What is Portfolio Optimization?

Portfolio optimization refers to the allocation of limited resources across qualified securities in such a manner to meet or exceed certain target objectives, performance metrics and criteria. The objectives vary by investor and can include minimizing risk, maximizing return, meeting liquidity benchmarks and other limits. The optimization process takes into account a number of factors, such as:

- Investment styles – value vs growth

- Choices available for investment

- Manager fee structure and tax environment

- Regulatory guidelines

- Practical limitations including data availability

- Sophistication and resilience of models used

The Portfolio Management & Optimization Course shows you how to use a simple EXCEL spreadsheet and Solver functionality to allocate resources among multi-asset portfolios. Allocation & optimization occur across sectors and specific securities based on risk, return, liquidity and other limits. The course in its current form was delivered to executive MBA students in Dubai and Karachi between 2016 and 2018.

At an individual level, the biggest reason to study portfolio management is the need to take ownership and control of your own savings and investments. It is important to understand the choices available today to retail and high net worth investors, even though you may not want to manage and run your own money.

Whether it is investment styles, fees, taxes, sector allocation and selection, the models available are bewildering in their range, complexity and eventual payoff.

As fund managers, the speed with which volatility switches gears and technology changes the investment landscape requires you to better understand how your investment management models are put together. This entails understanding under what conditions these models hold and what factors would create enough stress to break them?

