all of its material risks.

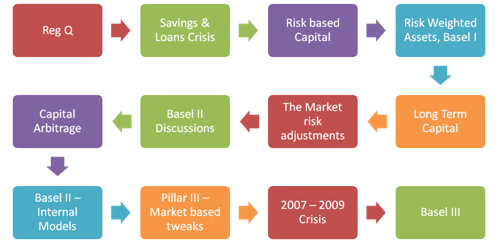

Figure 1 The evolution of banking regulation

It involves the determination of economic capital as opposed to regulatory capital and is a process that is run in parallel to the regulatory capital requirement determination process. Economic capital is the capital required to cover all risks that is estimated using internal risk models of the bank. ICAAP should be an integral part of the bank’s processes and must be embedded within the organization. Senior management and the Board of Directors (BOD) should be supportive and fully engaged in the process.

The Basel Committee has published the liquidity portion of the Basel III reforms to the capital and liquidity framework which aims to resolve the weaknesses and fill in the loopholes of the current Basel II framework that became apparent in the recent financial crisis.

Basel III would require the banking sector to maintain and monitor two key minimum funding liquidity standards as part of the supervisory/ regulatory approach to managing liquidity risk. This would be in addition to the supervisory assessments that regulators would be required to undertake to review whether liquidity risk management frameworks set up by the banks are consistent and in line with published basic principles of liquidity risk management.

Basel II & Basel III Frameworks

Basel II signaled a move away from a purely static regulator driven capital adequacy measure to an internal and relatively invasive assessment of the capital profile of a bank, called the Internal Capital Adequacy Assessment Process (ICAAP).

Under ICAAP requirements a bank needs to have in place internal procedures and processes to ensure that it possesses adequate capital resources in the long term to cover all of its material risks and the board is kept cognizant of any expected or projected capital shortfall.

Basel III introduces significant reforms to the Basel II networks primarily by setting out the supervisory framework for liquidity risk measurement via two minimum funding liquidity standards.

Internal Capital Adequacy Assessment Process (ICAAP)

ICAAP Topics guide

ICAAP overview and concepts

- Definitions and Terminology

- Back ground including Regulation Q, Basel I amendments to the capital accord, Basel II’s minimum capital requirements, supervisor review andmarket discipline processes, ICAAP framework and requirements

- Overview of ICAAP report

- Process and risk of model building

- Prevention and limitation of model risks

- A methodology for calculating Probability of Default (PD)

- Stress Tests for credit risk, market risk and liquidity risk

- Comparison of ICAAP requirements and processes for various Central Banks

- ICAAP Sample report and template (including methodology, risk aggregation, credit portfolio review, internal capital adequacy, ICAAP assumptions and data sources)

Basel III – Liquidity Framework

- Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR)

- 5 metrics for monitoring liquidity risk

- A framework for estimating liquidity risk capital for a bank

- Liquidity Risk Management Case Study (Bear Stearns, Lehman Brothers, AIG)

Basel II & Basel III prerequisites

History behind the current capital adequacy requirement framework

To understand the current capital adequacy requirement framework we begin with an overview of the historical back ground behind the development of Basel II:

- Basel II – Background: Great Depression, Regulation Q, Basel I

- A review of bank regulation and why it really doesn’t work.

- Basel II – A quick introduction & walk through

Basel II and ICAAP

The following courses then address Pillar 2 of the Basel II framework- the Internal Capital Adequacy Assessment Process (ICAAP):

- Internal Capital Adequacy Assessment Process (ICAAP) – Overview and Core concepts

- ICAAP Sample Report Template

- Building a liquidity risk management model for a bank under ICAAP & Pillar III reporting requirements

- Liquidity Stress Testing a Fixed Income Portfolio

- ICAAP: Estimating Strategic Risk Capital for ICAAP

Basel III

Basel III is due to be fully implemented by 2019 and represents reforms to and strengthening of the existing capital requirement and liquidity standards. The following courses in turn review the revisions to the Basel II framework that Basel III encompasses as well as a detailed review of the liquidity reforms.

- Basel III- Basel II framework revisions

- Basel III- Liquidity Framework – Reforms to the Global Liquidity Risk Regulations

- Basel III enhancement- Linking liquidity crisis with Liquidity Coverage Ratio and Stable Funding Ratios

- Probability of Shortfall and Expected Shortfall with or without Basel III

- Basel III Updates – March 2012

VaR measure form an important component for the ICAAP process. The following courses review VaR calculation methodology and use of the VaR measure:

Basel II, Basel III, ICAAP additional topics

Other courses related to Basel II, ICAAP and Basel III are:

- ALM Banking Models – Introductory Case Study

- Why does bank regulation fail? The Kill a bank in one day simulation

- Asset Liability Management – Assumptions, Convention, Tweaks & Hacks

- Value at Risk – Methods & Metrics

- Calculating Conditional Value at Risk

- Liquidity Stress Testing

- Senator Warren, Matt Taibbi, Michael Lewis and Bank Regulators

- Collateral Valuation in Credit Risk Management

- Asset Liability Management

- Liquidity Risk Management Case Studies

- Setting Counterparty Limits, Market Risk Limits & Liquidity and Interest Rate Risk Limits

- Calculating Value at Risk

- Value at Risk Case Study

- Duration and Convexity Example

Basel II, Basel III, ICAAP Related Online Courses

Basel II, Basel III, ICAAP Related PDF Files

- Basel III – Liquidity Framework

- ICAAP – Overview & Core Concepts

- ICAAP Sample Report Template & Executive Summary

- Calculating VaR – includes case study

- Collateral Valuation in Credit Risk Management

- ALM – Crash Course

- Setting Counterparty Limits

Basel II, Basel III, ICAAP Related EXCEL Files

- ALM Crash Course – EXCEL Example (Examples include: Cost to close liquidity gaps, Cost to close interest rate risk, Earnings at risk, Market value of equity)

- Setting Limits – EXCEL Example

- ICAAP – Credit EXCEL Example

- Calculating VaR – EXCEL Example

- Duration Convexity Example