Our new eight part series on TARF Pricing model guide is now live. The objective of the pricing model guide is to introduce both product features and behavior as well as pricing approaches to this common FX structure that can now be found on quite a few corporate balance sheets. Despite the effectiveness and potential of this specific hedging solution, mis-selling is quite common in FX markets. Our hope is that by de-mystifying product behavior and pricing relationship managers and customers will be able to make more informed decisions.

We begin with a quick review of a customer transaction and the question of hedge effectiveness across a number of common and exotic FX hedging solutions. We then quickly make the case for participating forwards and then jump straight into a first principle simulation model for a vanilla TARF. This is followed by two posts on extending the model by adding a closed form Black Scholes solution and a review of convergence techniques to reduce the size of the pricing error.

We close by taking a second look at the mis-selling challenge in treasury markets.

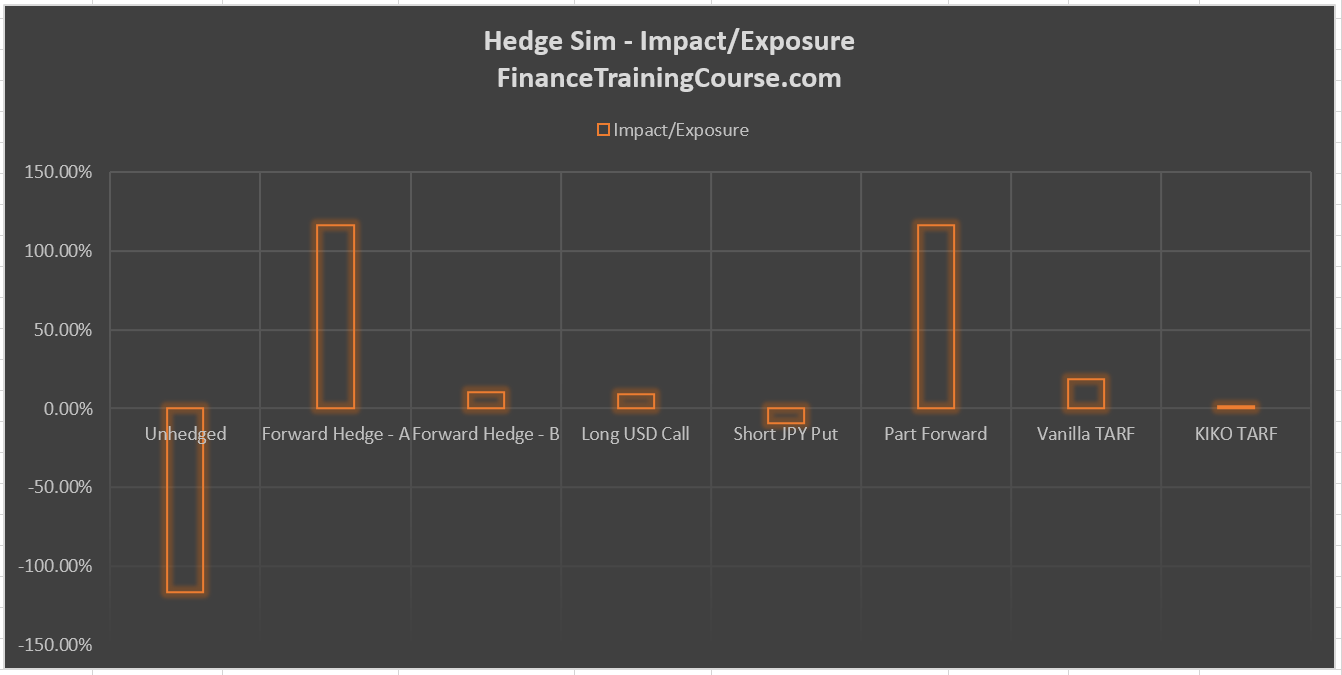

- The case study – Hedging multi leg FX forward exposure

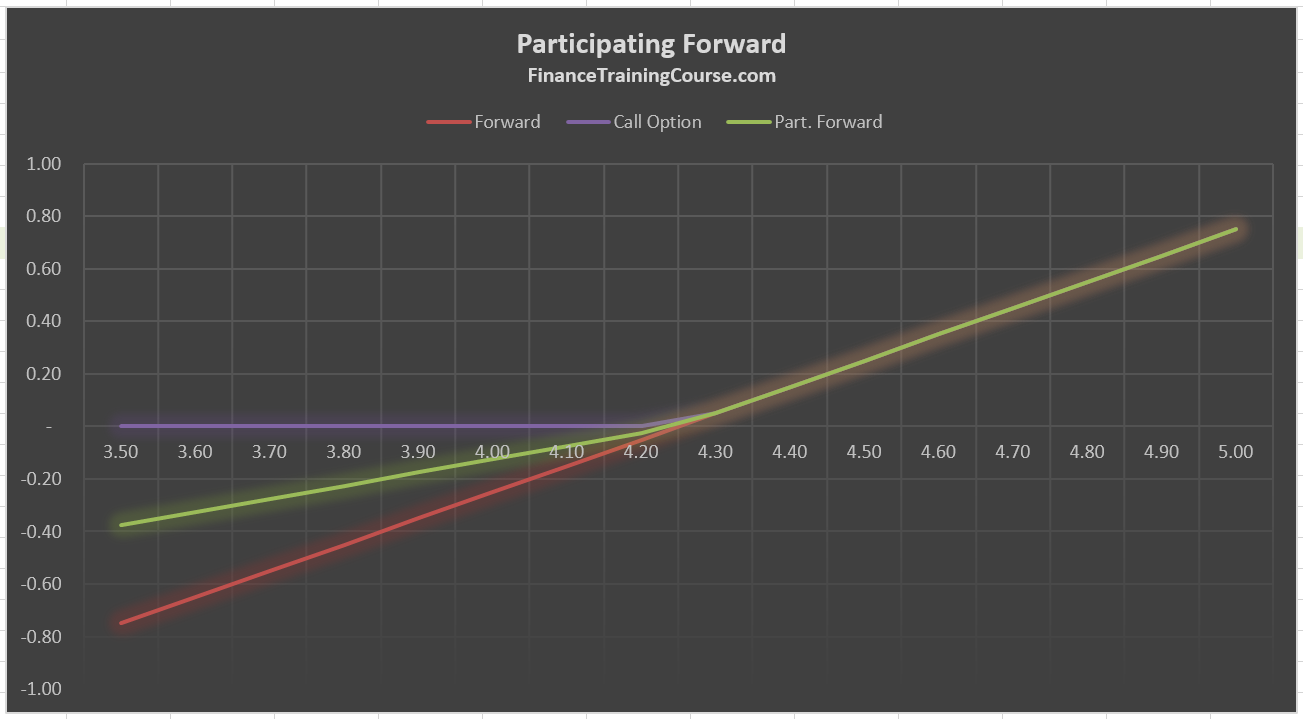

- The case for Participating Forwards

- TARF Pricing Models – Simulation

- TARF Pricing Models – Black Scholes

- Investigating Hedge effectiveness

- Pricing convergence – Excel convergence hacks

- Mis-selling treasury products in FX markets.

- Annex 1 – FX USD Yen convention.

- Annex 2 – TARF Pre-settlement risk (PSR) and PFE exposure estimation models

While the guide is for illustrative, academic and educational use only we expect to have a TARF pricing model package that combines the underlying spreadsheets and PDF pricing guide for sale by mid December. If you are interested in purchasing the model please drop us a line. We will let you know as soon as the model is listed for sale. Please note that given the academic nature of the guide, it’s usage is not recommended for valuation opinions and accounting disclosure without proper professional review and consultation by qualified professionals.