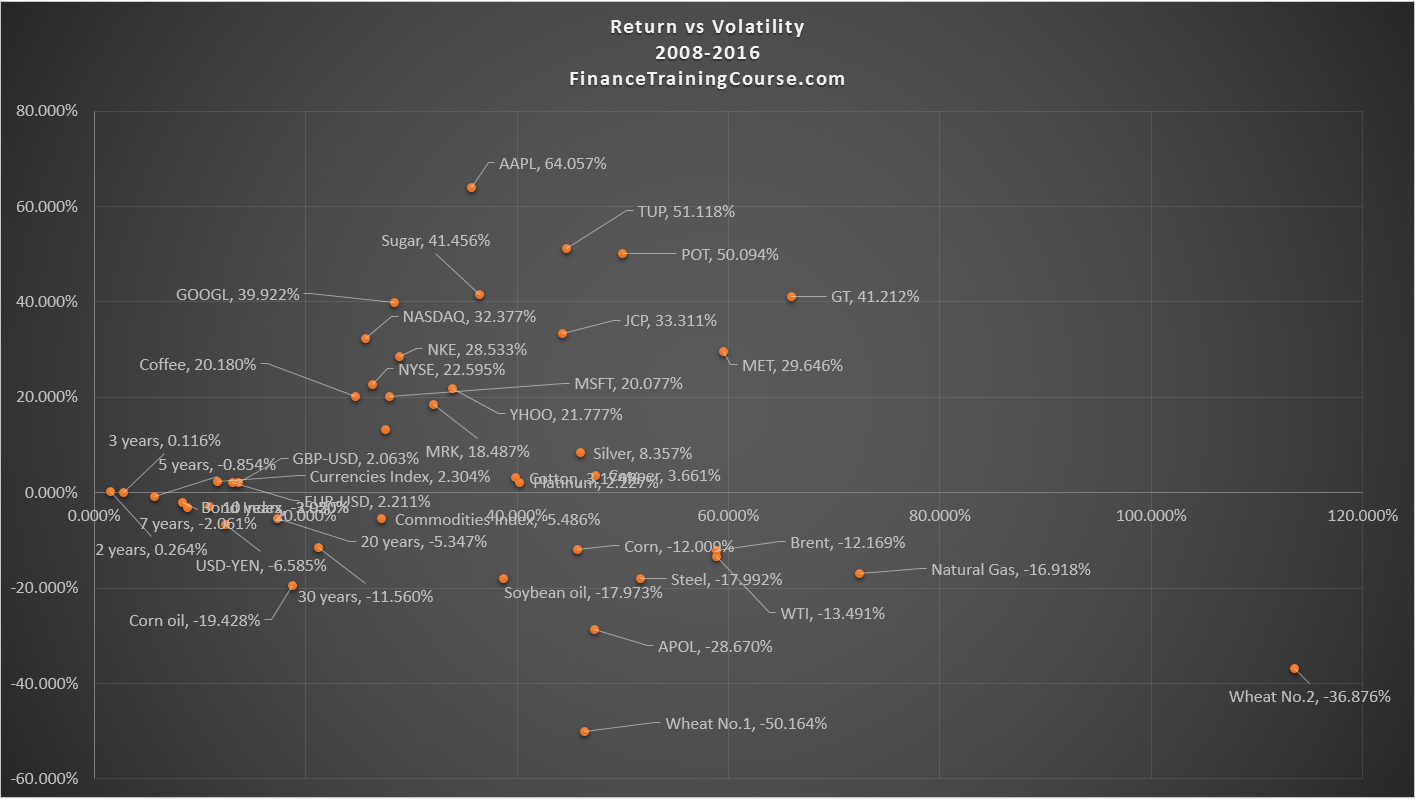

Consider this situation. You have addressed the sector weight and security selection filters of your selection process and now are at a point where you have a pool of 80 qualified investment securities that you would like to pick and choose from for your portfolio. Is there a tool out there that can handle and address the portfolio allocation & optimization questions for you? What about working within a performance evaluation framework? Or using Alpha and Beta to set the optimization function? Do you intend to match and beat an industry benchmark or a market index? What about the calculation of holding period returns? Should it be carried out on a simple interest basis? Or compounded semi-annually?

Business school courses review and cover hundreds of awkward minor challenges, however, these are usually locked away inside some dusty shelf in your brain. Wouldn’t it be nice to have a handy electronic reference to pick up whenever you need to cross check a calculation or a result?

Course Overview

The Portfolio Management & Optimization course aims to do just that by addressing the following core themes:

- Investment landscape: How has the environment changed over the last two decades? What factors do we need to be aware of? What can history tell us about future shocks?

- Models: How do models work at the fundamental level? What assumptions are questionable and what assumptions hold? What drivers can break models and create disasters as well as opportunities?

- Terminology: There is a dictionary of terms in the investment management field. How do we navigate it?

- Practical implementation: How does portfolio management work in practice? Where do we get the data from? What do we do with it? How do we optimize the portfolio for performance and risk?

- Regulatory environment: What does the regulatory landscape look like? We look at the Galleon fund case study to understand the challenges around regulatory compliance that fund managers need to understand and get comfortable with.

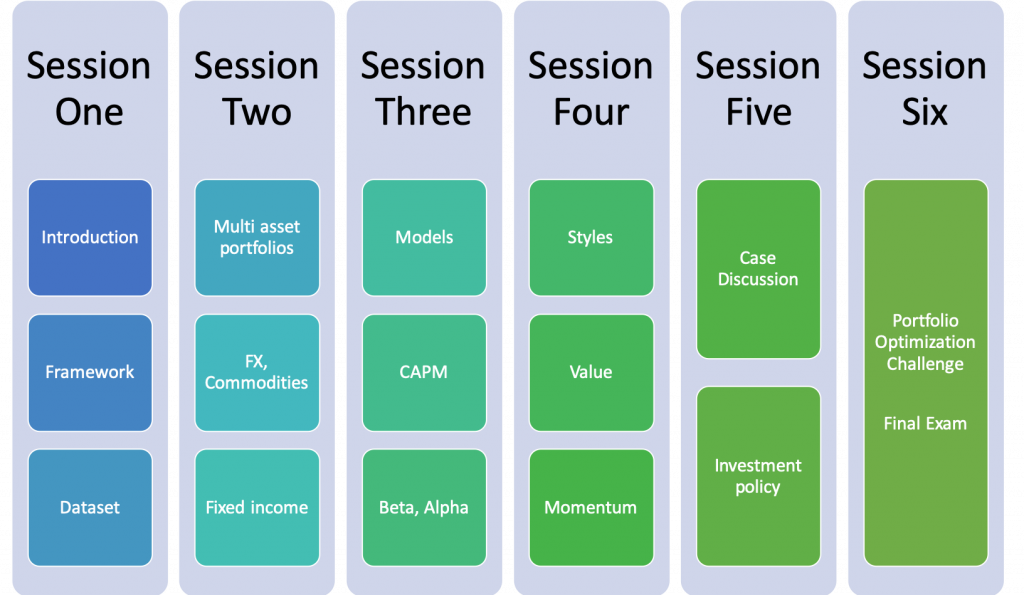

The course consists of the following six sessions:

Session One – Portfolio management drivers and context

The first session covers understanding risk and reward, a first look at mean variance optimization, putting together a simple equity portfolio, sector allocation over security selection and the regulatory framework (see session one’s recommended reading). The lessons include:

- Portfolio Management – Introducing risk and return

- Building the Excel Portfolio management worksheet

- Impact of taxes and fees on retirement savings and spending

- Market Risk – Portfolio volatility

- Market risk metrics – volatility trend analysis.

Session Two – Multi asset class portfolio optimization

Session two of the portfolio management course optimizes a multi asset class portfolio. Fixed income, foreign exchange and commodities are added to the equities portfolio. The optimization is carried out for a single period and over multiple periods. The lessons include:

- Fixed Income Portfolio Optimization using Solver

- Duration and Convexity calculations for Fixed Income Bonds.

- Liquidity stress testing a fixed income portfolio.

Session Three – Portfolio management models – a review of models and weaknesses

Session three takes a second look at the efficient frontier. It introduces multi factor models and APT.

The lessons include:

- The Capital Asset Pricing Model – CAPM (for background and context)

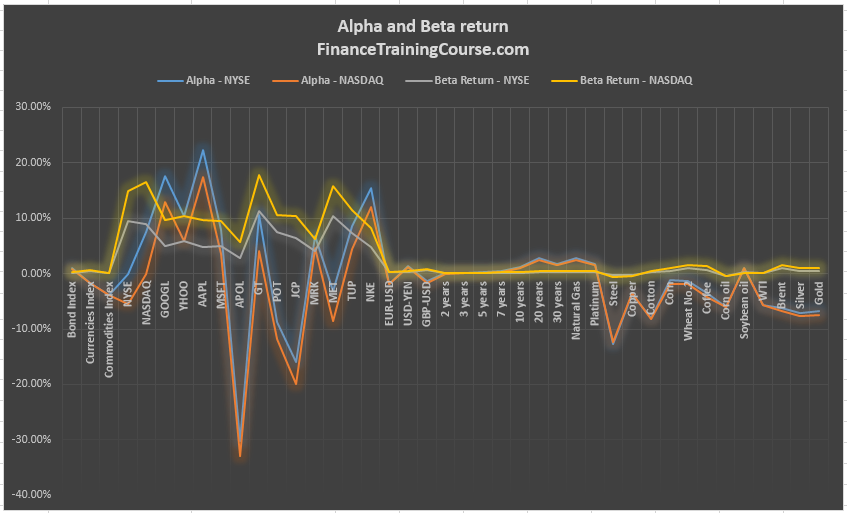

- Calculating Beta and Alpha for portfolio management in EXCEL

- The difference between Alpha and Beta

- Alpha dominant strategy and evaluation

- Portfolio Alpha stability and cyclicality

- Optimal Portfolio Alpha allocation

- Market risk metrics – calculating Beta

- Market risk metrics – Sharpe ratio

- Market risk metrics – calculating Alpha using regression

- Kelly Criterion – founders, start-ups and bet sizes

Session Four – Portfolio management styles – comparing value and momentum

The fourth session presents a quick review of investment styles covering fundamental and technical models, a detailed look at value versus momentum and at active versus passive strategies. We dissect index funds, funds of funds and hedge funds and add more advanced products to the mix.

The lessons include:

- Where do valuation multiples come from?

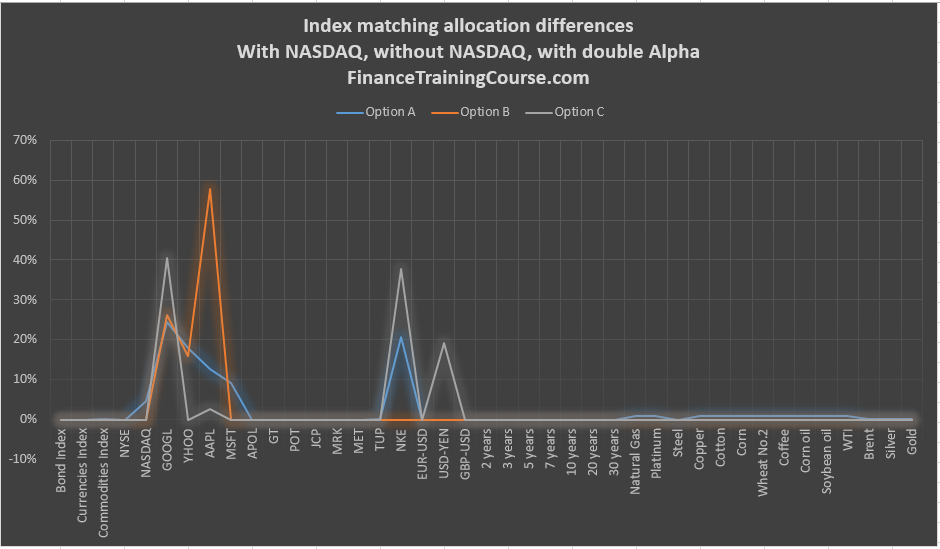

- Index Matching Portfolio Optimization problem set

- Debunking Finance Data Science myths

- The difference between value and growth investing

- The Big Short case study. For value investors, portfolio managers and fixed income traders

- Value investing lessons from the Big Short (film) – Part II

- Understanding CMO CDO and CDS. Big Short Case Study – Part III

- Understanding Synthetic CDO – The Goldman Mike Burry Big Short Trade

Session Five – Risk metrics and investment policy

In this fifth session, we put together investment policy guidelines. We review risk metrics and try to understand volatility and volatility driven metrics, trading and stop losses and the allocation & preservation of capital. We assess if a simpler objective function/target strategy leads to better results.

The lessons include:

- Evaluating Portfolio performance using Holding period return – a case study

- Holding period returns, aggregate returns and annual returns

- Higher Order Portfolio Optimization Models

- Evaluating portfolio performance. A single metric to rule them all?

- Calculating Portfolio Holding Period Return

- Setting Risk Limits that work

Session Six – Portfolio Optimization Challenge & Final Exam

In this session, you will be required to attempt the investment portfolio optimization challenge in EXCEL using the Solver functionality:

And after you have put in the effort you may review the solution:

For more context and background into the problem please see ALM for Board & ALCO Members.

Here is an additional sample exam for practice: Final Exam for Portfolio Management and Optimization Models.

Recommended Readings & Viewings

Initial list

Here is the initial list of books included in recommended reading for the Portfolio Management & Optimization Course. Additional readings are mentioned with each session below:

- Irrational Exuberance, Robert Shiller, Princeton University Press, 2015. Also, take a look at Shiller’s website at Irrational Exuberance for additional resources, updates and datasets. Shiller provides a great review of the history of speculative behaviour and documents the absence of irrationality amidst retail and institution investors. It is a great book on the background and context of successful trading within equity markets and the 2nd and 3rd editions provide updated commentary on the housing market.

- Fooled by randomness, Nicholas Nassim Taleb, Random House Trade Paperbacks, 2005. While reading the book it appears that Taleb wrote the first edition in a fit of cold, controlled anger. It is a brilliant read on chance, failure of models, trader biases, and what it takes to succeed in financial markets as a trader. Taleb identifies, comments on and sets aside many myths that still confound new arrivals at trading desks across the world.

- Thinking Fast and Slow, Daniel Kahneman, Farrar, Strous and Giroux, 2013. For a quick reference on the field see, www.behaviouralfinance.net as well as Misbehaving: The Making of Behavioural Economics. They document the limitations of human behaviour and the commonality of information and intuition biases and errors.

- Competition Demystified, Bruce Greenwald and Judd Kahn, Portfolio publishers, 2007 and Value Investing, also by Bruce Greenwald and Judd Kahn, 2004.

- The Big Short, Michael Lewis. Read the book first. Then watch the movie. If you can’t find the time, see the trailer below, then the two extended clips below under the recommended reading section for Session Four. Also see the two part Big Short Case Study – Lessons for investors, traders and portfolio managers.

- The textbook prescribed for the course is Elton and Gruber Modern Portfolio Theory and Investment Analysis, 9th Edition. I recommend it because I worked with the 5th edition and was very impressed by Elton and Gruber treatment of the subject. A word of fair warning, the book is fairly mathematical and technical but still remains readable. The alternate textbook for the course is Analysis of Investments and Management of Portfolios by Reilly and Brown, 10th Edition, published by CENGAGE. You can use either of the two books for reference or review.

From an investment style point of view, I am clearly biased towards value rather than growth, momentum or technical analysis. While we will cover and review all styles, I will spend a bit more time on value and tend to recommend materials more focused on value.

Session One

Readings:

- How Goldman Sachs lost $1.2 billion of Libya’s money – Matthew Campbell and Kit Chellel, September 2016, Bloomberg

- Hedge Fund managers struggle to master their miserable new world – Saijel Kishan, October 2016, Bloomberg

- Hedge Fund Clients Dump Humans for Computers and Still Lose – Nishant Kumar, November 2016, Bloomberg

Case Study: Regulatory compliance – Galleon Funds:

The Galleon Fund’s insider trading scandal rocked the financial world when it broke in 2009. Galleon at its peak had managed US$ 7 billion in assets and its performance during its peak years was quoted as a benchmark.

The case presents an interesting view on what can or cannot be classified as insider information. This was the primary defence used by the counsel for Galleon’s founder but it was rejected by the jury when it convicted Raj on all 14 counts. On a much more difficult note the case also highlights the impact of insider trading on the lives of people touches. Read more about this regulatory compliance case study in the following articles:

- A dirty business – George Packer, June 2011, The New Yorker

- The Strange, True Story of the Man Whose Maid Was Worth Millions – Nilita Vachani, November 2015, The Nation

- 14 Charged With Insider Trading in Galleon Case – Alex Berenson, November 2009, The New York Times

- Varied Paths in Life After Galleon, but Few Led to Success – Anita Raghavan, October 2014, The New York Times

Session Two

Readings/ Viewings on models:

- The blow up artist – John Cassidy, October 2007, The New Yorker

- Blowing Up – Malcolm Gladwell, April 2002, The New Yorker (the original blow up article juxtaposing Nicholas Taleb against Victor Niederhoffer)

- Nassim Taleb on the Importance of Probability – Bloombery , May 2016

Session Three

Readings on Kelly’s Criterion:

- Understanding Kelly for Portfolio management, Cameron Hight, August 2010, Alpha Theory

- Understanding the Kelly Capital Growth Investment Strategy, Dr William T. Ziemba, 2016, Investment Strategies

- Position Sizing Utilizing the Kelly Growth Criterion, January 2013, Market Folly

- Kelly’s criterions, founders and bet size, October 2019, Jawwad Farid,

Session Four

Film: The Big Short

As Mir mentioned in his session with the class – the single most valued attribute in high performing investment teams is curiosity. This involves figuring out the math, tracing the equation, seeing if the numbers really add up.

See The Big Short – the film based on the Michael Lewis book of the same name to get a sense of what outstanding portfolio managers have in common, why curiosity rules the day and the payoff reserved for individuals who are not afraid to question and challenge assumptions. If you don’t have the time to read the book, check out the summarized case notes for Big Short, prepared for this course

See the following two clips in order. The first presents the pitch for the short trade using CDS. The second walks through the on-the-ground investigation in Florida.

See the full film if you can. If you are serious about portfolio management, you won’t regret it.

Portfolio Optimization Models in EXCEL – The origins

Professor Mark Broadie at Columbia first introduced me to using EXCEL Solver for single and multi-period optimization problems. That material really came together in the first optimization workshop I ran for customers in the MENA region about a decade ago. We added local securities data, market eccentricities, treasury questions, issues around multi asset class optimization. Over the next few years the content grew and evolved as we spent more time with treasury customers, first on the systems side, and then pricing and training.

In November 2016 I ran a week long EMBA course on Portfolio Optimization for 15 students in Dubai at the SP Jain Campus. Post the course, I felt there was a need to put together a manual for students that they could use to play and explore Solver for this purpose. That realization led to a few posts driven by questions asked in the classroom that surprisingly grew into the textbook. While I had been teaching variations of this course for a while, this was the first 18 hour version of the course.

This was quickly followed by a semester long edition at the Executive MBA program at the Institute of Business Administration (IBA) in January 2017 in Karachi. This time the class was blessed by a number of traders and the interaction and the exchange helped refine the material further. We dug deeper in investment styles, formulating investment thesis, marrying frameworks and challenges specific to a given asset class. The book was used for 4 consecutive sections of EMBA students in Dubai and three sessions of executive MBA students in Karachi. The seven sections contributed a great deal of clarity to the treatment as well as identified common intuitive problems not addressed in typical text books on the subject.

Originally put together as a classroom study guide and a handy reference for their final exams, the book is now an intermediate to advance level textbook that looks at real life investment management challenges through the lens of EXCEL Solver. We assume some familiarity with CAPM and APT, hands on expertise with data analysis and modeling in EXCEL and comfort with basic financial modeling.

The textbook with the EXCEL data set and solver templates is available for sale and download on the store.

Target audience

The audience is intermediate level finance, investment and portfolio management professionals and individuals who have an interest in actively managing their savings and wealth portfolios. In wealth management and private banking roles, relationship managers will need to be increasingly current with respect to both asset classes as well as allocation models. The book does a good job of covering both topics.

The book also works well as an advanced level course in investment management for business school students. I have now used it twice to teach the specialization course in Portfolio Optimization after the first five core finance courses have been covered.

To address the challenge with most business school courses, more so with a specialization, of the paucity of time, the book teaches with the aid of a pre-defined dataset. This allows you can to easily follow along and work through the examples in the textbook.

Testimonials for the Portfolio Management & Optimization training